The popularity of weather derivatives has ebbed and flowed since their introduction in the late 1990s but trading activity has rebounded in recent years as the trading community has increasingly begun to reassess the need to hedge weather-related risks — everything from high temperatures and rainfall levels to power prices and cooling demand. In today’s RBN blog, we examine the role of weather derivatives, how they are used to hedge risk, and why they may be becoming increasingly important to the energy industry.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

US oil and gas rig count climbed to 549 rigs for the week ending September 26, an increase of seven rigs vs. a week ago and the largest gain since July according to Baker Hughes data.

Low-carbon steel that utilizes green hydrogen in the production process will be used in Microsoft data centers under an agreement announced this week with Swedish steelmaker Stegra.

While most of the country is enjoying the benefits that low cost North American supplies of natural gas bring to local and regional economies, many parts of the Northeast US and Atlantic Canada are still heavily reliant on expensive oil-based products for residential, commercial and industrial use. That is in spite of the proximity of burgeoning supplies of natural gas in the Marcellus and Utica shale basins. The challenge in converting users away from oil lies in infrastructure build out and deciding who will pay. Today we begin a two part series on the slow conversion process and new solutions to supply natural gas to customers before pipeline infrastructure is built.

Next year (2014) RBN Energy expects Utica natural gas processing plants to produce 43 Mb/d of natural gasoline – more than 3 times 2013 production. Local demand will only soak up 17 Mb/d – leaving 26Mb/d needing transport to markets outside the region. Midstream companies are building infrastructure to accomplish this – by pipeline, rail, truck or barge. Today we conclude our survey of Utica Condensate and natural gasoline takeaway.

Midstream companies are expanding their infrastructure in Edmonton, Alberta. Kinder Morgan is adding over 5 MMBbl of storage at the origin terminal for its Trans Mountain pipeline to the West Coast. However new investment is also being piled into rail infrastructure – including Kinder’s JV unit train loading terminal with Keyera. Canadian producers are shopping for routes to market that offer them optionality that can help mitigate congestion and discounting. Today we describe five company’s infrastructure plans in the Edmonton region.

The bases are loaded for another 2 MMb/d of pipeline capacity to bring additional crude supplies to the Texas Gulf Coast by the end of 2014. The majority of that payload will likely be light sweet crude from tight oil formations, a.k.a., shale. As the flood of crude headed to Texas passed through the Midwest over the past two years, prices at Cushing and points north were heavily discounted versus coastal markets. Now the discount action has moved to the Gulf Coast where light sweet crude imports have been pushed out. Today we look at the impact of the changing supply position on crude price differentials.

Rusty’s Introduction

As a general rule here at RBN, we try to avoid hot button issues like environmental policy. We have good friends on all sides of these issues, so our practice has been to steer clear of debates where the relationship between facts and outcomes can be subject to so much interpretation. However, today we make an exception for a blog by Keith Bailey, a highly respected leader in our industry who serves on the boards of MarkWest Energy, Aegis Insurance Services, Cloud Peak Energy, Apco International Oil and Gas, and by the way, was CEO of The Williams Companies when I worked for that company more than a few years back. Today Keith contemplates the issue of climate change from the vantage point of someone who has been around the track in energy markets and thinks deeply about the big picture issues.

The hopes of Marcellus gas suppliers to move more of their product east are playing out in very different ways in metropolitan New York City and in New England. New pipelines to deliver gas from Pennsylvania, West Virginia and Ohio to the Big Apple and its environs already are installed and operating, easing the metro area’s supply crunch and shrinking regional price “basis”. But plans to expand gas-transmission capacity to New England are stalled, and some gas users there are facing another potentially supply-constrained expensive winter. Today we begin a new series looking at why—for the foreseeable future at least--it’s better to be a gas user in New York City than Boston.

Valero is the latest in a long line of US midstream companies to file their Master Limited Partnerships (MLPs) for an IPO – expected early in the New Year. These popular tax efficient entities were created over 25 years ago to encourage energy infrastructure investment. In the last four years the number of MLPs has shot up 50 percent. Today we describe how Valero’s MLP is structured.

