King Coal is hurting. NYMEX Central Appalachian Coal prices have fallen 18 percent so far this year from $68.67/ short ton (ST) on January 3, 2012 to $57.23/ST on Monday (July 16, 2012). Coal consumption is down and coal company profits are hurting. Patriot Coal filed for bankruptcy last Monday. On top of these woes, new environmental regulations look set to pull the rug from under new coal power plant construction. Today we ask what the future holds for the US coal industry.

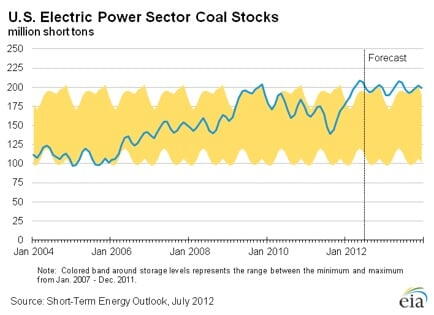

United States coal consumption is falling. Over 90 percent of the coal consumed in the U.S. is used to generate electricity. According to the Energy Information Administration (EIA) power-sector coal consumption fell from 975 million short tons (MMst) in 2010 to 929 MMst in 2011. The July 2012 EIA short term energy outlook forecasts that coal consumption for 2012 will fall to less than 800 MMst . Coal production for the first five months of 2012 was 6 percent below last year's level for the same period and EIA predicts an overall fall in production of 9 percent for 2012. Despite lower production EIA forecasts secondary stocks (at power generation facilities) to be close to record levels by the end of 2012 and to remain at those levels during 2013 (see chart below).

The main reason for lower coal consumption this year is lower natural gas prices leading to coal power generation switching to gas. We discussed that phenomena in several recent blogs (see A Hunk a Hunk of Burning Gas – Will Natural Gas Power Demand Keep The Lid on Storage?, Talking Bout My Generation – Coal to Gas Switching – Part I, and Part II). We concluded that generation switching from coal to natural gas is largely dependent on the fuel cost of natural gas CCGT generation remaining significantly below the fuel cost of equivalent coal steam generation. That was true during the second quarter of 2012 when natural gas plant fuel costs stayed at least $3/MWH below typical coal plant fuel costs. EIA reported in July that during April 2012 natural gas and coal were each used for an equal 32 percent of total US power generation for the first time ever and representing a dramatic shift from the previous April when coal was used for 41 percent of generation versus 23 percent for gas. During the first quarter 2012 both coal and gas consumption suffered when a milder than usual winter reduced demand for heating.