Chemicals, gas-to-liquids (GTL), steel and other industries that consume large volumes of natural gas either directly or as a fuel, expecting the new era of low and stable gas prices to continue are planning tens of billions of dollars in new or expanded facilities in the U.S. But how many of those plans will become a reality? Could the much-anticipated industrial renaissance be undermined by the higher gas prices that might come with the approval of a few more LNG export terminals, new environmental regulations that spur still more gas-fired power generation, and higher natural gas exports to Mexico? Those are critically important questions to gas producers and marketers, who are struggling to figure out just how quickly—and how much—demand for gas will rise. Today we continue our exploration of industrial demand for natural gas.

In Part 1 of "Industrials Say, 'I'm A Believer'", we looked at the factors behind what many think will be an unprecedented shale-driven industrial revival in the U.S., and discussed some key chemical, GTL and other industrial projects now on the drawing boards. Thanks to the nation’s almost limitless shale reserves and the now-widespread use of directional drilling and hydraulic fracturing (see Tales of the Tight Sand Laterals), U.S. gas prices are roughly one-third what they were at their peak five years ago, and they are projected to remain within the $4-to-$5/MMbtu range well into the 2020s. That’s led energy, chemical and steel giants - hoping for an edge over competitors outside the U.S., where naturally gas prices are generally higher - to plan big-dollar industrial projects that would make productive use of that plentiful, relatively inexpensive gas from the Eagle Ford, Marcellus and other major shale gas plays.

Plans to invest billions or at least tens or hundreds of millions of dollars in new industrial facilities are not made lightly. And there is obviously a lot of solid thinking behind the plans by smart companies like Sasol, G2X Energy, Methanex and others to spend precious capital on projects whose success will depend in large part on steady flows of reliably low-price natural gas. The consensus view, as we’ve said, is that gas prices in the U.S. will rise only very gradually over the next few years, and it’s logical to think that the sheer magnitude of the shale gas ready to be drilled for, produced and delivered would likely serve as a wet blanket if gas prices start to heat up.

