Kinder Morgan is conducting an open season to convert an El Paso Natural Gas pipeline to crude oil service from the Permian Basin in West Texas to California refineries. The ”Freedom Pipeline” project would cost as much as $2 Billion. Before going ahead they need to convince crude producers in the Permian and/or refiners in California to make long term commitments to the pipeline. Today we begin a two part assessment of the chances that this pipeline will get built.

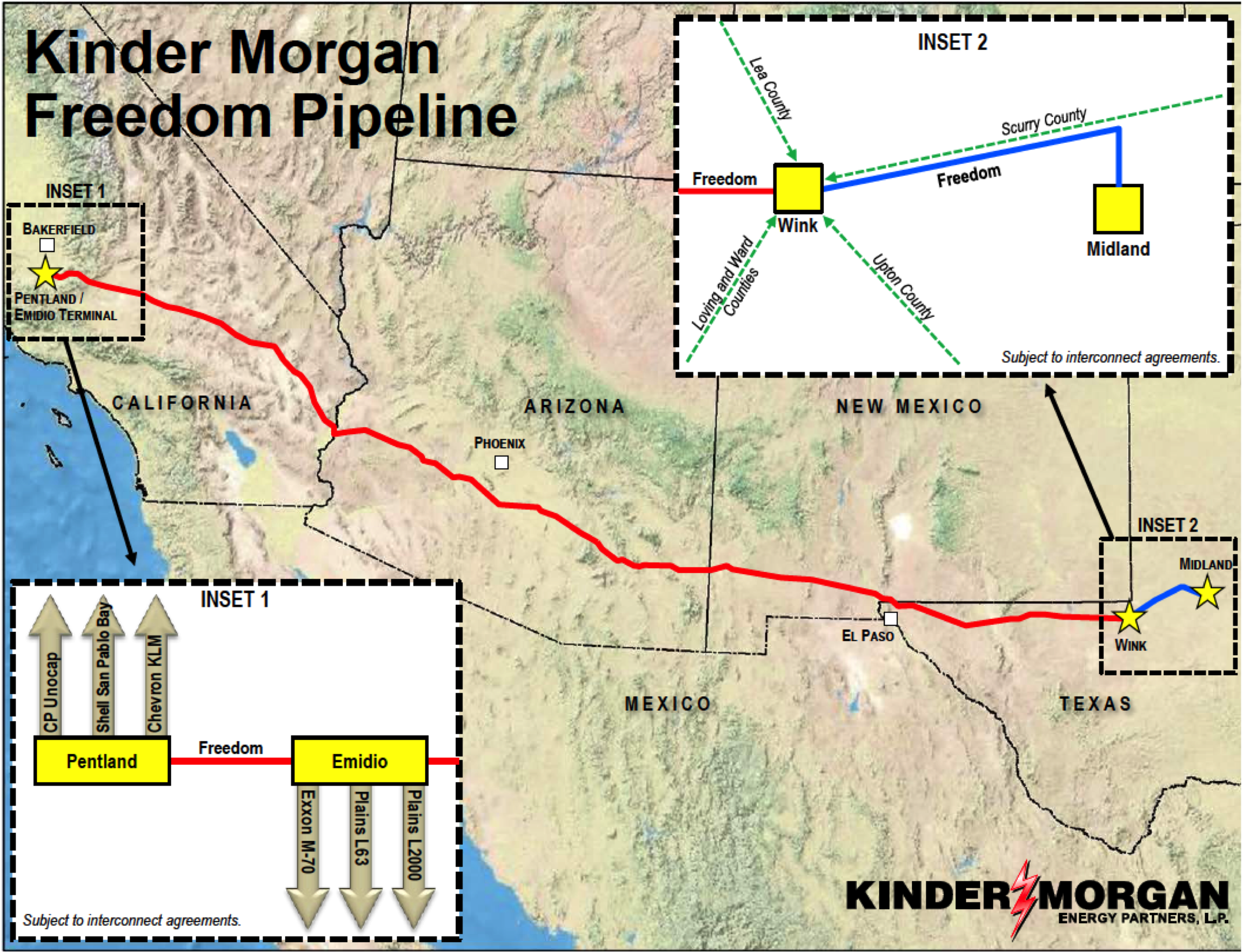

In March 2013 Kinder Morgan Energy Partners (KM) issued notice of an Open Season to gauge shipper interest in a crude pipeline from the Permian Basin in West Texas to refineries in San Francisco and Los Angeles (see map below). The project is called the Freedom Pipeline. Initial crude capacity will be 277 Mb/d and if approved the pipeline will go into service early in 2016. The Freedom pipeline will largely consist of converting 740 miles of an existing natural gas pipeline belonging to KM subsidiary El Paso Natural Gas (EPNG). That EPNG pipeline is a large westbound system with about 5.6 Bcf/d capacity that transports natural gas from the San Juan, Permian and Anadarko basins to California, other Western states, Texas and northern Mexico. KM will only be converting part of the EPNG pipeline and the rest will still provide gas service.

Source: Kinder Morgan Open Season Notice

Converting the FERC

The possibility to convert part of the EPNG pipeline comes about now as a result of reduced use of the gas capacity between West Texas and Southern California. That is because demand for gas in the Southern California consuming region has been falling - reflected in low basis spreads from the Permian Basin. Over the past two years the El Paso, TX to Socal Gas, CA pricing basis has traded on average at less than $0.25/MMBtu. As a pipeline operator KM is looking to increase revenue by converting a part of the pipeline to crude oil service. To make the conversion, KM will need to get Federal Energy Regulatory Commission (FERC) approval to abandon gas service on that part of the pipeline. That process may not be a rubber stamp. There have been concerns expressed that converting as much as 0.5 Bcf/d of gas capacity to a crude pipeline will create a constraint on gas supplies to California. That constraint would increase consumer prices if demand picks up in the future. The expected 1 bcf/d increase in natural gas export capacity to Mexico from Texas and California (see Oh Rio Rio – Gas Across the Rio Grande) being built by the end of 2014 already creates a potential strain on regional gas supplies.

