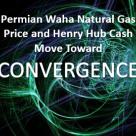

Over the past three months, spot-market prices at Henry Hub and Permian Waha have been steadily converging. As shown in the left graph below, Waha March gas traded at a mere $0.08/MMBtu (outright price), while Henry Hub fetched $4.12/MMBtu—creating a staggering basis spread of $4.04/MMBtu.

Analyst Insights

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

By Martin King - Friday, 6/13/2025 (3:15 pm)

For the week of June 13, Baker Hughes reported that the Western Canadian gas-directed rig count reached 47, an increase of two (blue line and text in left hand chart below) and eight less than one year ago.

By Jeremy Meier - Friday, 6/13/2025 (3:00 pm)

US oil and gas rig count declined for the seventh consecutive week, falling to 555 for the week ending June 13 according to Baker Hughes data. Rigs declined week-on-week in the Permian (-2), Anadarko (-1) and All Other (-1), while no basins posted gains.

By TJ Braziel - Wednesday, 6/11/2025 (3:15 pm)

Report Highlight: Crude Oil Billboard

Refinery activity surged last week, with total net inputs climbing 230 Mb/d to 17.225 MMb/d, the highest level since late 2019. Gross inputs rose by 170 Mb/d, pushing utilization up nearly a full point to 94.3%, with PADDs 2 and 5 leading the gains.

By Martin King - Wednesday, 6/11/2025 (3:00 pm)

Re-exports of Canadian heavy crude oil are estimated to have been 35 Mb/d in May 2025 (rightmost stacked columns in chart below), a drop of 121 Mb/d from April, 64 Mb/d less than a year ago, and an eight-month low based on tanker data compiled by Bloomberg and historical export data released by t

By Christine Groenewold - Wednesday, 6/11/2025 (1:30 pm)

Report Highlight: U.S. Propane Billboard

The EIA reported that total U.S. propane/propylene inventories had a build of 4 MMbbl for the week ended June 6, the second largest week on week increase in at least the past 10 years.

By Liz Dicken - Wednesday, 6/11/2025 (11:30 am)

Report Highlight: Crude Voyager

Total crude oil exports from the U.S. Gulf Coast (USGC) for the month of May dropped to 3.46 MMb/d, the lowest monthly volume since January 2023. This decline continues a broader downtrend of crude exports in the last few months.

By Liz Dicken - Tuesday, 6/10/2025 (3:30 pm)

Report Highlight: TradeView Report

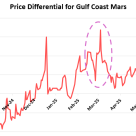

Just two weeks ago, the price differential for Mars sour crude plummeted to trade at discounts to NYMEX-CME Domestic Sweet (DSW) — the commonly quoted prompt month futures contract price of crude oil.

By Lisa Shidler - Tuesday, 6/10/2025 (11:30 am)

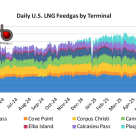

Report Highlight: LNG Voyager

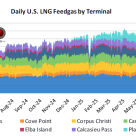

U.S. LNG feedgas demand slipped last week to its lowest level since mid-December, driven by ongoing maintenance at Sabine Pass and Cameron.

By John Abeln - Monday, 6/09/2025 (3:30 pm)

Report Highlight: NATGAS Permian

Overall outflows of natural gas from the Permian Basin were up slightly last week, with higher outflows to the West. Outflows to the West averaged 2.25 Bcf/d, up 0.08 Bcf/d week-on-week. Higher supply receipts were seen on El Paso Pipeline particularly in the back half of the week.

By Jeremy Meier - Friday, 6/06/2025 (3:15 pm)

US oil and gas rig count fell for the sixth consecutive week, falling to 559 for the week ending June 6 according to Baker Hughes data, a decline of four vs. a week ago. Rigs were added in the Haynesville (+2), while the Permian (-3), Anadarko (-2) and Eagle Ford (-1) all posted declines.

By Martin King - Friday, 6/06/2025 (1:45 pm)

For the week of June 6, Baker Hughes reported that the Western Canadian gas-directed rig count rose two to reach 45 (blue line and text in left hand chart below) and nine less than one year ago.

By Jason Lindquist - Friday, 6/06/2025 (9:45 am)

Report Highlight: Hydrogen Billboard

Senate Republicans should keep the 45V tax credit for clean hydrogen in place until at least 2029, and preferably longer, according to a letter signed June 5 by more than 200 companies and industry groups, including the American Petroleum Institute (API), the U.S.

By Martin King - Thursday, 6/05/2025 (2:00 pm)

Alberta’s crude oil output in April 2025 reached a record high for the month at 4.0 MMb/d (rightmost blue column and text in chart below), 0.1 MMb/d above one year ago (itself the prior record holder for April), down 0.2 MMb/d from March, and marks the seventh consecutive month of oil production

By Christine Groenewold - Wednesday, 6/04/2025 (3:00 pm)

Report Highlight: U.S. Propane Billboard

The EIA reported that total U.S. propane/propylene inventories had a build of 6.8 MMbbl for the week ended May 30.

By Liz Dicken - Wednesday, 6/04/2025 (2:45 pm)

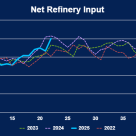

Report Highlight: Crude Oil Billboard

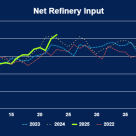

According to the latest Weekly Petroleum Status Report released by the EIA, net refinery input surged by 670 Mb/d for the week ending May 30 to nearly 17.0 MMb/d (blue solid line below), increasing capacity utilization by 3.2% to 93.4%.

By Kristen Holmquist - Wednesday, 6/04/2025 (2:30 pm)

As a follow up to yesterday’s blog, Hey, Hey, What Can I Do, the ban on exports of ethane by Enterprise is already in effect. Enterprise Products Partn

By Lisa Shidler - Tuesday, 6/03/2025 (11:45 am)

Report Highlight: LNG Voyager

U.S. LNG feedgas demand fell by 0.57 Bcf/d last week, primarily due to ongoing maintenance.