The proposed $2 Billion Kinder Morgan Freedom pipeline project is conducting an open season for shipper commitments from West Texas to California. The California refining market has long operated like an island within the US and has so far received few supplies from new domestic production. To proceed with the project Kinder need shippers to make long term commitments but today’s unsettled markets place a premium on flexibility. Today we conclude our two-part analysis of the chances that the pipeline will get built.

In yesterday’s first episode in this series covered the cost of building the pipeline, as well as the perspective of Permian producers (see Is the Price of Freedom Too High? Part 1). Today we look at how the pipeline benefits California refineries and how it shapes up against rail alternatives.

California Refineries

Kinder Morgan (KM) expects the Freedom pipeline to ultimately ship 400 Mb/d of crude from the Permian Basin to California that will be a combination of West Texas intermediate (WTI) and West Texas sour (WTS). WTI is a light sweet crude and WTS is a light sour crude. By contrast, California refineries are currently processing a predominantly heavy and medium sour crude slate as follows: (source California State Energy Almanac)

Total crude refined during 2012 = 1.6 MMb/d made up from:

Alaska North Slope (ANS): 195 Mb/d medium sour crude

California crude: 629 Mb/d of which approximately 51 percent is heavy crude (Thums, Kern River) and 49 percent is medium sour (Line 63)

Imported crude: 790 Mb/d made up of 27 Mb/d light sweet, 415 Mb/d light medium sour and 348 Mb/d of heavy crude