Conversion Cost and Line Fill

Assuming that they can convince the FERC to allow abandonment of the gas service, KM estimate that the cost of converting the EPNG gas pipeline to crude including adding new pipeline to connect at both ends and new pump stations will be $2 Billion. That’s a heck of a lot of money. We recently posted a blog that ran through the economics of gas to crude pipeline conversions (see One Way or Another). Another major cost in that conversion process - especially for longer pipelines - is the cost of filling the converted pipeline with crude oil. How much would that cost? We used earlier RBN Energy calculations (see A Time for Gas A Time For Crude Part 1 and Part 2) to estimate line fill costs for the Freedom pipeline. The published estimated initial crude flow is 277 Mb/d suggesting that the pipeline will be approximately 24-inch diameter. That equates to about 3,160 Bbl of light crude oil per mile. The length of the converted section of the pipeline is 740 miles and there will be an additional 200 mile section from Wink, TX to El Paso, TX for a total length of 940 miles. The line fill volume is therefore approximately 940 * 3160 or ~ 3 MMBbl. Using the Friday WTI Cushing price (May 3, 2013) of $95/Bbl the cost of 3 MMBbl of crude is $285MM. That cost is usually shared by committed shippers – roughly $1MM per 1Mb/d shipped. In the case of pipeline projects like Freedom, the operator KM would pay the capital investment cost (the $2 Billion) but shippers would be expected to pay the line fill. Clearly that barrier to entry caused a few jitters among potential shippers. A recently updated KM open season notice adds key changes to the shipper agreement including a tariff based option for shipper or carrier supplied line fill – meaning that shippers will have an option to pay a higher tariff instead of up front line fill costs. An attractive concession but shippers will still be paying line fill one way or another.

In the rest of this posting we take a look at the Freedom project from the perspective of crude producers in the Permian. Then tomorrow we look at how attractive the pipeline is for California refiners. We start by looking at Permian takeaway capacity and alternative routes to market.

