More than 70 new data centers are under development in Virginia, which is already the world’s leading hub for the massive, high-tech facilities. But given the rapid pace of the buildout and the challenges that come with it, it’s probably no surprise that not everyone in the Old Dominion State is as enthusiastic about data centers as they once were. In today’s RBN blog, we’ll look at some of the biggest data centers in the works and discuss their path forward.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

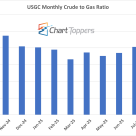

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

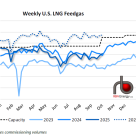

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

Gulf Coast diesel cracks (margins over crude) have averaged $8/Bbl more than gasoline for the past two years. As a result, Gulf Coast refiners have been producing more diesel than gasoline for the first time since records began. US demand for diesel has remained flat but exports have boomed. Diesel has been a shining light for US Gulf refiners at a time when their colleagues on the East Coast and in Europe are heading for the exits. Today we examine the diesel boom and where it is headed.

Oil production from the North Dakota Bakken shale reached 639 Mb/d in May 2012. Associated natural gas production was 651 MMcf/d. So far oil production has been the main focus for Bakken producers. Gas production has been an afterthought. So much so that 1/3rd of it is flared. A new BENTEK study for North Dakota energy policymakers (we provide a link to the study) indicates natural gas volumes in the region will increase substantially in the coming years. The obvious market for this gas is to displace Canadian gas flowing through the Bakken to get to the Midwest. Today we look at the coming battle for pipeline capacity between producers in the Bakken and those in Canada.

On June 1st, Mont Belvieu propane non-TET fell to 70 cnts/gal from about 150 cnts/gal six months earlier, down more than 50%. See Graph #1 below. But over the past couple of weeks the propane price has rebounded. On Friday the OPIS propane number was up to 89.4. Have we hit bottom for the time being? What makes propane prices move the way they do in the first place? Today we’ll continue last Friday’s blog series that covered trading and pricing of natural gasoline, normal butane and isobutane with a deep dive into the same issues for the most famous of the NGLs – propane.

Natural gas liquids trading is quite unlike natural gas or crude oil. Natural gas is natural gas. It is a truly fungible commodity. Crude oil varies widely in quality, but it is still crude oil. Not so, NGLs. Each of the five NGLs has different physical characteristics, different end-use markets and most importantly, different factors that make prices rise and fall. It is not at all unusual for ethane prices to increase while normal butane prices fall. Or vice versa. What makes this

Ethanol from corn as a motor gasoline blend stock seems like a good idea. As an oxygenate it is supposed to clean up the air, and as a U.S grown renewable it reduces our dependence on fossil fuels and foreign oil. The catch is that ethanol is being mandated under a morass of mind-numbingly complex government regulations, some of which conflict with each other, or worse yet are out of step with the realities of the market. For example, the mandatory volumes of ethanol required may soon exceed the quantity that the market can use. At the same time, high corn prices have driven margins on ethanol manufacture into the red forcing many ethanol producers to shutter their operation, reducing ethanol supplies. And if that were not enough, a government program created something called the renewable identification number – RIN – a 38-digit serial number that ‘tags’ batches of renewable fuels and has resulted in all sorts of complications. Today we’ll begin an examination of the ethanol market to understand how we got in this predicament and where we go from here. In Part I we tackle one of the most intractable problems – the Blend Wall.

After NYMEX WTI climbed higher all last week, topping $90/Bbl, euro-zone worries yesterday caused a 4 percent fall in crude to close at $88.14/Bbl. That is a still a long way above estimates of $50/Bbl break-even prices for crude produced from Eagle Ford shale. Oil production in the Eagle Ford is now close to 600 MB/d and estimated by Bentek to rise to over 700 MB/d by the end of this year. This South Texas play is attracting producers like bees to a honey pot. Midstream infrastructure projects are springing up left right and center. In the first of a series we look at how Eagle Ford crude prices compare to the Bakken.

August natural gas closed on Friday at $3.08/MMbtu, up 8.2 cnts and above $3.00 for the first time since January 9th 2012. Crude oil was down $1.22 to $91.44/bbl. That puts the gas to crude oil ratio at 30X, about half the 54X milestone hit in April and celebrated here in the series The Golden Age Of Gas Processors. Since then gas prices are up 60% while NGLs are down 20%. April ethane production was down 4% (due to ethane rejection), and may fall another 8% by the time we see the July EIA numbers. So is the Golden Age over already? Are gas processors panhandling on the streets of South Texas – “Will Process Gas for Food”? Or are processing margins still strong enough to make the Lexus payment just not cover the Mercedes as well? To figure this out we’ll resurrect the RBN Golden Age spreadsheet and drill down into the numbers.

