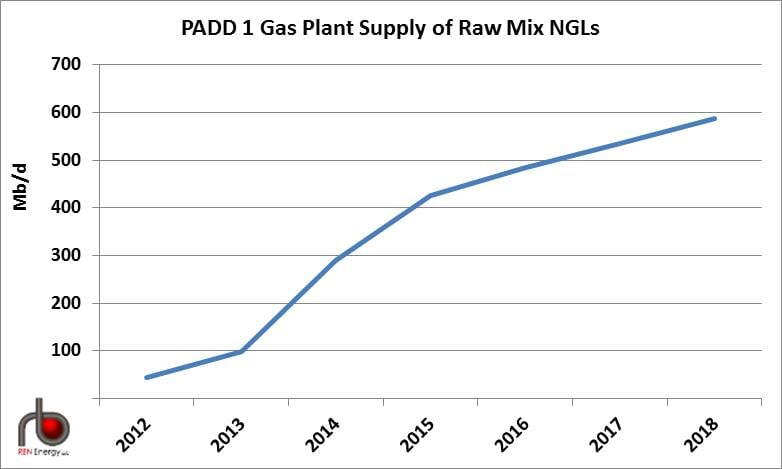

Last week we started a blog series looking to answer the question - Are we likely to run into storage issues with NGLs while we are waiting for infrastructure and demand side projects such as export terminals and petrochemical facilities to be built out? Today we are going to take a deeper look at PADD 1 NGL market dynamics where gas plant production of NGLs is expected to grow from 63 Mb/d as reported by the EIA for February 2013, to over 585 Mb/d in 2018. We’ll assess growing supply and demand mismatches and how production will move between regions. Today we will lay the foundation for our PADD 1 NGLs storage picture.

Historically, NGL production from PADD 1 has been minimal, and the need for storage has also been relatively low to keep the market balanced, but as we previously discussed in the Big Surge Comes to Whoville – Northeast NGLs to Increase Six Fold between now and 2015 nearly 4.7 Bcf/d of additional natural gas processing capacity, along with 500 Mb/d of fractionation capacity and 500 Mb/d of NGL pipeline takeaway capacity are due to come online in the Northeast to support growing Utica and wet Marcellus production. Once this infrastructure comes online, by 2015 NGLs production from the Appalachian Basin could exceed of 400 Mb/d (see chart below).

Note: Data includes PADD 1 plus Ohio

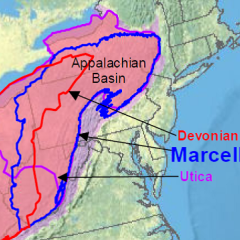

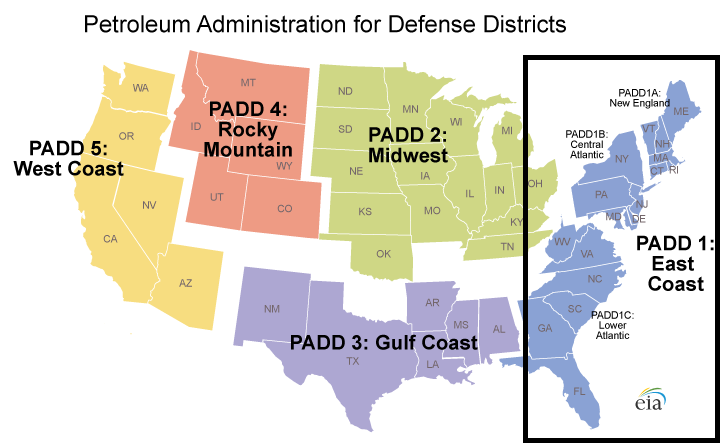

While PADD 1 covers the entire East Coast (see the box on the map below), NGL production in the region all comes from the Northeast District that the EIA defines as Appalachian No. 1, which includes the State of West Virginia and those parts of the States of Pennsylvania and New York not included in the East Coast District. The EIA’s East Coast District in PADD 1 includes several counties in New York and Pennsylvania. Crystal Clear!

Source: EIA

To confuse matters even further, for this analysis (as footnoted on the PADD 1 Gas Plant Supply chart above), we will be including NGL gas plant production from Ohio in PADD 1, despite Ohio technically being in PADD 2. Given the close proximity and interconnectivity of the Ohio plants with PADD 1, infrastructure production from the Ohio plants will compete for the same demand sources and takeaway capacity as the PADD 1 NGL production.

About half the NGL production growth indicated above will be ethane. Historically, no ethane has been produced in the region due to lack of local demand and takeaway capacity. In the future, ethane from the region will meet demand from petrochemical facilities in Canada and Europe, and to some extent the Gulf Coast, and also insure that the residue natural gas from processing plants can meet pipeline BTU content specifications. For more on why ethane will need to be produced in this region see Big Surge Comes to Whoville – Northeast NGLs to Increase Six Fold.

Ethane

By 2015 over 200 Mb/d of ethane could be produced from the region, but no incremental local demand will have developed by that point. Consequently the produced ethane will be leaving the region via pipelines planned and under construction by Enterprise and Sunoco/MarkWest. Sunoco/MarkWest’s Mariner West Project is the first due online, with an expected in service date of July or August 2013. The Mariner West Project is a 50 Mb/d ethane-only pipeline to move ethane from the Houston fractionator in Western Pennsylvania to the Sarnia, Ontario petrochemical market. Also proposed to move purity ethane, and possibly propane too (given Enterprise’s recent open season announcement) is Enterprise’s 190 Mb/d ATEX pipeline which will move products from the Appalachian Basin to the Texas Gulf Coast. In addition to the ethane only pipelines just mentioned Sunoco and MarkWest have also proposed the Mariner East project to move ethane and propane to the eastern seaboard for export. In total these three projects provide for 280 Mb/d of ethane takeaway capacity. For greater detail on these projects see Too Much Marcellus/Utica NGL Pipeline Capacity? Or not enough? A final proposed option for moving ethane out of the region which was recently formalized between Williams and Boardwalk is the proposed Bluegrass pipeline which would move 200 Mb/d of raw mix from the Northeast to the U.S. Gulf Coast starting in late 2015.