By Al Troner, President Asia Pacific Energy Consulting (APEC)

Historically U.S. condensate production has been in the backwater of crude markets, dumped into local crude flows or more recently exported to Canada for use as heavy crude diluent. In stark contrast, the separation and processing of condensates in East of Suez markets is a major downstream activity, accounting for much of the Mideast Gulf’s naphtha exports and Asia’s feedstock supply. As U.S. condensate production increases, it is clear that new markets will be needed for the volumes – with suppliers eyeing those robust East of Suez destinations. Today we continue our blog series on international condensates examining splitter/processing capacity in the Middle East and Asia Pacific regions.

|

Yesterday in our blog titled “To the Pipelines, Robin” we examined Genscape data that showed lower volumes moving via out of the Bakken and higher volumes moving via pipe. One of the terminals in the data table was Inergy’s Colt terminal, which showed a decline this month versus last. We got an email from our good friends at Inergy saying that in fact April volumes at Colt were in excess of the reported volumes and more importantly their May actual volumes increased 12% versus April. Genscape uses remote cameras to record the goings and comings of rail cars at these terminals. It turns out that there was a camera malfunction for a week, so the table should have reflected that fact. We apologize for the error. |

To really understand just how different the international condensate markets are from how these hydrocarbons are handled in the U.S. we need to go much deeper into the sources of production, processing and handling of international condensates in by far the largest market for the products – East of Suez (by East of Suez we mean the Mideast Gulf and Asia Pacific regions). In this blog we’ll focus on processing, which in these markets includes distillation, usually in a specially-built distillation tower, called a condensate splitter, and transformation – taking the condensate, through a number of process technologies, into a ready-to-use feedstock, either for olefins (ethylene cracking), aromatic petrochemicals, or as a basic input for making gasoline blending components.

Condensate Processing East of Suez

Before we get to condensate processing, it is first worth mentioning that not all East of Suez condensate gets processed. Just like in the U.S., some condensate is used directly as base stock for gasoline blending. The material is also used as boiler feed for gas combined-cycle turbines and as field fuel in remote exploration sites. Further, there are some condensate grades that are so light, clean (containing so little heavier components) and high in paraffins that they can be used directly in ethylene cracker furnaces. But the latter grouping represents a handful of grades and is often sold, from the Mideast Gulf, classified by producers as “paraffinic naphtha” rather than condensate. We talked about this ‘misbranding’ in Part 1. And just like in the U.S., some condensates are blended with or even spiked into other crudes, as dictated by operational needs.

There is an interesting twist on refinery and petrochemical condensate use, when two facilities are nearby and operated in concert with each other. In this case, East of Suez markets sometimes share a condensate feed using a petrochemical pre-treatment unit. Basically the pre-treatment unit splits the components needed for the refinery from the components needed for the petrochemical plant. More technically, while there are many types of petrochemical pretreatment units, most aim to separate naphtha from the rest of the kerosene and heavier outturn in condensate. The kerosene and heavier cut goes to the refinery. These units usually do not fully separate the naphtha cut into segregated and distinct products as a refinery distillation tower does. Instead they split the inlet volume into a heavy, mainly N+A stream [1] and a light, mainly paraffinic naphtha stream. The heavy N+A stream goes to a reformer for use in aromatic petrochemicals or for gasoline and gasoline components. The light paraffinic stream goes to an olefins petrochemical plant, for ethylene cracking.

Of course, a pre-treatment unit is not an absolute necessity for running condensates through refineries. Any conventional refinery can run condensate in its slate. However, since condensate yields such a high proportion of “light ends”, most conventional refineries lose working distillation capacity even when running relatively small volumes of condensate. That is because the light end yield from the distillation tower (crude unit) produces more volume than the refinery is designed to process. When the inlet volume is reduced to match the refinery’s light end capacity, it cuts the refinery’s overall capacity, or “bottlenecks” distillation capacity