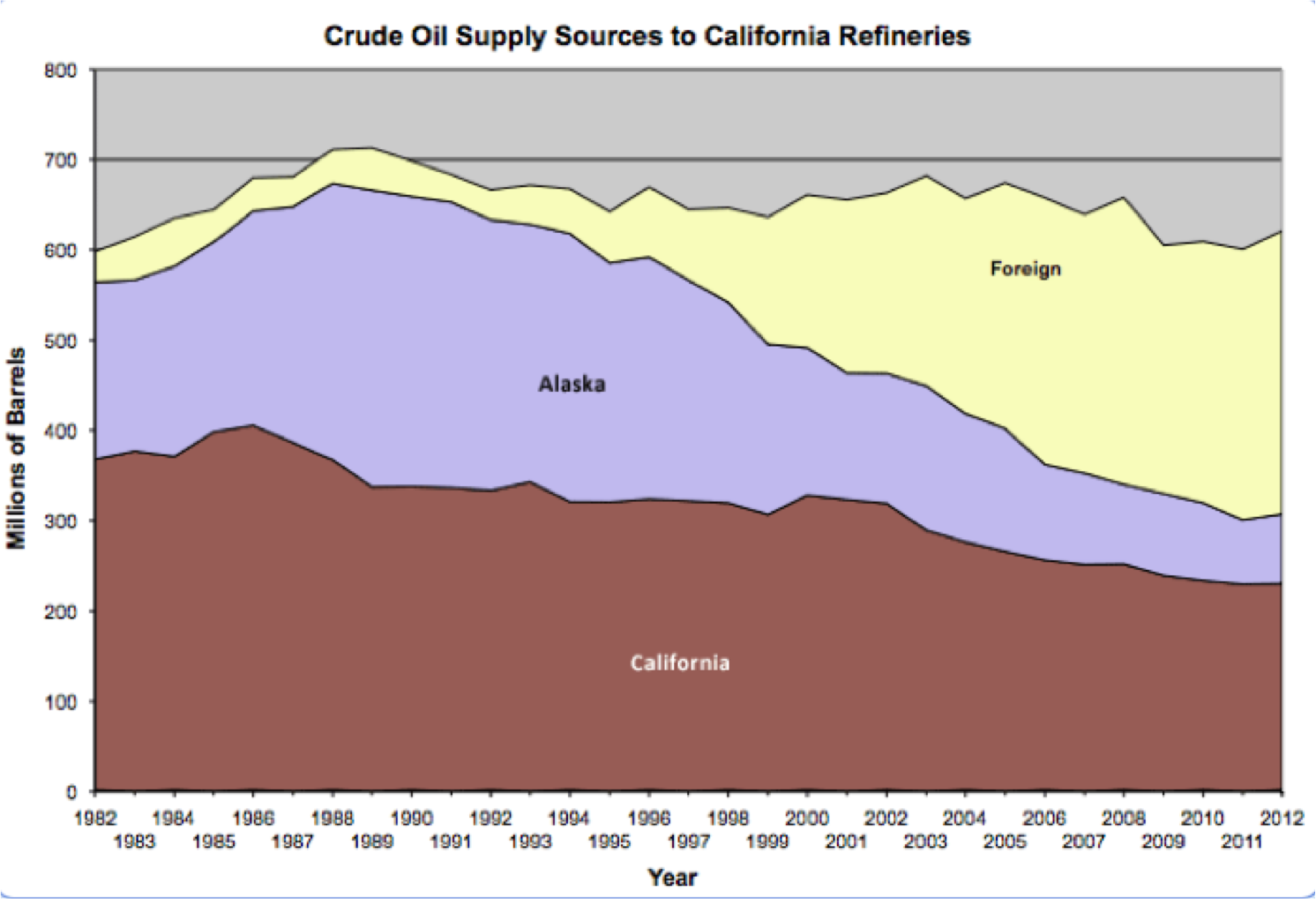

The chart below shows the historic crude diet of California refineries. Notice three trends. First California crude oil production was about 540 Mb/d in 2012 but has been declining since 1995. Production is not expected to increase unless producers successfully exploit the State’s Monterey Shale. The Monterey has potential reserves of 15 billion Bbl according to the Energy Information Administration (EIA) but there are geology challenges to extracting the oil and environmental concerns about fracing in California. The second trend on the chart is the decline in ANS production (we discussed that previously in “After the Oil Rush”). Making up for the decline in ANS and California production is the third trend of increasing foreign imports. Permian crude supplies shipped by pipeline from Texas would most likely take the place of California’s imported crudes.

