Gulf Coast diesel cracks (margins over crude) have averaged $8/Bbl more than gasoline for the past two years. As a result, Gulf Coast refiners have been producing more diesel than gasoline for the first time since records began. US demand for diesel has remained flat but exports have boomed. Diesel has been a shining light for US Gulf refiners at a time when their colleagues on the East Coast and in Europe are heading for the exits. Today we examine the diesel boom and where it is headed.

Before we start - a quick note on diesel and distillates. Today we are mostly talking about diesel produced by Gulf Coast refiners. Diesel is part of a pool of refined products with similar qualities that are called distillates. The data we will use include import and export numbers from the Energy Information Administration (EIA) that are grouped together as distillates. The main differences between distillate products produced by Gulf Coast refiners are in the sulfur content. US refiners now mostly produce ultra low sulfur diesel (ULSD) to meet new 15 parts per million (ppm) sulfur specifications mandated by the Environmental Protection Agency (EPA) since 2010. The sulfur specifications required by countries that the US exports diesel to can be lower or higher than for ULSD.

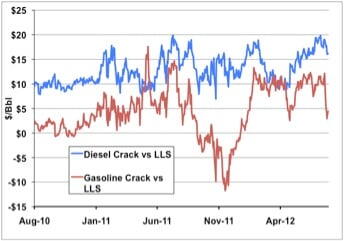

Over the past two years producing diesel has been very profitable for Gulf Coast refiners. In the chart below the blue line is the Gulf Coast ULSD crack spread (crack spread math defined in a minute – bear with us) against Gulf Coast benchmark Light Louisiana Sweet (LLS) crude. The red line is the Gulf Coast gasoline crack spread against LLS. The ULSD crack spread has averaged $12.88/Bbl since August 2010. Over the same period the gasoline crack averaged only $4.50/Bbl and at times fell as low as $-11/Bbl.

Source: CME NYMEX Data from Morningstar

For those unfamiliar with crack spreads (the rest of you can jump to the next paragraph), we talked about 3-2-1 crack spreads in our analysis of refining margins for Bakken crude producers (see “The Bakken Buck Starts Here – Bakken Crude Pricing Part IV”). In that case the 3-2-1 crack spread we used was an approximation of a refining margin based on a ratio of crude (3 Bbls) gasoline (2 Bbls) and heating oil (1 Bbl). In this case we are simplifying things further by calculating the price spread or “crack” between Gulf Coast diesel and LLS crude and Gulf Coast gasoline and LLS Crude. As in all crack spread analysis, we run the risk of over simplifying the complex economics that dictate refinery profitability. However, as a rule of thumb, these crack spreads (or just “cracks” if you want to sound credible) tell us whether it is profitable for refiners to make distillate or gasoline and which product is more profitable.