The bases are loaded for another 2 MMb/d of pipeline capacity to bring additional crude supplies to the Texas Gulf Coast by the end of 2014. The majority of that payload will likely be light sweet crude from tight oil formations, a.k.a., shale. As the flood of crude headed to Texas passed through the Midwest over the past two years, prices at Cushing and points north were heavily discounted versus coastal markets. Now the discount action has moved to the Gulf Coast where light sweet crude imports have been pushed out. Today we look at the impact of the changing supply position on crude price differentials.

This is Part 1 of a two-part review of Gulf Coast crude price differentials that extends a series on the topic that we started back in November (2013). The first episode in the series described 4 MMb/d of current and planned expansions to crude transportation capacity into the Texas Gulf Coast region (see Handling The Texas Gulf Coast Crude Flood). Our analysis showed that the new incoming light crude capacity will exceed Texas Gulf Coast demand by somewhere north of 0.5 MMb/d by the end of 2015. In episode two we described how some of these excess crude supplies would move east on the reversed Ho-Ho pipeline (see Gulf Coast Crude West to East Flows). In episode three we looked at how shippers could divert supplies away from Texas Gulf Coast congestion (see Texas Gulf Coast Bypass Options). Episode four looked at progress bringing TransCanada’s Keystone XL Gulf Coast extension (a.k.a, Cushing Marketlink Pipeline (CMP)) online (see Keystone Marketlink Comes to Texas). Episode five looked at the impact of the twin Seaway Pipeline from Cushing to Freeport expected online during the second quarter of 2014 (see Impact of the Seaway Expansion). Now we’ll get into what happens to price differentials as new crude supplies come flooding into Texas in the next six months.

Forecasting prices for tomorrow is like gambling – only fun if you don’t mind losing money. And the odds of being right get worse the further out the predictions go. So our intent here is to concentrate on price differentials – the spread between key crude benchmarks rather than getting into absolute price levels. We start with a review of what has happened since 2012 and then offer some scenarios for how things might turn out next year (2014). Buckle up.