Source: California State Energy Almanac

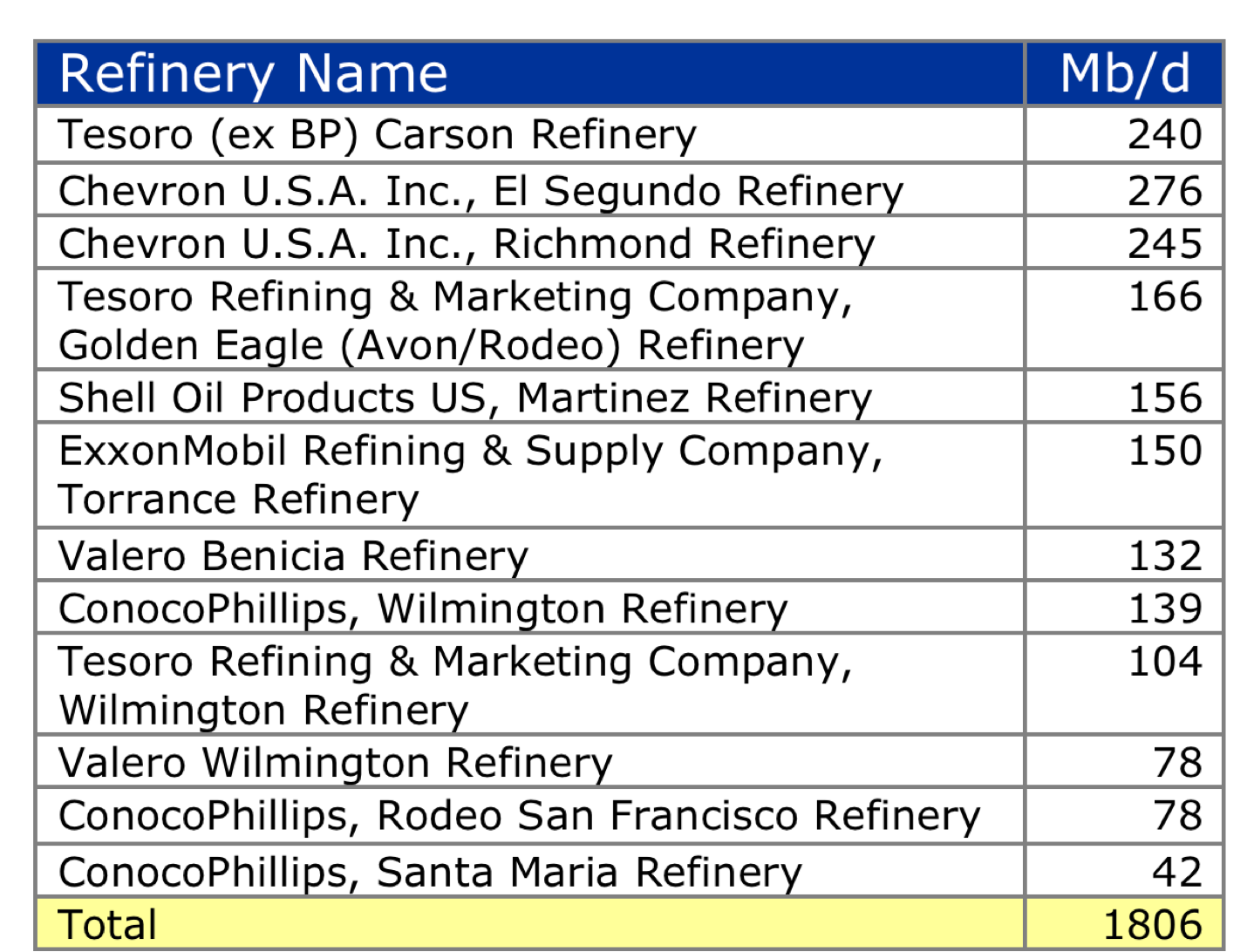

One obvious question is whether WTI and WTS are a good fit with California refineries that currently process a diet of heavy or medium sour crude? Typically refineries configured for heavy crude are not optimized to handle lighter grades (see Turner Mason and the Goblet of Light and Heavy for more on this topic). The table below lists the refineries that the Freedom pipeline will connect to with a total capacity of 1.8 MMb/d. That is enough capacity whereby refiners could immediately process significant volumes of light Permian crudes by blending them with heavier crude. WTS crude would probably be a good fit to replace light medium sour crudes. Between them these refineries could probably consume 200 Mb/d or more of Permian crudes and replace imported barrels. Over time refiners would probably need to invest in new processing equipment to handle lighter a bigger diet of lighter crudes. The reality is that given US crude production trends all refiners are incentivized to make that transition over the next several years.

Source: California State Energy Almanac

A potential benefit to California refiners from using crude produced in West Texas is the lower carbon footprint of US domestic shale crude compared to imports – especially from the oil sands in Western Canada. Carbon footprint is important to refiners in California because of recent California Air Resource Board (CARB) regulations. These regulations, under the Low Carbon Fuel Standard (LCFS) program require every crude that California refiners process to be graded by carbon footprint based on how they are produced and transported. The grading includes estimates of carbon emissions made during crude extraction. Newer Permian Basin production from tight oil shale will likely have a lower carbon footprint than crudes produced using more energy intense methods like Canadian oil sands or ANS. Although it is still unclear how the LCFS will be enforced, it will have an important influence on the crudes that California refineries choose to process. In the longer term this could mean that refining lighter crudes that require less complex refining will help refiners comply.

Competition from Rail

We covered crude by rail delivery to the West Coast recently in our Crude Loves Rock’n’Rail series (see West Coast Destinations). We noted then that crude by rail has been slow to penetrate into California. That is partly because state regulations have delayed the building of rail unloading terminals because the permitting process is complex. A lot of crude is being railed to refineries in Washington State from the Bakken or to marine terminals in Washington and Oregon. Some of that crude will reach California refineries by barge or tanker. Some refiners – notably Alon and recently Valero have announced plans to build rail terminals at California refineries – so far with the intent to rail light crude from the Bakken or heavy crude from Canada. Crude is also being sent by rail from the Permian Basin – where a number of rail loading terminals have been built including a KM/Watco terminal at Pecos, TX (see Load Terminal Craze Sweeps the Nation).

Recent company presentations estimate crude by rail costs from the Bakken to central California at $13/Bbl and to Southern California at $14/Bbl. We did not find a published rail rate from West Texas to California but have heard estimates in the $8 -$10/Bbl range plus terminal and lease charges. If this is the case then shipping Permian crude to California by rail will be less expensive than Bakken or Canadian alternatives. Although KM have not published their pipeline tariff yet it will almost certainly undercut rail freight door to door. So if California refiners decide that they need to start using inland US domestic or Canadian crudes then they might as well lock in the least expensive delivery option.