Given all the recent attention, you’d think the prospects for carbon-capture project development are fantastic. In the U.S., last year’s Inflation Reduction Act (IRA) featured significant increases in the 45Q tax credit for carbon sequestration, improving the economics for a wide range of carbon-capture projects. On a global level, it seems clear that efforts to reduce greenhouse gas (GHG) emissions and reach a net-zero world will continue for a long time to come. Nearly every plan to reach that target includes a significant reliance on carbon capture, with the International Energy Agency (IEA) forecasting that 7,600 million metric tons per annum (MMtpa) of carbon dioxide (CO2) — that’s 7.6 gigatons per year — will need to be captured and sequestered by 2050. We are a long way from those levels, given that most estimates put global carbon-capture capacity at a little more than 40 MMtpa today, or less than 1% of what the EIA thinks we’ll need in less than 27 years. In today’s RBN blog, we look at the main factors holding back the wider commercialization of carbon-capture initiatives in the U.S.

First, let’s start with a look at the bright side. The pace of development in the carbon-capture industry has ticked up significantly in the last couple of years, with 244 MMtpa of capacity under development and 61 facilities added to the worldwide project pipeline in 2022, according to the Global CCS Institute’s latest annual report. But as has been the case elsewhere, the number of CCS projects advancing from concept to financing, construction and commercial operation has been limited. According to the institute’s facilities database, there are just 14 carbon-capture projects in commercial operation globally. (To be considered a commercial facility, the CO2 must be captured and transported for permanent storage as part of an ongoing commercial operation. Among other things, pilot and demonstration facilities may or may not permanently sequester the captured CO2 and are not intended to support a commercial return during their operation.)

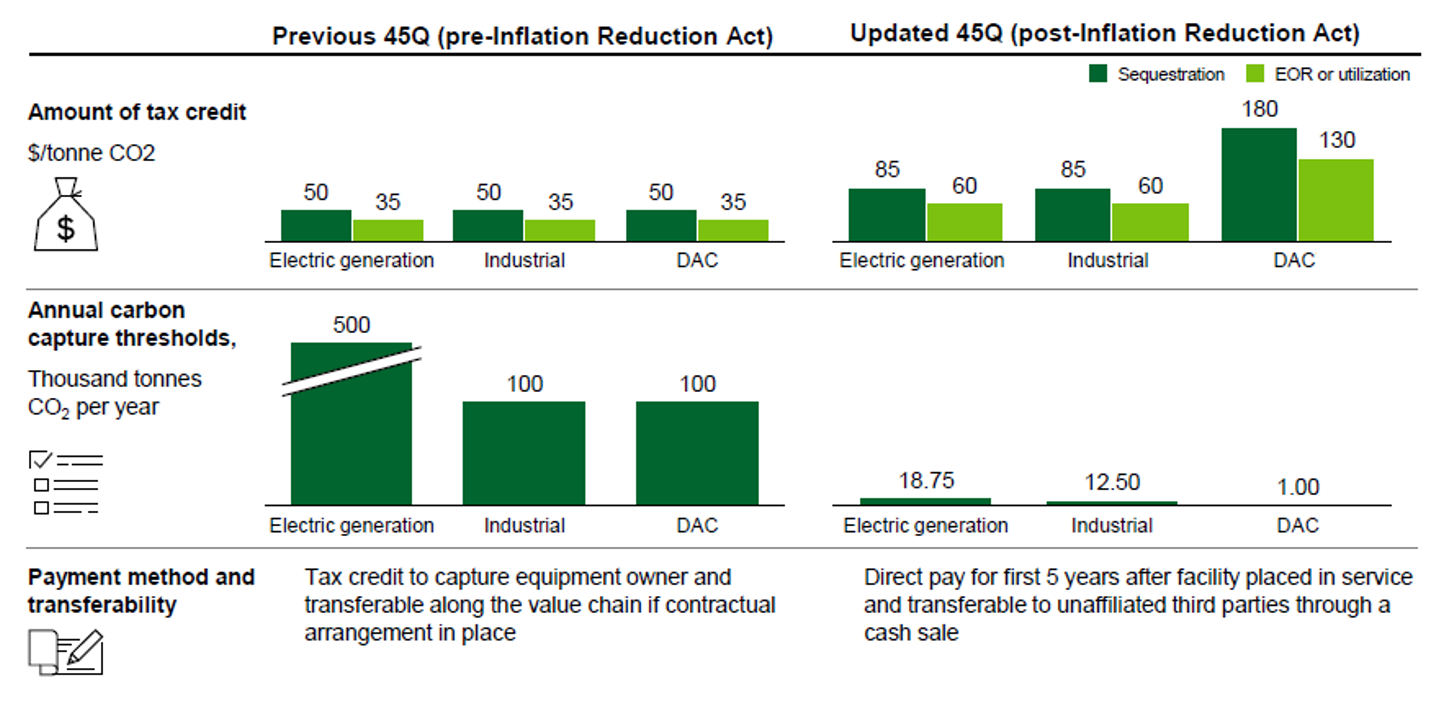

So, if there are new incentives in place and the global environment for carbon capture has never been better, why isn’t the industry taking off at a faster pace? As we discussed in our Way Down in the Hole series, the highly variable costs of carbon capture remain an issue with multiple impacts on the wider industry. Generally speaking, facilities emitting CO2 can be lumped into two buckets: high-purity and low-purity. For the most part, high-purity sources include processes with a highly concentrated CO2 stream, generally where CO2 is a byproduct and is much easier (and cheaper) to separate and capture, such as with ethanol production or natural gas processing. Low-purity sources are generally from a process where the CO2 is a product of combustion and commingled with other emissions, making it harder (and more expensive) to capture, such as a coal-fired power plant. Figure 1 below shows the level of tax credits for carbon capture and sequestration (CCS, dark green bars) and carbon capture use and sequestration (CCUS, light green bars), both before the IRA (left side of graphic) and after (right side of graphic).

