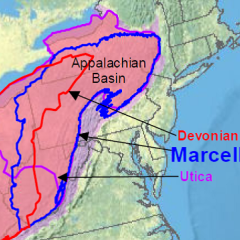

Three years ago the predicted onslaught of Marcellus NGL production kicked off a horse race to build new ethane pipelines out of the region. At one time, at least seven different projects were being promoted. Since then most of the projects have dropped by the wayside, yielding to Mariner West (MarkWest/Sunoco) and ATEX (Enterprise). Do those two projects provide enough capacity? Perhaps too much? What about possible competition from a new Marcellus/Utica NGL pipeline project that hit the radar screen last week? Could that be a signal that a lot more liquids are on the way?

Last week I spoke at the Infocast Marcellus & Utica Infrastructure Summit in Pittsburgh. Capacity issues out of the region for both ethane and propane were the topics of my presentation, titled ‘Marcellus Infrastructure: Getting Ethane and Propane to Market’. We can’t cover everything in that presentation here, but today I’ll hit the high points of the ethane situation and we’ll pick up the propane issues later in the week.

Before we get started, we need to recount a semi-snafuish interchange from the Infocast Summit. We mention it here only because it is directly relevant to our topic. It started when Caiman Energy CEO Jack Lafield mentioned in a panel presentation that Williams Partners (recent purchaser of Caiman’s midstream business and major investor in Caiman Energy II) is planning to build a new 150-200 Mb/d pipeline to move y-grade from MarkWest’s Houston plant in Pennsylvania to the Gulf Coast. There was even a name for the new pipeline – Bluegrass.

The story was picked up the next day by the energy press. Well….the announcement must not have been ready for prime time, because the next day Williams tried to put the quietus (East Texas word) on the whole thing. For example, Argus Natural Gas Americas noted in their next edition that Williams has “no immediate plans to build NGL takeaway capacity out of the Marcellus or Utica” and indicated that Mr. Lafield clarified his statement to say that Williams is “studying such a project but no decision has been made.”

Regardless how all this plays out, it certainly sounds like serious consideration is being given to yet another route for NGLs to exit the region. How does that jibe with current forecasts for NGL/ethane outbound flows? Well, if a new pipeline out of the region is being considered, it‘s because either (a) the new alternative is expected to significantly out-compete ATEX in the market (unlikely since ATEX has firm throughput commitments from Chesapeake and Range that grow from 65 Mb/d in 2014 to 105 Mb/d in 2017), or (b) A LOT more liquids are expected to be produced in this region than most forecasts are predicting. Contemplate that concept for a couple of minutes before we get into the nitty-gritty.