Midstream infrastructure companies are investing heavily in facilities to gather, store and transport condensate and natural gasoline range materials in the Utica. The expectation is that production of these light hydrocarbons from the wellhead and gas processing/fractionation plants will increase significantly in 2014. Today we take a deep dive into two company’s plans for condensate and natural gasoline takeaway.

Throughout the three year-long disruption of the US crude oil distribution system caused by rising domestic and Canadian production trying to find a path through the Midwest, the Seaway pipeline reversal project has been a market bellwether of progress to unwind the congestion. In 2Q 2014 the final phase will come online - opening up an additional 450 Mb/d capacity between Cushing and Houston. As the Seaway project has been built out, the crude surplus in the Midwest appears to have moved to the Gulf Coast. Today we detail the impact of Seaway Phase 3 on Gulf Coast crude supplies.

Could the US end up exporting 700 MMb/d of crude to Canada by the end of the decade? Despite static domestic refinery demand and a growing production surplus, Canadian imports of crude increased this year. How could that be? The reason for this apparent anomaly is that East Coast Canadian producers are getting better prices exporting their crude anywhere but the US rather than competing at home against cheaper imports from South Texas and North Dakota. Today we explain some unintended consequences of the US crude export regulations.

Expanding Western Canadian Oil Sands production is currently butting up against pipeline constraints to move the crude to markets in the US and beyond. The result is painful price discounts for producers and an increased inventory of crude in storage at the Edmonton and Hardisty hubs in Alberta. New storage capacity is being added in both hubs to handle the growing volume. Today we detail TransCanada and MEG Energy expansion plans in Edmonton.

Output of naphtha range material such as plant condensates and natural gasoline in the Ohio section of the Utica shale is increasing rapidly as new processing and fractionation capacity in the region comes online. Output of field condensate from the wellhead is also expected to take off in 2014. These light hydrocarbons will be delivered to market by a combination of pipeline, rail and barge infrastructure. Today we look at pipeline infrastructure plans to deliver condensates and natural gasoline to Canada as diluent.

So far in 2013 around 645 Mb/d of new crude oil pipeline capacity has opened up to ship supplies to the Texas Gulf Coast. Early this month (December) line fill starts on the largest new capacity addition to date – the 700 Mb/d Keystone Gulf Coast Pipeline. The new pipeline runs from Cushing to Port Arthur and will carry mostly Canadian heavy crude. Today we wonder if all that crude will find a home.

The first episode in this series described 4 MMb/d of current and planned expansions to crude transportation capacity into the Texas Gulf Coast region (see Handling The Texas Gulf Coast Crude Flood). Our analysis showed that the new incoming light crude capacity will exceed Texas Gulf Coast demand by somewhere north of 0.5 MMb/d by the end of 2015. In episode two we described how some of these excess crude supplies would move east on the reversed Ho-Ho pipeline (see Gulf Coast Crude West to East Flows). In episode three we looked at how shippers could divert supplies away from Texas Gulf Coast congestion (see Texas Gulf Coast Bypass Options). This time we consider the impact of the Keystone Gulf Coast pipeline.