Key Changes to 45Q Tax Credit Under the Inflation Reduction Act

Figure 1. Key Changes to 45Q Tax Credit Under the Inflation Reduction Act. Source: Department of Energy

About the song

“We’ve Only Just Begun” was written by Roger Nichols (music) and Paul Williams (lyrics). It appears as the first song on side one of The Carpenters' second studio album, Close to You. The song was originally written for a television commercial for Crocker Bank in California. Richard Carpenter had liked the song in the commercial and asked Paul Williams if a full-length version existed. Williams told a white lie and said “sure,” and got busy that day writing the rest of the song to present to Carpenter. Released as the third single from Close to You in August 1970, the song went to #2 on the Billboard Hot 100 Singles chart and has been certified Gold by the Recording Industry Association of America. The song was inducted into the Grammy Hall of Fame for “recordings of lasting quality or historical significance” in 1998. Personnel on the record were: Karen Carpenter (lead, backing vocals), Richard Carpenter (piano, backing vocals, orchestration), Joe Osborn (bass), Hal Blaine (drums), Doug Strawn (clarinet), and Jim Horn, Bob Messenger (woodwinds),

Close to You was recorded during the spring of 1970 at A&M Studios in Hollywood, with Jack Daugherty producing. The album was released in August 1970 and went to #2 on the Billboard 200 Albums chart. It has been certified 2x Platinum by the RIAA. Three singles were released from the LP.

The Carpenters were an American vocal and instrumental duo consisting of siblings Karen and Richard Carpenter. The pair from Downey, CA, became top-selling artists in the soft rock, easy listening and adult contemporary markets. The duo started playing professionally in 1965 before being signed by Herb Alpert to his A&M Records label in 1969. They released 14 studio albums, two live albums, 16 compilation albums, three soundtrack albums, and 49 singles. They have sold over 100 million records worldwide. Karen Carpenter died in February 1983 at the age of 32, putting an end to one of the most successful pop duos in music history. Richard Carpenter continues to write and record. He has released three solo studio albums and four singles. He is an avid Mopar automobile fan and collector. He owns several letter-series Mopars from the fifties and sixties, and still owns the 1970 Plymouth Barracuda with a 440 six-pack engine that he bought new.

Comments

Have you looked at NetPower Process? (Electricity generation in CO2 rich process stream with NG and O2 injected). Partnered and partialy owned by OXY

In reply to CO2 rich electricity generation $NPWR by Dayne Kells

Yes. We're planning to cover them in an upcoming blog.

Hi Team,

will there be anything on California CCS ?

thank you,

Jason, thanks for your analysis. Here's an example of wasteful subsidy-seeking in Saskatchewan, Canada. This project is the only grid-scale carbon capture and storage project in the world. In 2014, SaskPower started with a small 139 MW(electric) coal-fired power plant named Boundary Dam 3 (BD3). They upgraded it to 160 MW. Then, they fitted it with a problem-plagued carbon capture system that reduced the small plant's output to 110 MW. The cost to capture a metric ton (Tonne) of CO2 is about $300 Canadian. A significant fraction of the carbon dioxide still goes up the smokestack. The captured carbon dioxide is piped to an oil field for enhanced oil recovery. There, about half of the carbon dioxide leaks to the atmosphere, doubling the capture cost per Tonne. This boondoggle cost at least $1.5 billion Canadian, per http://sequestration.mit.edu/tools/projects/boundary_dam.html There have been significant operations and maintenance costs since September 30, 2016, boosting the carbon capture cost per Tonne.

Performance statistics are available at https://www.saskpower.com/about-us/our-company/blog/2023/bd3-status-update-q1-2023 Promoters of coal-fired generation fondly speak of the *potential* of carbon capture and storage (CCS.) Berkshire Hathaway Energy, a major operator of coal-fired power plants in the western U.S. appears to be reluctant to deploy CCS unless the firm receives government subsidies. Despite poor BD3 performance and poor economics, millions are being allocated for CCS in California. Emission-free nuclear power is far more cost-effective.

I think carbon capture is ultimately silly - all we need to do is to stop emitting CO2 and Global Greening will re-sequester the "extra" for free.

So the real question is - why is there no press coverage in any of the MAJOR media about the only energy source in our techonological bench which offers the promise to be as clean and reliable as nuclear but (with some experience) at costs comparable to natural gas? Eavor (dotcom) finished their final experiments 8 months ago, have received over 3 billion Euros plus about $200 million in committed funding for 24+ plants, and their first plant is well (pun intended) underway.

Mainstream Media: <crickets>

Anyone have any thoughts?