Marcellus/Utica natural gas production grew by leaps and bounds in the 2010s, but the pace of growth has slowed dramatically in recent years, mostly due to takeaway constraints. Finally, the prospects for renewed growth are improving. New pipeline capacity out of Appalachia is coming online — especially to the booming Southeast, and maybe the Gulf Coast too. New LNG export capacity is about to be commercialized. And a lot of new gas-fired generating capacity — much of it tied to planned data centers — is under development within (or very near) the Marcellus/Utica region. In today’s RBN blog, we examine the three big gas-demand drivers behind the shale play’s impending renewal.

The NATGAS Production Tracker - Texas provides a DAILY update of natural gas production in Texas the New Mexico side of the Permian Basin. Quickly and easily view today’s supplies in the Lone Star state and download the full historical table when you need it.

As we said in Part 1, the Marcellus/Utica is by far the most prolific gas production area in the U.S., accounting for about one-third of the nation’s daily output. The shale play’s gas production soared from less than 2 Bcf/d to more than 33 Bcf/d over that decade, but its output through the first half of the 2020s has stayed close to flat, averaging about 35 Bcf/d over that period — ~24 Bcf/d from the NGL-rich “wet Marcellus/Utica” in southwestern Pennsylvania, northern West Virginia and eastern Ohio and ~11 Bcf/d from the “dry Marcellus” in northeastern Pennsylvania. (Note: Only about half the gas emerging from wells in the parts of the Marcellus/Utica that we generally refer to as “wet” includes significant volumes of NGLs; the other half is dry.)

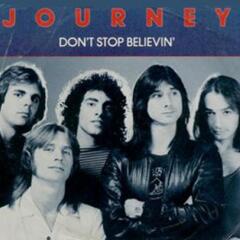

The primary hurdle to further growth has been takeaway capacity; there hasn’t been enough space on pipelines out of Appalachia to move more of the shale play’s gas to demand centers hundreds of miles away. That’s been changing, however, mostly due to the June 2024 startup of the 2-Bcf/d Mountain Valley Pipeline (MVP; aqua line in Figure 1 below) from northern West Virginia to Transco Station 165 in south-central Virginia and the advancement of several capacity-expansion projects on or near Transco itself. A few of these projects (Regional Energy Access, Southside Reliability Enhancement Project, Carolina Market Link, and Southeast Energy Connector) came online over the past 18 months, and others (Commonwealth Energy Connector, MVP Southgate, Southeast Supply Enhancement, and Alabama Georgia Connector) will follow later this year and in 2027-28. (See Part 1 for details.)

Figure 1. MVP, Transco and Related Expansion Projects. Source: RBN

About the song

“Don't Stop Believin’” was written by Journey members Steve Perry, Jonathan Cain and Neal Schon. The song appears as the first song on side one of Journey’s seventh studio album, Escape. It was recorded at Fantasy Studios in Berkeley, CA, and produced by Kevin Elson and Mike Stone. Released as a single in October 1981, the song went to #9 on the Billboard Hot 100 Singles chart. It has sold more than 7 million digital downloads in the U.S., placing it in the Top 10 of digital song downloads. It has been certified Platinum by the Recording Industry Association of America (RIAA). Personnel on the record were: Steve Perry (lead vocals), Ross Valory (bass, backing vocals), Jonathan Cain (keyboards, backing vocals), Neal Schon (guitars, backing vocals), and Steve Smith (drums, percussion).

Escape was recorded between April and June 1981 and released in July 1981. It went to #1 on the Billboard 200 Albums chart and has yielded four Top 20 hit singles. It has been certified Diamond (10 million copies sold) by the RIAA. It was the first album with keyboardist Jonathan Cain, who replaced founding member Gregg Rolie.

Journey is an American rock band formed in San Francisco in 1973. Eighteen members have passed through its ranks since its formation. They have released 15 studio albums, five live albums, 11 compilation albums, a soundtrack album, two EPs and 52 singles, and have sold more than 100 million records worldwide. Journey was inducted into the Rock and Roll Hall of Fame in 2017. The current iteration of the band, featuring longtime members guitarist Neal Schon and keyboardist Jonathan Cain, is joined by vocalist Arnel Pineda, bassist and backing vocalist Todd Jensen, keyboardist and backing vocalist Jason Derlatka, and drummer and backing vocalist Deen Castronovo. They continue to record and tour.