Cold weather, abundant supplies of natural gas and lower-than-normal winter gas prices spurred record power burns in January and February, and the power burn for the rest of 2015 is likely to be record-breaking too. It almost has to be; all the gas expected to be produced this year needs to go somewhere, and there’s only so much that can be stored. That suggests continued softness in natural gas prices—hardly good news for gas producers. Today, we examine the outlook for this year’s power burn, and the variety of factors that point to record-breaking gas consumption by the U.S. power sector.

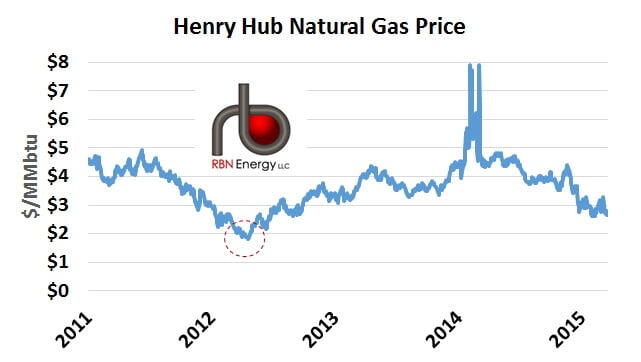

For natural gas, the 2012 power burn season was one for the record books. As we said a while back in 2012 Natural Gas Power Burn—Was That a Wild and Crazy Year?, abnormally high gas consumption by the power sector that year [peaking at a record-shattering 1.08 trillion cubic feet (Tcf), or almost 35 Bcf/d, in July 2012] was driven primarily by very low spring and summer gas prices--the result of fast-rising gas production and much-higher-than-normal storage levels at the end of the “non” winter of 2011-12 (2.4 Tcf, vs. the five-year average of less than 1.9 Tcf). With a return to higher gas prices, the gas power burn sagged in 2013 (peaking at 29.2 Bcf/d, again in July) and 2014 (peaking at 28.9 Bcf/d in August). Now, gas prices (and futures) are down to their lowest level since September 2012, gas storage levels are 500 Bcf higher than they were this time last year, and 2015 gas production is expected to remain strong (likely topping 73 Bcf/d, on average), despite recently announced cutbacks in drilling. Before we consider the factors suggesting a record-breaking power burn this year, let’s look at the 2012 power burn phenomenon in a little more detail because it helps inform us about this year’s potential. As seen in Figure #1 showing cash market Henry Hub gas prices from NGI, mild weather and abundant supplies in the winter of 2011-12 precipitated a big post-winter drop in gas prices (to about $2/MMBTU in April 2012 – red dashed circle). Gas prices that low (and they stayed below $3/MMBTU through that summer and early fall) get utilities and independent power producers (IPPs) thinking about taking some coal-fired units offline temporarily and replacing their output with energy from gas-fired combined-cycle units.

Figure #1; Source: Intelligence Press - NGI

In Switching on a Dime—How Power Burn is Driven by Plant Fuel Costs, we discussed how coal-to-gas switching is not simply a matter of which fuel is cheaper at the moment on a per-BTU basis. Other, “operational” factors come into play, including total system demand (if it’s very high, or if a nuclear unit is down, you may need to run all your coal and gas units), unit location (will taking Coal Unit A offline and firing up Gas Unit B cause transmission congestion?), and gas pipeline capacity. Still, fuel cost is the principal determinant in economic dispatch, the process utilities, IPPs and electric grid operators use to determine which units run--and which don’t--on any given day (or any given hour, for that matter). With natural gas prices unusually low in the second and third quarter of 2012, gas consumption by the power sector each month (according to EIA) was sharply higher than the same month in 2011—up 37% in April, 42% in May, 26% in June, 15% in July, 9% in August, and 17% in September—and 2011 was no slouch in the power burn department. All that incremental gas consumption moved the gas market back into balance; without the increased power burn, too much gas would have been stored.

About the song

"These Boots Are Made for Walkin'" was a Number 1 hit for Nancy Sinatra in 1966, and was later covered by singers ranging from Loretta Lynn to Jessica Simpson. The song was written by Lee Hazlewood, the son of an Oklahoma oil man.

Comments

Thanks for the excellent and timely article. I look forward to reading more about this.

Regarding demand, a big (2 BCF/d) project has been completed on the U.S. side to export natty to Mexico. The last I heard was that the "demand" on the Mexican side, i.e., power generation, wasn't ready and wasn't going to be ready until 2016. You all have done a number of articles on the increased demand in Mexico for U.S. gas, but I don't remember seeing anything about this. Can you provide any updates? 2 BCF/d is a chunk of demand that could materially alter the picture.