Despite dreams of a white Christmas and a “soft landing” for the U.S. economy, there’s a lot going on in the world — much of it upsetting and even gut-wrenching. As for energy, crude oil prices have been sagging after a brief rise and natural gas prices, while up from their lows, remain less than stellar — and it seems things could get far worse in the blink of an eye. All of that has combined to make folks cautious and wary, and that’s impacting how oil and gas producers spend — or hoard — their money. In today’s RBN blog, we analyze U.S. E&Ps’ increasingly conservative cash allocation despite rising returns in Q3 2023.

NATGAS Billboard is a daily, early morning email and report that provides an up-to-the-minute view of the natural gas market outlook, including storage injections/withdrawals and price. Billboard’s models incorporate pipeline flow data, weather models, electricity demand data and more.

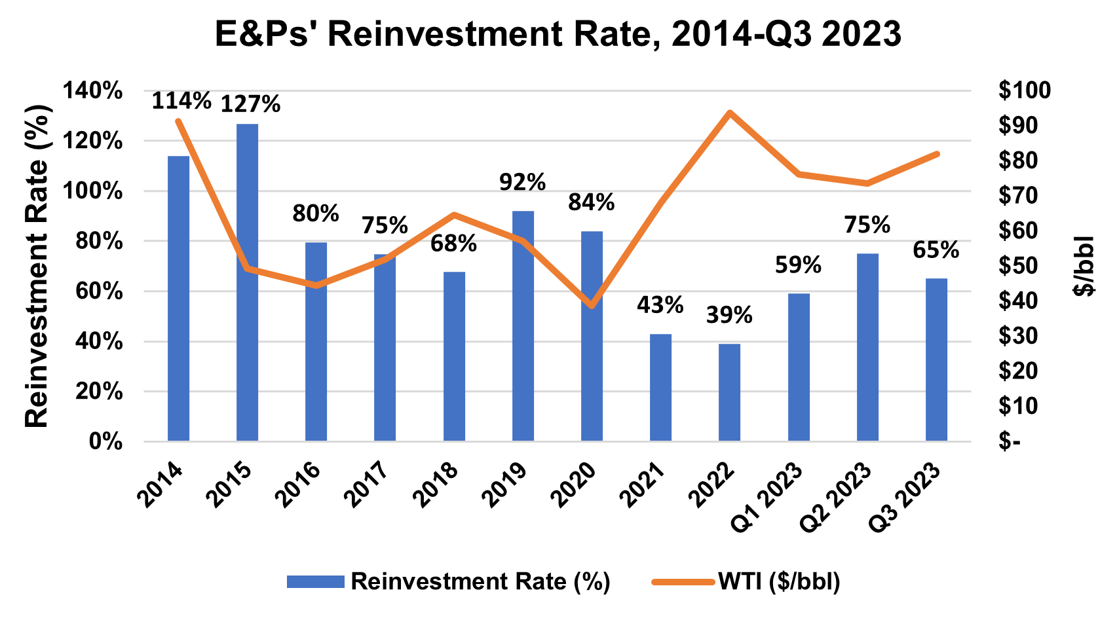

In After the Gold Rush, we documented a 15-month decline through Q2 2023 in the operating income and pre-tax operating cash flows of the 41 oil and gas producers we covered in that analysis. Rising capital expenditures sopped up 76% of cash flows in Q2 2023, nearly double the reinvestment rate of a year earlier, which left just $6.6 billion in discretionary funds for allocation. It’s no surprise that remittances to shareholders fell 34% from the previous quarter to a level less than half the peak in Q2 2022. Share repurchases — the most discretionary of expenditures — plunged to $3.8 billion from $7 billion in the previous quarter and a high of $10.9 billion in Q4 2022. Dividends, both fixed and variable, fell to $5 billion from $6.4 billion in the previous quarter and a high of $8.7 billion in Q3 2022. That still left a $2 billion shortfall, which producers met by increasing debt.

Fortunately, as we recently discussed in Baby Come Back, E&Ps saw a 13% increase in average realized prices in Q3 2023 — including a healthy $82/bbl for WTI (right end of orange line and right axis in Figure 1). The resultant rebound in earnings and cash flow for our universe of producers exceeded expectations, with pre-tax income rising 42% and cash flow from operating activities (CFOA) increasing 17% to $30.1 billion. As we predicted in that blog, management also put the brakes on capital expenditures after a 44% increase since Q1 2022, holding outlays flat with the preceding quarter at $19.4 billion. That decreased the reinvestment rate to 65% (blue bar to far right and left axis) and increased free cash flow (FCF) to $10.7 billion, $4.1 billion, or 62%, higher than Q2 2023.

Figure 1. E&Ps’ Reinvestment Rate, 2014-Q3 2023. Source: Oil & Gas Financial Analytics, LLC

About the song

“Take It Easy” was written by Jackson Browne and Glenn Frey. It appears as the first song on side one of the Eagles’ debut album, Eagles. Released as the first single from the album in May 1972, it went to #12 on the Billboard Hot 100 Singles chart. The song was written by Browne and Frey when they lived in the same apartment building at 1020 Laguna Avenue in the Echo Park community of Los Angeles. Browne would later record the song for his second studio album, For Everyman. There is a “Take It Easy” Glenn Frey statue in Corner Park in Winslow, AZ, in tribute to the song. Personnel on the record were: Glenn Frey (lead vocal, acoustic guitar), Bernie Leadon (lead guitar, banjo, backing vocal), Randy Meisner (bass, backing vocal), and Don Henley (drums, backing vocal).

The album, Eagles, was recorded in February 1972 at Olympic Studios in London and Wally Heider Recording in Los Angeles with Glyn John producing. Released in June 1972, it went to #22 on the Billboard 200 Albums chart and has been certified platinum by the Recording Industry Association of America. Three Top 40 singles were released from the LP.

The Eagles are an American rock band formed in Los Angeles in 1971. They have released 10 studio albums, three live albums, 10 compilation albums, and 30 singles. They have had five #1 singles and six #1 albums, and have sold more than 200 million records worldwide. The Eagles have won five American Music Awards and six Grammy Awards, and were inducted into the Rock and Roll Hall of Fame in 1998, the Vocal Group Hall of Fame in 2001. They received Kennedy Center Honors in 2016. Nine members have passed through the group since its formation. Founding member Glenn Frey died in 2016; Randy Meisner died in 2023. The group continues to record and tour and will finish their The Long Goodbye Final Tour in March 2024.