The popularity of weather derivatives has ebbed and flowed since their introduction in the late 1990s but trading activity has rebounded in recent years as the trading community has increasingly begun to reassess the need to hedge weather-related risks — everything from high temperatures and rainfall levels to power prices and cooling demand. In today’s RBN blog, we examine the role of weather derivatives, how they are used to hedge risk, and why they may be becoming increasingly important to the energy industry.

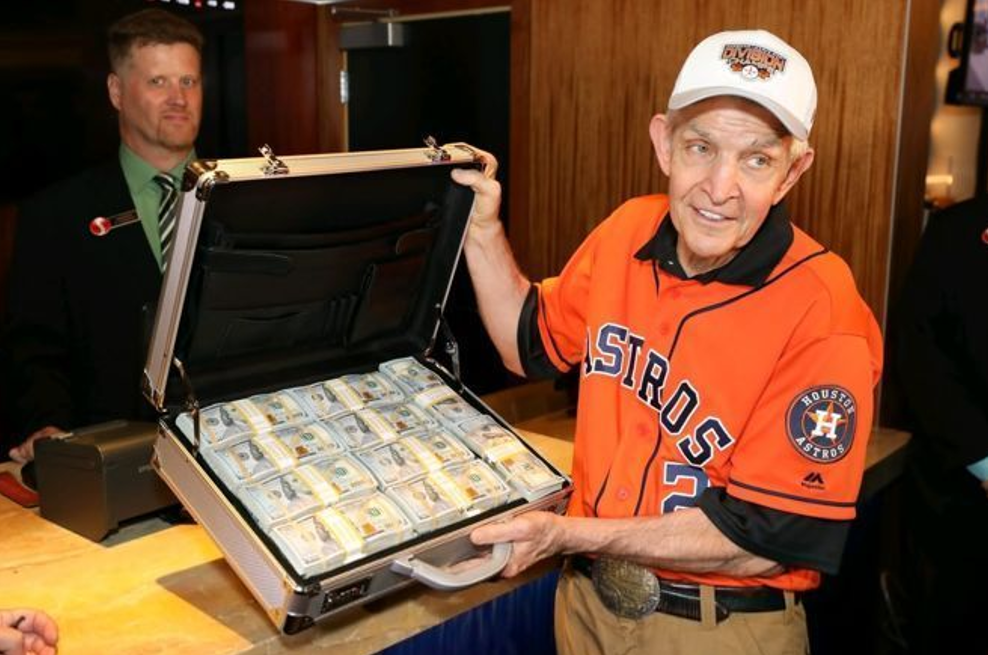

Many of you are probably familiar with Jim McIngvale (see photo below), the Houston-area celebrity known as “Mattress Mack” and the owner of Gallery Furniture. He gained national attention back in 2017 when he opened his stores to those affected by Hurricane Harvey, but he’s also attracted a lot of notoriety for his big-dollar bets on college and professional sports. We assume that Mattress Mack enjoys a good wager and the publicity that comes with it, but there’s often a bottom-line strategy behind his bets. In perhaps the most newsworthy example, his stores ran a promotion back in 2022 that said if you bought at least $3,000 in furniture, you’d get it for free if the Houston Astros won the World Series. That potentially expensive proposition became a reality when the Astros beat the Philadelphia Phillies in six games, but Mattress Mack was covered because the downside risk of that promotion (giving away a lot of free furniture) was hedged by his bet on the Astros to win the Series. In the end, he won a reported $75 million in bets (on $10 million wagered), earned himself and his store a load of free publicity, and more than made up for all the free furniture he ended up giving away.

Houston’s Jim McIngvale, Better Known as “Mattress Mack.”

Weather derivatives, which have been around for about 30 years, work in much the same way as the example above, so let’s start with some basics. Weather derivatives are financial contracts that are linked to one or more specific, measurable variables, such as average temperatures, wind speeds and cumulative rainfall. They are financially settled using data from the National Weather Service (NWS) or other trusted, third-party providers. Perhaps most importantly, there is no physical damage required to trigger a payout (unlike insurance); the only thing that matters is whether the specific conditions of a derivative have been met. For example, a business impacted by the aforementioned Hurricane Harvey would have had to document any actual damage and file a claim for its insurance to pay out but could have quickly collected on any derivatives tied to above-average rainfall for that month. (Harvey dropped 40-50 inches of rain on Houston in August 2017, well above the monthly average of 5.4 inches.)

About the song

“Chances Are” was written by Robert Allen with lyrics by Al Stillman. It appears as the first song on side one of Johnny Mathis’ 1958 compilation album, Johnny’s Greatest Hits. Released as a single in August 1957, it went to #1 on the Billboard Most Played by Jockeys and #5 on the Billboard Hot 100 Singles charts. Music critic Robert Christgau wrote that the song “projected an image of egoless tenderness, an irresistible breath of sensuality.” It was inducted into the Grammy Hall of Fame in 1998 and was selected for inclusion in the National Recording Registry of the Library of Congress in 2024. The record is close to perfection on every level. Mathis’ smooth vocals, Ray Coniff’s lush arrangements and Dick Hyman’s perfect piano arpeggios laying on top of the chord changes make for a stellar listening experience. It was recorded at Columbia 30th Street Studio in New York City in June 1957 and produced by Mitch Mitchell and Al Ham. Personnel on the record were: Johnny Mathis (vocals), the Ray Coniff Orchestra (orchestrations) and Dick Hyman (piano).

Johnny’s Greatest Hits is a compilation album of singles Mathis recorded at Columbia 30th Street Studio in New York City between 1956 and 1958. Produced by Mitch Mitchell and Al Ham, the album was released in March 1958 and went to #1 on the Billboard 200 Albums chart. The album was compiled from 12 previously released Mathis Singles.

Johnny Mathis is an American singer whose catalog focuses on romantic American Standard songs. He cites Lena Horne, Nat King Cole and Bing Crosby as his influences. He started singing while attending George Washington High School in San Francisco, where he was a star athlete. He then attended San Francisco State College on an athletic scholarship. He started singing in San Francisco nightclubs in 1955 and released his debut studio album on Columbia Records: Johnny Mathis: A New Sound in Popular Music, in 1956. He has released 73 studio albums, three live albums, 30 compilation albums and 113 singles. He is in the Grammy Hall of Fame, the Great American Songbook Hall of Fame, has a Grammy Lifetime Achievement Award, and a star on the Hollywood Walk of Fame. At 89, Mathis has retired from performing and gave his last concert at the Bergen Performing Arts Center in Englewood, New Jersey, in May.

Comments

Is there a figure missing from this blog? The text says:"The recent surge in trading (far-right blue bar in Figure 1) coincides with this year’s spike in European natural gas prices, which was caused in part by lower renewable output (along with geopolitical tensions and low storage levels)." But, there is no figure with a blue bar.

In reply to Chances Are by Ian MacLean

Thank you for reading and catching that error. The text has been updated.