The U.S. can make a lot more ethane than it can consume. Producers are drilling for ‘wet’ shale gas, high in natural gas liquid (NGL) content – with ethane making up more than half of that NGL volume. Unfortunately there is not enough U.S. petrochemical cracking capacity to use all that ethane. And for a whole variety of reasons the product has been notoriously difficult to export. Consequently, over 250Mb/d of ethane is being rejected – sold as natural gas instead of being processed into liquid ethane. What if there were a ready market for all this surplus ethane supply, just waiting to open its doors? Well, there just may be. The emerging U.S. LNG export market may be able to absorb a big portion of the supply imbalance, and make LNG buyers happy at the same time. In this blog series we will explore that possibility and consider the implications for the ethane market in North America.

The Ethane Problem

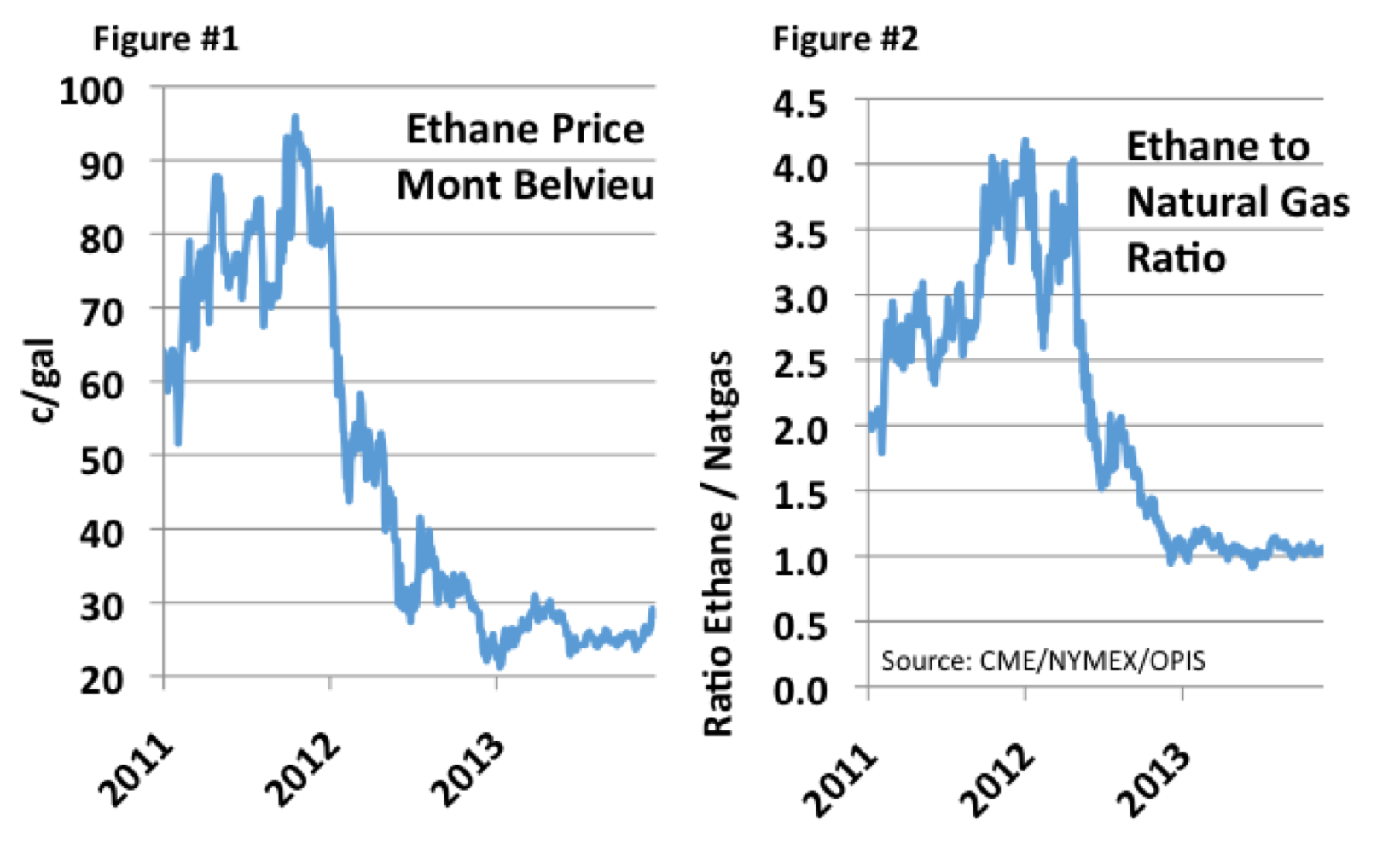

Ethane prices have kicked up just a bit in the past week or so, but generally speaking (as shown in Figure #1) ethane is still dirt cheap. Figure #2 puts the numbers in perspective. It shows the ratio of Mont Belvieu ethane converted to a BTU equivalent price and compared to Henry Hub natural gas. The graph indicates that the price of ethane continues to languish at prices just above the equivalent price of gas (a ratio of about 1.0), where it has been for most of this year. It is worse than it sounds, because to get to Mont Belvieu, ethane must be processed, transported by pipeline and fractionated, all of which cost money. So back at the gas processing plant, the “netback” value of ethane is well below the value of natural gas across much of the U.S. Why pay money to extract, transport and fractionate ethane when it is worth more selling it is gas?

The result is ethane rejection. We’ve discussed this phenomenon many times in the RBN blogosphere, including No Particular Place to Go, The Ethane Asylum and Dirty Deeds Done Dirt Cheap. With so much “wet” or high BTU content shale gas flowing to them, natural gas processors can simply make much more ethane than petrochemical companies can use. The result has been high inventories, low prices and rejection.