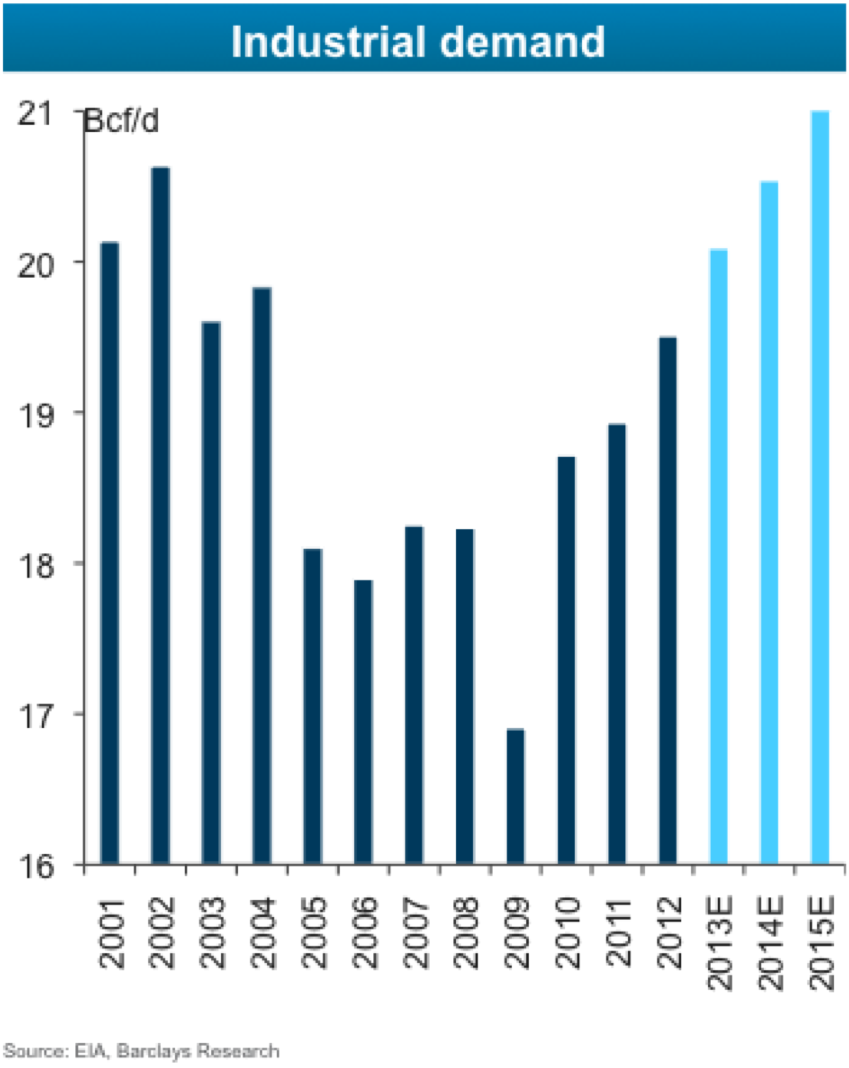

That’s a key assumption in Figure #1 below from a presentation by Biliana Pehlivanova, Head of Global Gas Research, Barclays Capital at a Platts conference in Houston last week. (Sept. 23, 2013), The Barclays analysis indicates that U.S. industrial demand for natural gas, which fell to less than 17 Bcf/d at the depth of the economic downturn in 2009 but rebounded to about 19.5 Bcf/d last year, now stands at about 20 Bcf/d and will rise to 20.5 Bcf/d in 2014 and 21 Bcf/d in 2015. This might not sound like all that much growth. But the reason is that it takes time – several years to build these plants. The significantly bigger gains for industrial use of natural gas could follow in the 2016-18 period, when many of the larger-scale GTL, ethylene, ammonia/urea and methanol projects now on the drawing board are expected to begin commercial operation. For example, Barclays figures that while only 2.2 million tonnes per annum (MMtpa) of new ethylene capacity will come online in the 2013-15 period, 8.4 MMtpa more will begin operating in the following three years. Similarly, only a relative smidgen of new ammonia, urea and urea ammonium nitrate capacity—maybe 3.5 MMtpa of it—is slated to start up in 2013-15, but 10 MMtpa is scheduled to come online in 2015 alone, and nearly another 6 MMtpa the year after that. The same goes for methanol; just under 3 MMtpa of new methanol capacity is seen operating by the end of 2015, with 4.5 MMtpa more to follow in 2016. And the biggest GTL projects--the most direct users of large volumes of natural gas—are still severalyears away from startup. As we noted in Part 1, Sasol is in only the front-end engineering and design (FEED) phase on an $11 billion-plus, 96 Mb/d GTL plant in Lake Charles that would come online in two phases in 2018 and 2019. And Royal Dutch Shell may be a year or two away from committing to a multibillion-dollar GTL project of its own in Louisiana; again, that facility would not beigin operating until late in this decade. If all the post-2015 industrial capacity that has been announced comes online it could mean another 3 Bcf/d of demand or more. But that demand is far from a certainty.

Figure 1 - U.S. Industrial Demand for Natural Gas; Source: Barclays Research

Plans and commitments to build new industrial projects are two distinct things—and it’s not unheard of for a company to actually start constructing a major facility and either suspend or cancel the work sometime later if key market conditions change enough to warrant it. As anyone who experienced the dizzying heights of natural gas prices in 2008 and the equally dizzying depths of 2012 knows, forecasting long-term gas prices is a tricky business at best, and regional gas production activity, gas-transmission constraints and other local factors make it even tougher to predict what gas from any particular shale play will cost five or 10 years from now. Forecasts and forward prices for natural gas build in a consensus view of the good and bad that is likely to happen, but there is a large set of unknowables right now that could lead the widely anticipated boom in industrial demand for gas to shrink to something more like a boomlet. A few examples? What if the Federal Energy Regulatory Commission (FERC) ends up approving a few more LNG export terminals than most think it will? FERC already has approved three such projects, with a combined capacity to export the LNG equivalent of 5.6 Bcf/d, and several more LNG export proposals are on-deck (see Figure 2). The impact of a bigger-than-expected expansion of LNG exports is pretty clear: Dow Chemical, a vocal opponent of LNG export expansions, has said that its plan to invest several billion dollars along the Gulf Coast to expand its ethylene and propylene capacity could be set back if LNG exports are permitted to boom and domestic natural gas prices rise as a result.

Comments

I hope we don't "screw the pooch" by chasing short term returns on international sales of commodity gas. Those currently attractive returns will quickly disappear as gas prices "adjust" to a new international standard. Instead, we should focus on longer term but more challenging opportunities that utililize our gas bonanza to make us very competitive exporting value-added products. The net result of this can be a large reduction in our trade deficit leading to a reduction of national debt. (Of course, that also assumes we have a functional government, not a given by any means)