Available Capacity

We know that Permian crude production is growing rapidly. Bentek estimates 1.37 MMb/d for April 2013 and forecasts growth to 1.6 MMb/d by 2016. Existing pipeline capacity and local refinery consumption totals about 1.2 MMb/d. That means production exceeds takeaway capacity today and producers are using rail and even trucks to transport their crude to the Gulf Coast market as a result. However, by the end of 2014 another 900 Mb/d of pipeline capacity will have come online to move Permian crude to the Gulf Coast (see New Adventures of Good Ole Boy Permian). All of that pipeline capacity is either approved for construction or in the case of the Longhorn reversal (135 Mb/d) and Phase 1 of the Permian Express (90 Mb/d) already beginning to ship crude. Adding to these Permian projects a new proposal from Plains All American was announced at the end of April 2013 – the Cactus Pipeline - that would run from the Permian Basin to South Texas to link with existing pipelines to Corpus Christi or Houston. The Cactus pipeline would carry 200 Mb/d and be in service 1Q 2015.

The net result of these capacity expansions is that unless the Permian production forecast is very understated, existing and already planned pipeline capacity of 2.1 MMb/d will exceed production for at least the next 2 years. The Cactus and Freedom projects will add another 400 Mb/d to that excess capacity. To attract producers the Freedom project will therefore have to compete with existing projects for production barrels. Winning that competition is going to require an attractive economic proposition for Permian producers.

Alternative Routes to Market

The two pipeline destination alternatives for producers who might ship on KM Freedom are the Midwest and the Gulf Coast. Midwest capacity is on the legacy lines moving crude either into Cushing (Centurion and Basin pipelines) or through the Midwest to Illinois (West Texas Gulf pipeline). Gulf Coast capacity would be on the new pipelines under construction. Both alternatives have disadvantages. The Midwest market is over supplied with crude trying to get past Cushing to the Gulf Coast. That means crude prices are lower at Cushing than they are at the Gulf Coast today. So some of the crude currently travelling into Cushing on Basin or Centurion would likely be attracted to the Freedom project, especially since the Midwest is likely to have more than adequate light sweet crude supplies from the Bakken for the foreseeable future.

The Gulf Coast market is an attractive alternative to the Midwest in the short term because of the potential to sell crude at higher international related prices based on the Light Louisiana Sweet (LLS) benchmark. Last week (May 3, 2013) LLS was trading at an $11/Bbl premium to WTI. That premium more than covers the pipeline tariff of $2.50/Bbl on the new Longhorn pipeline from Crane, TX in the Permian Basin to Houston. In the longer term, however, the Gulf Coast market is likely to be over supplied with light sweet crude grades such as WTI (see After The Flood) – placing downward pressure on prices. The recent narrowing of the Brent/WTI spread has shown that differentials can evaporate quickly when market sentiment changes. Given that the Gulf Coast market does not look so attractive in the long term, producers could be tempted to look favorably at the alternative of moving their crude west on the Freedom pipeline.

Comments

This line is the original All American (Plains All American) pipeline which stretched from the onshore facility at Gaviota CA across the coastal range to Pentland then to McCamey Texas. This originally was to stretch to Houston but permits through the Edwards could not be secured. And then the price of crude oil collapsed and moving CA grade crude and ANS via the AA was scrapped. At one time Arco Pipeline was moving ANS via the Black Mesa pipeline to Bisti NM then to Jal and on to the gulf via Mobil and Shell Pipeline.

When ELP bought the line they purged it and removed the heating stations that were built to keep the crude flowing. Except for the tie in at Wink I do not believe they have tied anything in to the line across NM or AZ. And for gas hydraulics are not as big a concern as liquids. There are two points, Continental Divide and coming out of the Colorado River basin where there may be some concerns about the wall thickneess of the pipe. This may wind up resulting in either alower MAOP of the line or changing out pipe at these locations. There are a lot of options today for doing this.

The other concern is the grade of crude and the crude slate for the refinerys in CA. The new crude coming on is super sweet and light. There will have to be modifications for the CA refinerys to run this type of crude. Will the refiners be willing to expend the CapX for the changes to be able to run this crude? They may be able to blend the heavy CA grade crude to get a decent slate, but if they are having to pay a premium for the crude then would it be worth it. I dont see the whole pictures but I do not see enough excess refining capacity in California to be able to take an additional 277K bbls a day. From what I see CA is pretty ballanced. What comes in goes out. And I do not see CA increasing a need of more refined produce. It is a state on the decline, and large energy users looking to relocate would pick a whole bunch of places long before they would go to CA.