Source: CME data from Morningstar and OPIS

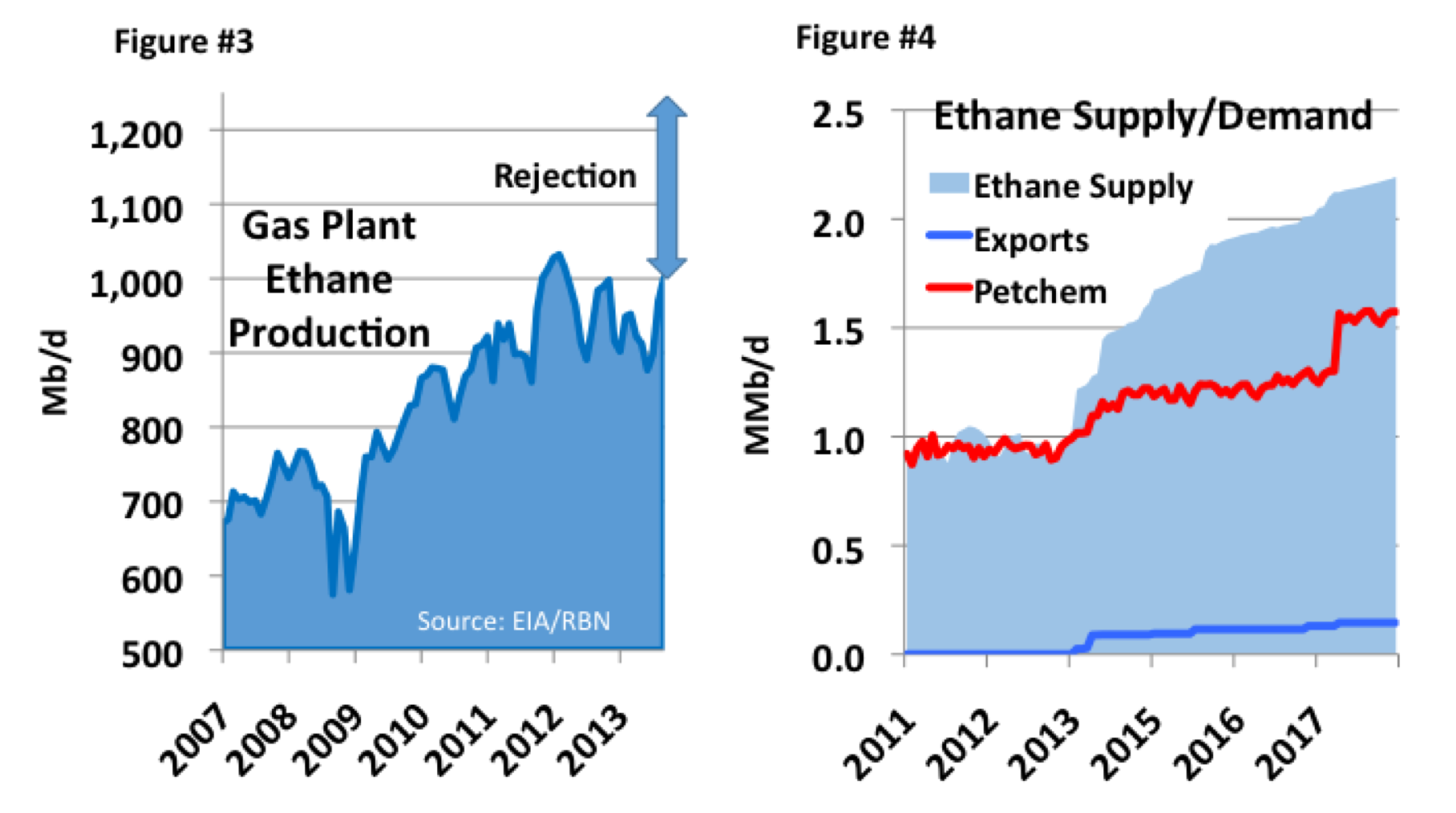

We estimate that there is about 250 Mb/d of ethane rejection happening right now. It is a difficult number to assess, because it is an estimate about something that is NOT happening. The ethane is not being recovered. However, it is possible to make an educated guess based on the growth in other NGL production volumes that ethane has not been enjoying (See Figure #3). If all the ethane in the ‘wet gas’ stream was being recovered, fractionated and moved to market, ethane production would be more than 1.2 MMb/d. As it is, ethane production reported by EIA is only about 1.0 MMb/d.

Figure #4 shows one scenario of how bad this problem may become. Given the RBN outlook for significant NGL production growth, we see the possibility that - within five years there could be more than twice as much ethane available for extraction than there is today. Most of this potential new supply would be coming from the 'usual suspects' - Eagle Ford, Bakken and especially Marcellus/Utica. That is way more ethane than is slated to be used. The blue line on Figure#4 shows the ethane that could be exported to Canada (via the Vantage pipeline from North Dakota) and to overseas markets from the Marcellus (via the ETP/Sunoco Mariner East pipeline and Marcus Hook, PA dock). Stacked on top of the export line is one scenario for upcoming petrochemical demand increases, with a big bump happening in 2017-18 when new olefin crackers from Exxon, CP Chem, Oxy/Mexichem, Formosa and Sasol are expected to come on line. Note that even with these new plants, this scenario anticipates that another 500 Mb/d of ethane will remain in rejection mode. That is a lot of ethane being sold as natural gas.

Source: EIA and RBN Energy

Why Not Just Export the Surplus?

With all this surplus ethane, why not just export it to overseas markets? After all exports are the solution for surplus propane and butane in the NGL world. And surplus natural gas supplies will be exported in the form of liquefied natural gas (LNG) once liquefaction plants are built later this decade. Even surplus light crude oil will effectively be exported in the form of refined motor gasoline. (We will talk more about all of these exports in our end-of-year blog, coming soon.)

About the song

The Kid is Hot Tonight – was a hit in 1981 for Canadian rock band Loverboy

Comments

Nice teaser!

I guess the value for Ethane is feedstock for LNG since the low Ethane/HH NG ratio.

Simon