Finding profitable markets for the rapidly increasing volumes of condensates produced in the Eagle Ford and other U.S. shale plays will be challenging. Sure there will be a growing Canadian need for condensates as a diluent for oil sands-derived bitumen, but that will still leave U.S condensate producers with a big surplus. The logical thing would be to look further afield, but selling to overseas markets— particularly to the growing Asia/Pacific region—is a complicated matter. First, an export license for “raw” (unprocessed) condensate to overseas markets is required, but no such licenses are being issued. Second, the Asia/Pacific region is also experiencing supply growth.

Today we conclude “Through the Looking Glass,” our three-part analysis of the international condensate market, by examining which countries produce and consume various condensates and why. We also look at how U.S. condensate producers, forced by their surplus supplies to jump into the topsy-turvy rabbit hole of that international market, can try to make sense of it all.

In Part 1 of our series, we discussed the complex and sometimes convoluted international condensate market. We contrasted the U.S. convention that differentiates “plant condensate” (produced at natural gas processing plants) from chemically similar “wellhead, field or lease condensate” (precipitating naturally from gas); overseas markets treat both condensate types much the same. In Part 2 we examined the condensate splitters in major countries of the Middle East and Asia/Pacific regions, where most of the condensate market action occurs. Today we examine in some depth production and demand trends “East of Suez,” and consider potential niches for surplus U.S. condensates in markets overseas.

The production side of the international condensate market East of Suez can logically be split into two groups: the Middle East, which dominates condensate supplies, and the Asia/Pacific region, which produces some segregated condensate but also regularly imports a large volume of Mideast supply. Some major Asian condensate consumers rely entirely on imports, mainly from the Mideast, notably South Korea, Japan, Singapore and at times, Taiwan. Yet a number of the importing countries produce sizable volumes of condensate and consume most of it in the domestic market, such as Indonesia, Malaysia, Thailand and China, but none, however, is bigger than China.

Mideast Gulf Producers

Four countries provide almost all of Middle Eastern condensate supply: Qatar, Saudi Arabia, UAE/Abu Dhabi and Iran. Here’s a drill-down on the situation and strategy unique to each:

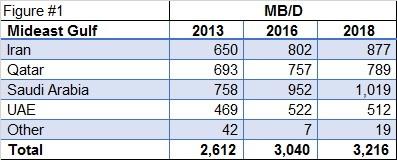

*Qatar: Almost all of Qatar’s condensate supply comes from its North Field, the world’s largest known gas field. Three grades of condensate are produced by Qatar Petroleum (QP): (a) NGL naphtha, a plant condensate that is sold solely as an oil product - paraffinic naphtha - and is used as olefin (petrochemical) feedstock. The remaining two other grades – (b) Low Sulfur Condensate (LSC) and (c) Deodorized Condensate (DFC) - are blends of field condensate together with plant output. Qatar is second only to Saudi Arabia as the largest condensate producer in the Mideast Gulf and is the world’s largest volume condensate exporter. Qatar’s 2012 condensate production was greater than its black oil output and is expected to increase from 693 Mb/d in 2013 to 789 Mb/d in 2018 (See Figure #1). However, that buildup in Qatar’s output will slow with completion of current gas projects, and export volumes likely will fall once a second large splitter starts up. While the Emirate’s base petrochemical capacity will continue to expand, the primary feedstocks will be ethane and LPG (propane and butane), with condensate serving only as feedstock “trim”. Qatar is an exporter of petrochemicals, LPG, gasoline, naphtha and kerosene, as well as large volumes of condensate. Most exports move to Asia/Pacific buyers, mainly in northeastern Asia; in the future Qatar will focus further on China.

Mideast Condensate Production (Click to Enlarge)

*Saudi Arabia: The Kingdom this year edges out Qatar and Iran in condensate output, but is planning expansions that by 2018 will increase that advantage by boosting its output to 1,019 Mb/d, from 758 Mb/d this year. Unlike Qatar, Saudi Arabia’s condensate comes mainly from oil field-associated gas, though this will change as non-associated fields start up. The Kingdom works to minimize condensate exports, to preserve the large sales premium that light, highly paraffinic A-180 (see Part 1 for background on A-180) receives, when sold as top-quality naphtha. Saudi Arabia’s other condensate grade, known as Khuff, is used in conventional refineries, or split, mainly to produce gasoline. A-180 is used as trim feedstock for Saudi olefins, but as in Qatar ethane and LPG make up base load supply. As the world’s largest crude exporter, substantial volumes of condensate are simply spiked into crude oil. Together with Qatar, the Kingdom accounted for most Mideast Gulf base petrochemical exports. Saudi condensate is usually sold to East Asian buyers.

*UAE/Abu Dhabi: The UAE is a relatively small volume exporter in proportion to its raw condensate production, as it splits most condensate and then exports the resulting naphtha, gasoline and middle distillate, focusing on jet/kerosene. In 2013, UAE’s condensate output is expected to total 469 Mb/d, and it’s expected to rise by only 10%, to 512 Mb/d, over the next five years. While condensate output and splitting is dominated by Abu Dhabi, merchant splitters also operate in Dubai and Fujairah. Abu Dhabi has pushed a policy of minimizing condensate exports to add value to its output, but the program has had mixed success. Within the UAE, only Abu Dhabi produces base petrochemicals, using mainly LPG as feedstock, supplemented by ethane. Domestic UAE demand absorbs much of the gasoline, diesel and jet produced by condensate splitters, while naphtha is usually exported.

*Iran: Tightening international sanctions, the withdrawal of foreign investment and growing domestic unrest have slowed the buildup of Iranian condensate output, though in 2012 it remained at over 500 Mb/d and by 2018 it’s expected to top 800 Mb/d. Most of the output is absorbed in domestic refining or condensate splitting, or is being fed directly into petrochemical plants, though National Iranian Oil Company (NIOC)—if it wants -can push out large condensate volumes, as it did in late 2012. Iranian condensate demand is for both gasoline and petrochemical feedstock. An ambitious building program for new splitters has fallen far behind schedule, while many gas projects remain pending.

As indicated in Figure #1, total Mideast condensate production is expected to rise from about 2.6 Mb/d to 3.4 Mb/d in the 2013-18 period, an increase of 23%, with more than two-fifths of the gain coming from Saudi Arabia. Because the leading Mideast Gulf producers use much of their condensate internally, exports from the region this year will total about 0.9 MMb/d out of the total 3.6 MMb/d of production. More than half of that export volume, or about 0.5 MMb/d, will come from Qatar; Saudi Arabia will export 0.3 MMb/d and UAE 0.1 MMb/d.

Join Backstage Pass to Read Full Article