Oil production from the North Dakota Bakken shale reached 639 Mb/d in May 2012. Associated natural gas production was 651 MMcf/d. So far oil production has been the main focus for Bakken producers. Gas production has been an afterthought. So much so that 1/3rd of it is flared. A new BENTEK study for North Dakota energy policymakers (we provide a link to the study) indicates natural gas volumes in the region will increase substantially in the coming years. The obvious market for this gas is to displace Canadian gas flowing through the Bakken to get to the Midwest. Today we look at the coming battle for pipeline capacity between producers in the Bakken and those in Canada.

Last week, the BENTEK analysis of Williston Basin natural gas production growth through 2025 for the North Dakota Pipeline Authority was published. Free to the public! The 179 page study’s stated objective is to determine if adequate natural gas pipeline infrastructure exists in North Dakota to handle future growth. The study forecasts an increase in natural gas production for the Williston Basin from 651 MMcf/d in 2012 to 2.1 Bcf/d in 2017 and 3.1 Bcf/d in 2025. You can access a copy here:

“North Dakota Pipeline Authority – Natural Gas Production Study July 2012”

So far the Bakken play has been all about oil, with natural gas and natural gas liquids (NGL) playing second fiddle. Rapidly growing oil production is forecast to reach 1.7 Mb/d by 2017. The more than 50 active operators in the Williston are putting up with transport constraints out of North Dakota and lower crude prices (see “The Bakken Buck Starts Here – Bakken Crude Pricing Part I, Part II and Part III”). In spite of these drawbacks, high oil production rates still assure them a healthy rate of return.

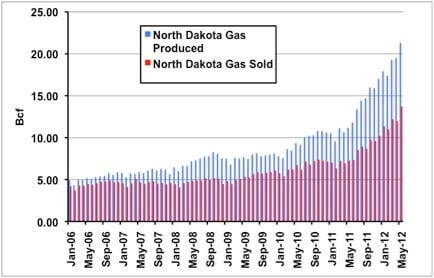

Source: North Dakota Drilling and Production Statistics

Gas production from the Bakken is largely attributable to “associated gas”. Associated gas comes out with oil from a liquids well and typically is not the primary revenue generator for producers. Around 36 percent of gas from North Dakota wells is currently not sold (see Chart 1 above – source ND drilling and production statistics). That unsold gas is flared at the wellhead. The gas to oil ratio (GOR) for North Dakota production based on May 2012 production numbers is about 1 Mcf/d of gas per Bbl of oil which is low by comparison to other US shale plays.

Natural gas prices fell below $2/MMbtu in April this year and only recently returned above $3/Mmbtu. The impact of flaring on overall well profitability is reduced by these lower prices. Until infrastructure is built to deliver the gas to market, flaring will continue. However the issue of natural gas flaring is attracting increased attention from the Environmental Protection Authority (EPA). Bakken producers may soon no longer be allowed to ignore their flared gas.