King Coal is hurting. NYMEX Central Appalachian Coal prices have fallen 18 percent so far this year from $68.67/ short ton (ST) on January 3, 2012 to $57.23/ST on Monday (July 16, 2012). Coal consumption is down and coal company profits are hurting. Patriot Coal filed for bankruptcy last Monday. On top of these woes, new environmental regulations look set to pull the rug from under new coal power plant construction. Today we ask what the future holds for the US coal industry.

United States coal consumption is falling. Over 90 percent of the coal consumed in the U.S. is used to generate electricity. According to the Energy Information Administration (EIA) power-sector coal consumption fell from 975 million short tons (MMst) in 2010 to 929 MMst in 2011. The July 2012 EIA short term energy outlook forecasts that coal consumption for 2012 will fall to less than 800 MMst . Coal production for the first five months of 2012 was 6 percent below last year's level for the same period and EIA predicts an overall fall in production of 9 percent for 2012. Despite lower production EIA forecasts secondary stocks (at power generation facilities) to be close to record levels by the end of 2012 and to remain at those levels during 2013 (see chart below).

A week or so ago in Part IV of the Marcellus Changes Everything series, we noted that by 2016 there would be a summer surplus of natural gas production from the Marcellus of around 3 Bcf/d. We pointed to Dominion’s Cove Point LNG proposed export terminal on the Chesapeake Bay as one likely outlet for the surplus. Dominion’s proposal is one of 14 LNG terminals being reviewed by the government for an export permit. Today we investigate how many of these terminals will be built and whether the natural gas markets sustain can such a high level of exports?

Three years ago the predicted onslaught of Marcellus NGL production kicked off a horse race to build new ethane pipelines out of the region. At one time, at least seven different projects were being promoted. Since then most of the projects have dropped by the wayside, yielding to Mariner West (MarkWest/Sunoco) and ATEX (Enterprise). Do those two projects provide enough capacity? Perhaps too much? What about possible competition from a new Marcellus/Utica NGL pipeline project that hit the radar screen last week? Could that be a signal that a lot more liquids are on the way?

Just when we thought that East Coast refining had become an oil company’s equivalent of musical chairs and all the players were headed for the exits, a consortium including Carlyle, original owners Sunoco, and JP Morgan strung together a deal to save the 330MB/d Philadelphia refinery that had been slated for the scrap heap. Can the new consortium succeed? How will they overcome the obstacles that chased the previous owners off the lot? Today we look at why they just might succeed.

Today the Energy Information Administration (EIA) publishes weekly US natural gas storage numbers for the week ending July 6, 2012. Last week EIA reported 39 Bcf injections making the total storage 3,102 Bcf. The natural gas stockpile is now 602 Bcf higher than this time last year but the rate of storage injection has slowed as a result of increased demand for natural gas burn by power generators. In today’s blog we look at the supply demand picture to see what is driving higher natural gas burn by power generators and the implications for storage.

So far this year WTI crude prices have fallen 22 percent from their highs in February 2012 to close at $85.99 /Bbl yesterday (Monday). Brent crude prices fell 21 percent over the same period to close at $99.73 /Bbl yesterday. WTI has traded at an average discount to Brent of $15 /Bbl this year. Historically WTI always traded at a slight premium to Brent. The crudes share similar qualities. In today’s blog we ask when will the WTI discount to Brent end, if ever?

Over the next five years, natural gas production in the Marcellus is expected to double, from just less than 8 Bcf/d today up to almost 16 Bcf/d in 2016. As that production enters the market, volumes that have traditionally served the Northeast market from LNG imports, Canadian imports, inflows from the Rockies/Midwest, and inflows from the Gulf will no longer be needed. Last week we examined possible scenarios for these flow shifts. Today we’ll look at the ramifications for regional supply imbalances and where the traditional supplies will be going if not to the Northeast in this, the Great Flow Reversal of 2016.

In little more than two weeks, the CME/NYMEX prompt natural gas futures contract is up $0.76 to close at $2.945/MMbtu on Thursday (see graph below). That’s getting dangerously close to $3.00. Yesterday we noted that it was the drop below that $3.00 threshold that kicked off serious coal to gas switching in January. Now that the price is near to crossing the $3.00 mark the other way, we better look carefully at how plant fuel costs drive generation economics for natural gas versus coal. To do so we’ll take a deep dive into the math.