The Marcellus/Utica has massive natural gas reserves, but daily, weekly and annual production in the three-state shale play is limited by three key factors: in-region demand, takeaway capacity and gas prices. In recent years, the basin’s output has been rangebound between 34 and 36 Bcf/d and Appalachian producers see only modest gains in 2025. But a handful of pipeline projects and rising gas demand from power generators suggest the Marcellus/Utica may finally be on the verge of a production breakout. In today’s RBN blog, we discuss the leading E&Ps’ production forecasts for 2025 and the prospects for considerably higher output by the end of this decade.

NATGAS Billboard is a daily, early morning email and report that provides an up-to-the-minute view of the natural gas market outlook, including storage injections/withdrawals and price. Billboard’s models incorporate pipeline flow data, weather models, electricity demand data and more.

This is the third blog in our series on recent upstream and midstream activity in the Marcellus/Utica. In Part 1, we noted that while the shale play’s gas production soared from less than 2 Bcf/d to more than 33 Bcf/d in the 2010s, its output through the first half of the 2020s has stayed close to flat, averaging about 35 Bcf/d over that period — ~24 Bcf/d from the NGL-rich “wet” Marcellus/Utica in southwestern Pennsylvania, northern West Virginia and eastern Ohio and ~11 Bcf/d from the “dry” Marcellus in northeastern Pennsylvania. (Note: Only about half the gas emerging from wells in the parts of the Marcellus/Utica that we generally refer to as “wet” includes significant volumes of NGLs; the other half is dry.) The primary hurdle to further growth has been takeaway capacity; there hasn’t been enough space on the pipelines out of Appalachia to move more of the shale play’s gas to demand centers hundreds of miles away.

In Part 2, we discussed a long list of recently completed, under-construction and planned pipeline projects that provide — or soon will provide — additional egress. These include the 2-Bcf/d Mountain Valley Pipeline (MVP), which started up in June 2024; a host of capacity-enhancement projects along and near the Transco pipeline system that will enable more Marcellus/Utica gas to flow into the Southeast; and the possible construction of the Borealis Pipeline across Ohio (and related improvements to the Texas Gas Transmission system) that would allow more gas to flow south/southwest to Louisiana. We also looked at the three primary drivers for Appalachian gas demand growth in the second half of the 2020s, namely higher in-basin power demand from new data centers, expanding Gulf Coast LNG export volumes, and rising demand for gas in the fast-growing Southeast. Separately, in Family Affair, we discussed Kinder Morgan’s Mississippi Crossing and South System Expansion 4 projects, which would let more Marcellus/Utica gas flow into the Deep South.

Today, we shift our focus to (1) what the leading E&Ps in the nation’s largest gas production area have been saying about their 2025 production and longer-term prospects, and (2) how much production growth the Marcellus/Utica as a whole might experience as gas demand from power generators and other big customers increases.