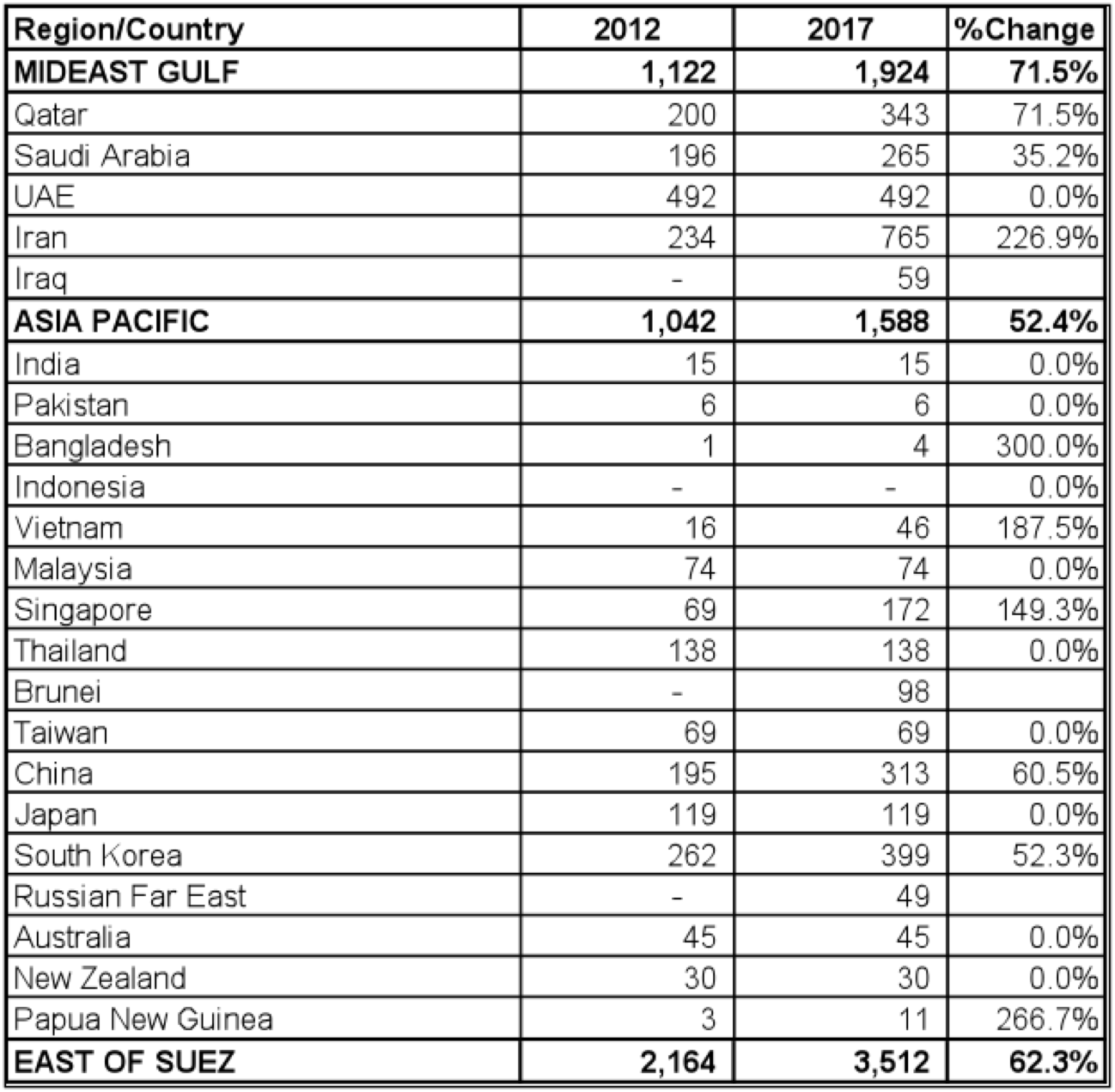

East of Suez refineries have made adjustments to handle increasing volumes of condensates. Refinery capacity in the region has risen sharply since 2000, and has been dominating overall demand for condensate. As shown in Table 1 below, in 2012, both the Mideast Gulf and Asia Pacific had 1.1 MMb/d and 1.0 MMb/d of splitter capacity operating, respectively, and that represented roughly 14% of Mideast base refining and 3% of Asia Pacific base capacity. By 2017, this should expand to 3.5 MMb/d for East of Suez, more than many countries’ total distillation capacity.

Build-Up in East of Suez Condensate Splitter Capacity (in Mb/d)

Source: ‘Condensates East of Suez 2012’, by Asia Pacific Energy Consulting

East of Suez Condensate Splitters

There are many market drivers for building condensate splitters, but overall Mideast state companies usually focus on processing to reduce the amount of segregated condensate exported, adding value by converting condensate to oil products and producing large volumes of moderate-quality gasoline for domestic consumption. Condensate is introduced into Asia Pacific refinery crude slates when refiners need a notable boost to light end output (as is the case in China and Thailand; less regularly Singapore and Japan). This might be because, when using N+A-oriented grades, a refiner needs to produce significant volumes of incremental gasoline (often the practice in South Korea and less so, Taiwan). It also might be the case that a refiner uses condensate to add a light, but more importantly, a low-sulfur grade to balance their slate. In either case the refiner either has to have underutilized capacity or a unit designed specifically to process condensate.

All splitters possess relatively simple configurations compared to conventional refineries. Some work hand-in-hand with conventional refineries (common in UAE/Abu Dhabi, Taiwan, China, Japan); others are standalone facilities (common in UAE/Dubai, Singapore, Indonesia, Australia). A few typical characteristics of these splitters include:

- Can process ultra-light crudes and moderate volumes of light crude, without plant modification;

- Have limited ability to remove sulfur from products;

- Focus on naphtha and sometimes, gasoline production; to a lesser extent also concentrate on producing better-quality grades of gas oil, in particular high-quality diesel and jet/kerosene;

- Often rely on blending to meet market quality standards, particularly for gasoline;

- Sometimes are captive suppliers of petrochemical feedstocks (Singapore, Thailand etc.).