Recap 2012

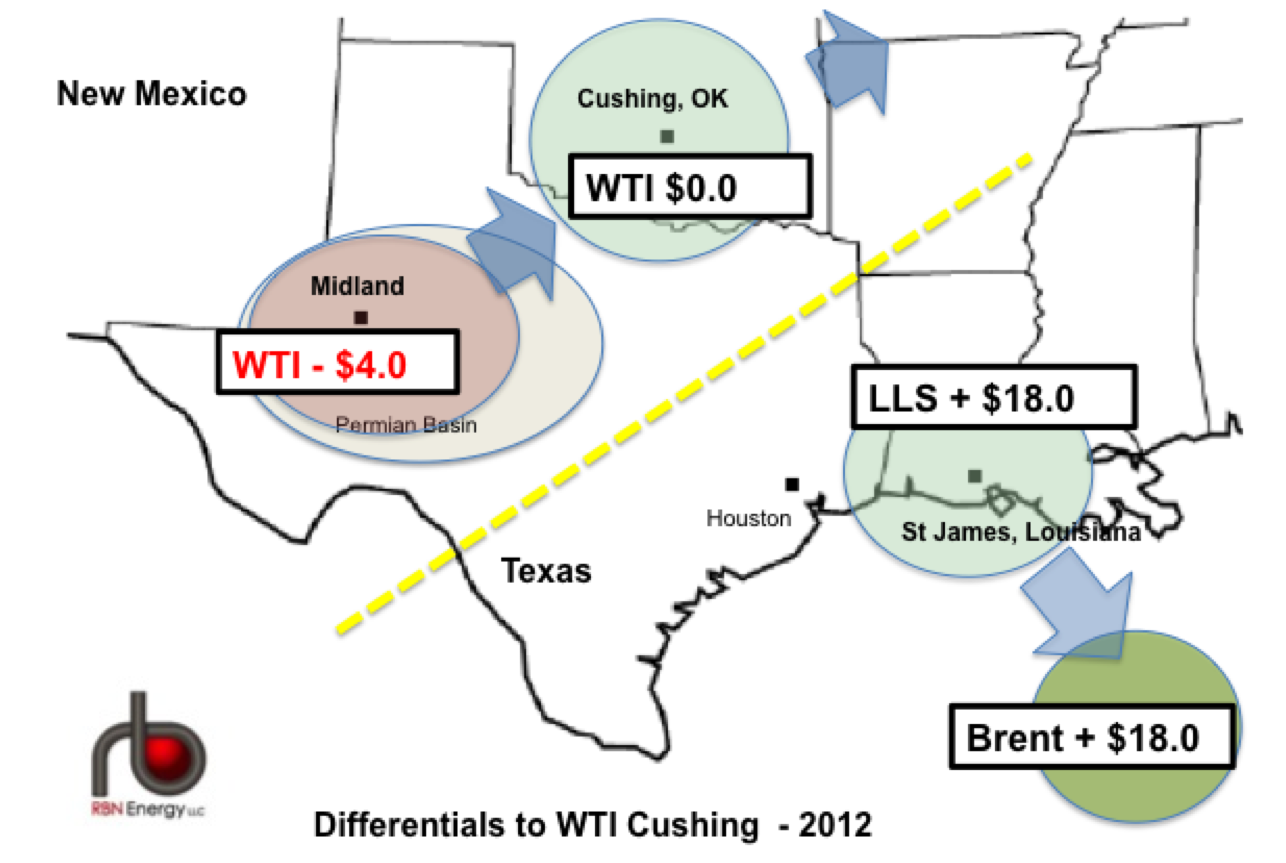

Figure 1 below shows average differentials for key benchmark light sweet crude grades at the Gulf Coast during 2012. The prices are averages for the year versus the West Texas Intermediate (WTI) NYMEX benchmark price at Cushing - set to $0/Bbl. Recall that during 2012 surging crude production in North Dakota and Canada exceeded demand in the Midwest and supplies started backing up at Cushing, OK because there was very little pipeline capacity from the Midwest to the Gulf Coast (where 50 percent of US refining capacity resides). Because of this logjam a stockpile of crude built up at Cushing and inland domestic prices based on WTI were discounted heavily versus Gulf Coast supplies priced against the international benchmark Brent crude (see The Seven Gates of Hell for WTI Traders). Domestic light sweet crude grades sold at the Gulf Coast – represented by Light Louisiana Sweet (LLS) in our diagram - traded at the higher international levels. In 2012 both Brent and LLS averaged $18/Bbl above the discounted WTI “stranded” at Cushing. The dotted yellow line on the chart indicates the pipeline ‘capacity constraint’ boundary that split Cushing and Gulf Coast pricing markets at that time. You can think of that yellow line as separating zones of domestic and international pricing along the Gulf Coast region.

Figure 1 - Source: RBN Energy

Prices for WTI are set both at Cushing, OK – the gateway to Midwest refineries – as well as at Midland, TX, closer to the Permian Basin production region. During 2012, Midland prices for WTI were discounted by an average of $4/Bbl to WTI at Cushing because of capacity constraints on the pipelines between Midland and Cushing (caused by surging crude production in the Permian Basin). Until new pipelines opened up from the Permian direct to Houston in 2013, WTI had to travel to market from Midland to Cushing - into an already oversupplied Midwest market (see New Adventures of Good Ole Boy Permian).

Comments

With light imports (>34 API) of between 400-500 MBbl/d still going into the northeast, and less than 100 MBbl/d of that coming from Canada, why isn't the excess light being shipped around the coast to those refineries. My understanding that relative to pipelines, ship transport was almost negligible in cost/bbl. Is it due to loading infrastructure constraints, or legacy contracts those refiners have?

In reply to PADD I and the LLS Brent disconnect by salmonfries

Crude shipped from the Gulf Coast to the East Coast must travel on Jones Act vessels that are expensive compared to international freight - perhaps $5/Bbl - narrowing the arbitrage opportunity

My predictions for Winter/Early Spring 2014.

During 2008-2012, Billions of dollars were poured into structures created by banks (ex: ETF physically backed by Oil) and after Lehman collapse, oil was a reasonable price and bets in the oil curve were stable on the rise. Production was rising, prices were higher, the only physical limit to this trade was storage but storage capacity has rapidly emerged too. A favorable market structure for carry has emerged from this environment.

Oil has been pumped/trucked/barged to be stored and delivered later under the WTI contract at Cushing’s facilities by Oil Companies’ trading arms, Banks and Oil middlemen.

But with the emergence of shale-oil fields far away from pipelines and big discounts between Cushing and fields, Refiners, Midstream companies and Producers have learned to use Rail to by-pass Cushing thus, often forcing better basis. Crude By-Rail has emerged and we have learned that a single 50,000 barrels rail cargo passing Cushing could move the Brent/WTI spread by more than 1$ overnight.

Market has changed, Basis differentials for producers have fallen sharply and was followed by a fall in the WTI back months of the curve, (no longer creating incentives to carry the oil) and inventory selling in Cushing, Ok.

Now imagine what will be the impact of ”15 units trains per day” debotlnecking at Cushing, OK: Welcome to 2014 !

First crude from Cushing Market Link (CML) will flow from January 2, 2014.

First, any debottlenecking pipeline needs a “line fill”, this initial amount required for Cushing Market Link 830KPD (Part of Keystone South Leg) is 3.9 MMBBLS. Crude will have to come from cushing storage first and compete existing supplies feeding Midwest refineries. Curve and pipeline expansions are now telling us that a big change is coming in Oil pricing sooner, faster and bigger than what we might think.

WTI, Brent Curve and Brent/WTI curve.

WTI is aggressively showing selling at Cushing in the fronth-month, WTI Downward Curve shows no incentives to carry oil and deliver for deferred months.In the near-term, Game is over for many middlemen engaged in the storage business in Northern Oklahoma.The WTI Curve is showing compelling evidence that CML isn’t under-subscribed this winter.Brent/WTI Curve is showing bearish expectations for Winter 14′, Spring 14′.Spreads

Local USGC crudes (Eagle Ford, Permian, Argus LLS will feel the heat from the WTI selling and oil movements to the USGC.It sounds great for USGC refiners but less good for Texas producers or Midwest Refiners.WCS/WTI will be firmer, the pipeline is designed to flow to the USGC on Heavy Crude, Canadian Producers are likely to by-pass Cushing and store directly in the USGC.Brent/WTI is to watch, Like a Swiss-based oil researcher suggests: mounting domestics supply reaching the USGC by pipe/rail is capping the upside potential in the Brent/WTI spread. However the ongoing WTI inventories liquidation at Cushing, OK supports Brent/WTI. By March, notwithstanding international turmoil, Brent/WTI could switch back to the $0 -5$ low-end.This is what I see in my frozen crystal ball, it's getting very cold here. Global Cooling :)

Merry Christmas, Ho Ho Ho Houston and Happy Holidays to all RBNers, Simon