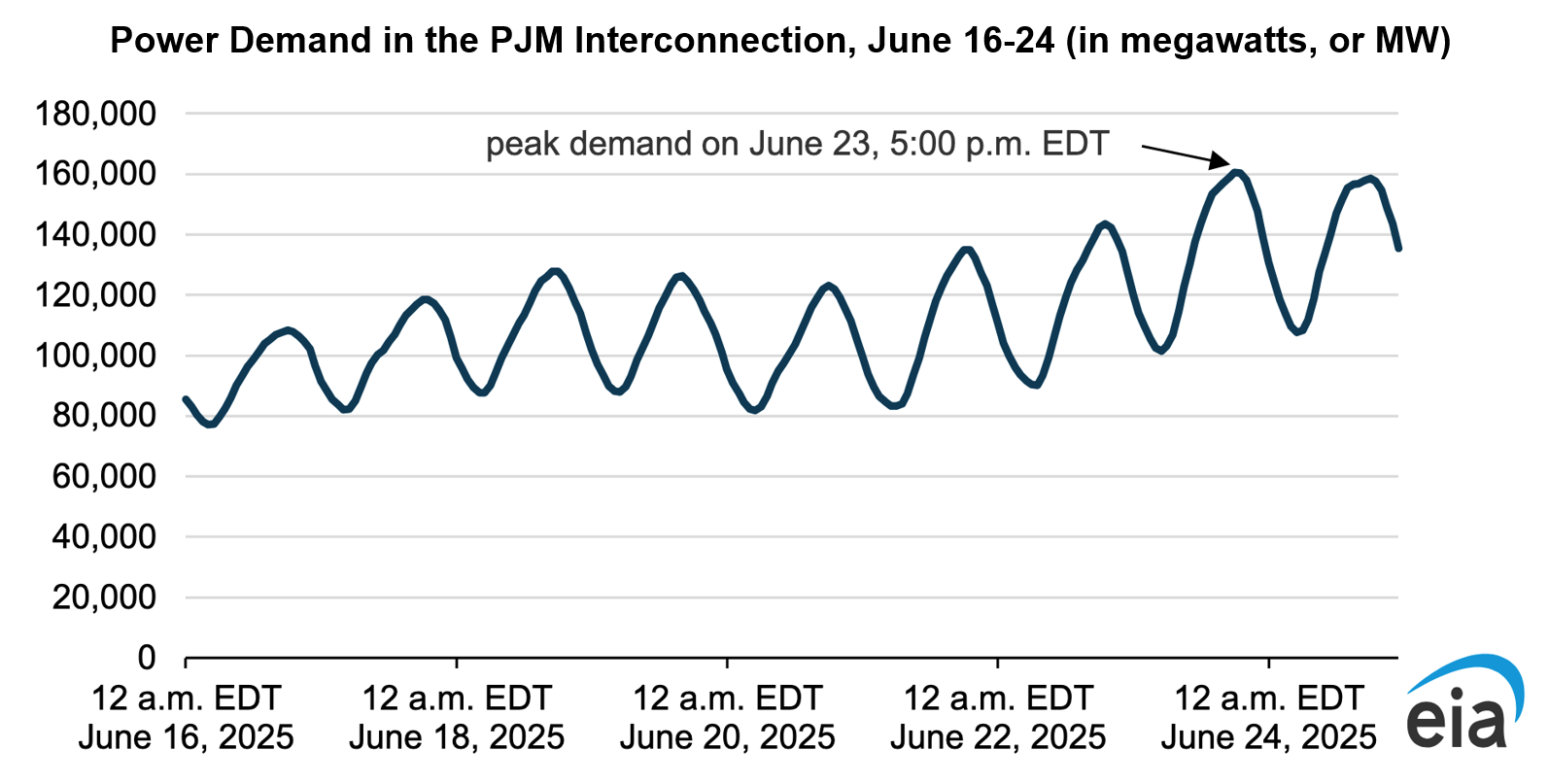

Before we begin, we should note that gas demand in the Eastern U.S. soared the week of June 22, when New England, the Mid-Atlantic states, the Southeast and the Midwest suffered through their first major heat wave of 2025. The Energy Information Administration (EIA) said the PJM Interconnection, the largest wholesale electricity market in the country (reaching from northern Illinois to New Jersey to northeastern North Carolina), experienced near-record demand of more than 160,000 megawatts (MW) on June 23 (see Figure 1 below), and that gas-fired plants provided 44% (or ~71,000 MW) of the power being consumed then. Electricity demand in New England approached record levels the following day, with gas plants providing 47% of the power.

Figure 1. Power Demand in the PJM Interconnection, June 16-24 (in megawatts, or MW). Source: EIA

About the song

“Don't Stop Believin’” was written by Journey members Steve Perry, Jonathan Cain and Neal Schon. The song appears as the first song on side one of Journey’s seventh studio album, Escape. It was recorded at Fantasy Studios in Berkeley, CA, and produced by Kevin Elson and Mike Stone. Released as a single in October 1981, the song went to #9 on the Billboard Hot 100 Singles chart. It has sold more than 7 million digital downloads in the U.S., placing it in the Top 10 of digital song downloads. It has been certified Platinum by the Recording Industry Association of America (RIAA). Personnel on the record were: Steve Perry (lead vocals), Ross Valory (bass, backing vocals), Jonathan Cain (keyboards, backing vocals), Neal Schon (guitars, backing vocals), and Steve Smith (drums, percussion).

Escape was recorded between April and June 1981 and released in July 1981. It went to #1 on the Billboard 200 Albums chart and has yielded four Top 20 hit singles. It has been certified Diamond (10 million copies sold) by the RIAA. It was the first album with keyboardist Jonathan Cain, who replaced founding member Gregg Rolie.

Journey is an American rock band formed in San Francisco in 1973. Eighteen members have passed through its ranks since its formation. They have released 15 studio albums, five live albums, 11 compilation albums, a soundtrack album, two EPs and 52 singles, and have sold more than 100 million records worldwide. Journey was inducted into the Rock and Roll Hall of Fame in 2017. The current iteration of the band, featuring longtime members guitarist Neal Schon and keyboardist Jonathan Cain, is joined by vocalist Arnel Pineda, bassist and backing vocalist Todd Jensen, keyboardist and backing vocalist Jason Derlatka, and drummer and backing vocalist Deen Castronovo. They continue to record and tour.