So far this year WTI crude prices have fallen 22 percent from their highs in February 2012 to close at $85.99 /Bbl yesterday (Monday). Brent crude prices fell 21 percent over the same period to close at $99.73 /Bbl yesterday. WTI has traded at an average discount to Brent of $15 /Bbl this year. Historically WTI always traded at a slight premium to Brent. The crudes share similar qualities. In today’s blog we ask when will the WTI discount to Brent end, if ever?

West Texas Intermediate crude (WTI), the US domestic benchmark and Brent crude, the benchmark for crude sold in Europe, Africa and the Middle East are both light sweet crudes with similar refining qualities. WTI has a gravity of 39.6 API degrees and sulfur content of 0.24 percent. Brent has a gravity of 38.06 API degrees and sulfur content of 0.37 percent. Historically, WTI and Brent prices tracked closely, with WTI generally having a slight premium over Brent. Since August 2010 WTI has traded consistently at a discount to Brent that ballooned out to $27.68 /Bbl in October 2011 and has averaged $15 /Bbl so far this year.

Analysts and commentators generally attribute the WTI discount to Brent to logistics constraints at Cushing OK caused by an historic change in US crude supply sources. New and growing domestic crude production in the prolific North Dakota Bakken shale as well as a surge in Western Canadian crude imports into the US have taken the place of imported crudes previously delivered into the US Midwest via pipelines from the US Gulf Coast. Bakken production and Canadian imports exceed Midwest refining capacity and are stockpiling at the Cushing OK pipeline and trading hub with few outlets currently available to reach the large refining complexes on the US Gulf Coast. In addition pipeline constraints are restricting the flow of Bakken crude out of North Dakota into Cushing or to refining centers on the East Coast and the Gulf Coast. The resulting crude surplus in the Midwest exerts downward pressure on WTI prices while Gulf Coast refiners unable to source lower priced domestic crude are paying higher Brent related prices for imports. [Note that it has been a while since actual Brent crude was imported to the Gulf Coast and light sweet crude imports originate mostly from West Africa but are priced against Brent. This is due to a decline in the production of North Sea Brent stream crude and the shorter distance from West Africa to the Gulf making freight less expensive.]

The Midwest logistics constraints cannot be solved overnight because it takes a long time to gain approval for and then to build the necessary new pipelines from Cushing to the Gulf Coast that will relieve the Cushing oversupply. The first step in that process was the reversal of the Seaway pipeline in May of this year. The Seaway pipeline runs from Cushing to Houston and initially carries 150 MBbl/d of light crude to the Gulf Coast. Early next year (2013) Seaway capacity will expand to 400 MBbl/d and by mid 2014 proposed expanded capacity will increase the flow to 850 MBbl/d. Later this year the Keystone Gulf Coast project will commence construction with an anticipated in service date of mid to late 2013 and an initial capacity of 700 MBbl/d. In theory, once adequate pipelines open up the supply lines from Cushing to the Gulf Coast, the downward pressure on WTI prices will evaporate and the US domestic benchmark will once again track closer to Brent.

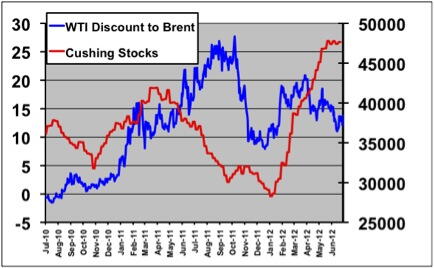

Looking at the data, the chart above shows the growing stockpile at Cushing (red line, right axis) and the Brent minus WTI spread (blue line, left axis) since August 2010. The WTI discount to Brent fell below $10 /Bbl in the last two months of 2011 partially in response to the announcement of the Seaway reversal. Between February and May of 2012 the WTI discount was consistently back up above $15 /Bbl. Since then the spread has traded as low as $11 /Bbl and is currently at $13.74 /Bbl.