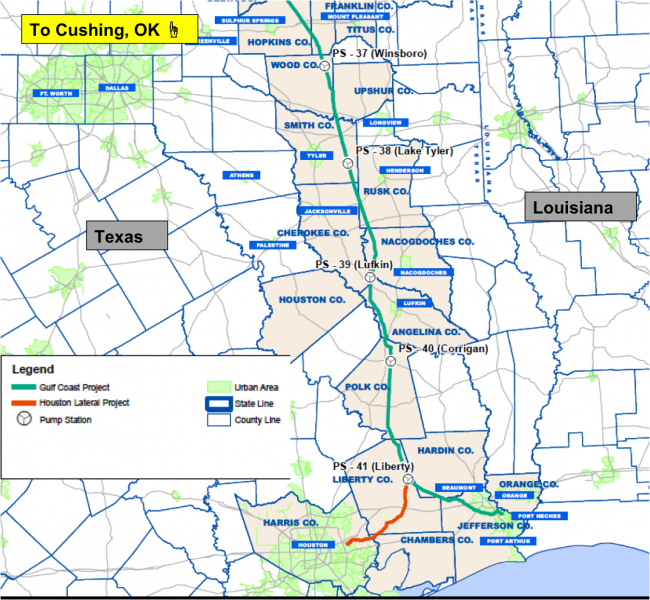

One of the more confusing features of the Keystone Gulf Coast Pipeline is what to call it – the name seems to change in real time. That is probably due to a desire to disassociate the southern Gulf Coast section of the pipeline from delays in permitting the Canada to US Keystone XL pipeline. Owner and operator TransCanada most recently set up a subsidiary to operate the pipeline called Marketlink LLC and it should now apparently more properly be called the Cushing Marketlink Pipeline so we will go with CMP as an abbreviation.

The 36-inch-diameter CMP runs 485 miles from Cushing, OK, to Nederland, TX (see green line on the map below). The line will have an initial capacity of 700 Mb/d with the option to expand to 830 Mb/d. It is almost ready to commence operations but before that can happen it has to be filled with oil – a process known as “line fill”. We described how line fill works and provided a formula to approximate the volume of oil required back in May 2012 (see A Time for Gas A Time For Crude – Part 2). According to that formula CMP requires 3.5 MMBbl of line fill. Marketlink LLC has said the first pipeline deliveries will be made before the end of 2013. The company is also constructing a 48-mile Houston Lateral pipeline (orange line on the map) that will run from the Liberty pumping station to East Houston and should be online by the end of 2014 with 130 Mb/d capacity.

Source: TransCanada Website and RBN Energy (Click to Enlarge)

The initial destination of the CMP is the Sunoco Logistics (part of Energy Transfer Partners) Nederland terminal. We have covered the Nederland terminal in two previous blog posts (see Nederland Crude Wonderland and Nederland Crude Volume Surges). The terminal is located on the Sabine-Neches waterway between Beaumont and Port Arthur, TX and has 22 MMBbl of storage capacity (see map below). The location is in the heart of Beaumont/Port Arthur refining country – home to four large refineries owned by ExxonMobil (Beaumont, 365 Mb/d), Valero (Port Arthur, 310 Mb/d), Total (Port Arthur, 174 Mb/d) and Shell/Saudi Aramco (Motiva 600 Mb/d). The Sabine Neches Waterway connects to the Gulf of Mexico, providing waterborne access to the entire Gulf Coast region. Nederland is about 100 miles East of Houston and 350 miles West of New Orleans.

The golden years of natural gas abundance in which we find ourselves are sparking tremendous enthusiasm among potential users of the fuel, from power generators to major industrial companies, to exporters both current and potential. After all, a trifecta of cheap, abundant, and clean is hard to resist. But the big question is how supply and demand really shake out after everyone’s enthusiasm results in new and growing use of the resource. Is the natural gas industry going to be able to supply all the new demand without prices going up the way they have in the past, most recently hitting double-digits at Henry Hub just five years ago? The first step in order to weigh supply against demand is to have a plausible scenario of what that demand might be. What does it all add up to? So in today’s blog we will see how much demand we should be trying to meet, to be followed later by a next installment to see how producers might meet it.

The northern corn-belt states are winding down from a very wet bumper crop of corn which has required a lot of grain drying, fired by propane. That has translated into a shortage of propane supplies – so much so that seven governors recently issued emergency orders to expedite propane deliveries to their states. Now, with about three weeks left before the official onset of winter (and it feels like winter already), 2013 Midwestern propane problems should be behind us. But what about next year? In 2014, Cochin pipeline – one of the most significant traditional sources of propane for the region goes away. Kinder Morgan (current owner and operator of Cochin) is reversing the system and turning it into a diluent pipeline. Volumes of propane previously delivered by Cochin must come from somewhere else. Today we’ll continue our series looking at upper Midwest propane and how the region is likely to adjust in the post-Cochin market.