What a difference a year makes! The summer of 2022 was a golden age for U.S. E&Ps that embraced a dramatic shift in their business model from prioritizing growth to a focus on maximizing cash flows and emphasizing shareholder returns. Oil prices over $90/bbl and gas prices hovering about $7/MMBtu filled their coffers and funded lavish increases in share repurchases and dividends. But those golden days quickly faded as oil prices retreated and gas prices plunged 66% to just above $2/MMBtu. In today’s RBN blog, we explain how E&Ps are scrambling to sustain shareholder return programs in the face of shrinking cash flow.

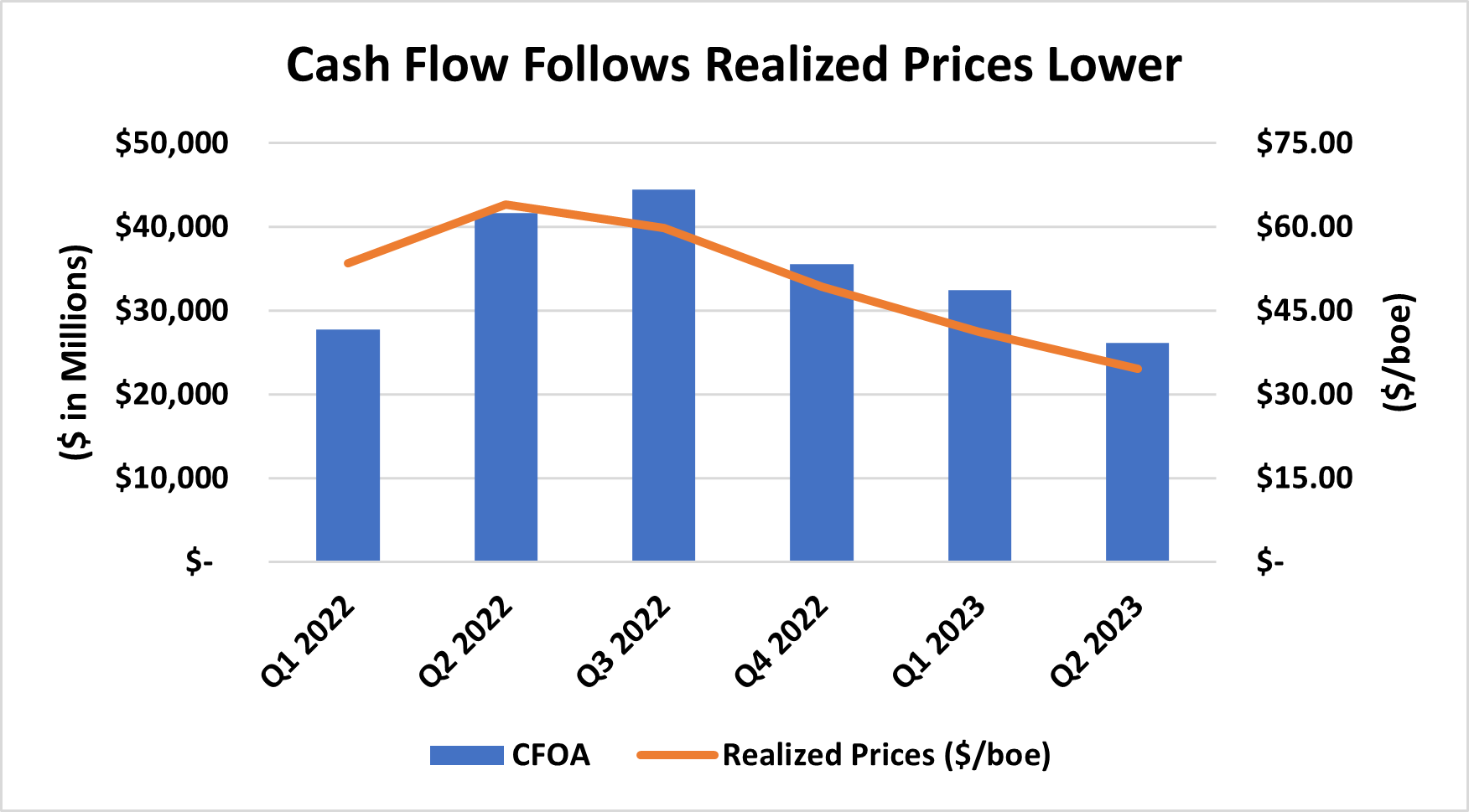

In our blog Two Shots of Happy we recapped a near-idyllic Q2 2022 as cash flows for the 41 U.S. E&P companies we follow surged 22% from the preceding quarter to $43.4 billion on average prices of $108/bbl for oil and $7.47/MMBtu for gas. Cash flow from operating activities (CFOA) topped out at $46.5 billion in Q3 2022 as share repurchases more than doubled to $9.7 billion from $4 billion in Q1 2022 and dividends rose 62% to $8.7 billion. But as shown in Figure 1, the average realized price (orange line) peaked in Q2 2022 and fell to $34.57 per barrel of oil equivalent (boe) by Q2 2023, 46% lower than a year earlier. Cash flows (blue bars) followed suit, reaching a two-year low of $26.2 billion.

Figure 1. Cash Flow and Realized Prices, Q1 2022-Q2 2023. Source: Oil & Gas Financial Analytics, LLC

Compounding the lower commodity prices is the impact of inflation on the cost of oilfield goods and services. Producers largely held the line on capital investment in 2022, budgeting maintenance-level spending that increased modestly from $14.4 billion in Q2 2022 to $15.8 billion in Q4 2022. However, higher costs and the need to replace inventories of drilled but uncompleted wells (DUCs) have driven capex to $18.5 billion in Q1 2023 and $20 billion in Q2 2023.

About the song

“After the Gold Rush” was written by Neil Young and appears as the second song on side one of Neil Young’s third studio album of the same name. When asked about the meaning of the song’s lyrics, Young has said: “It’s an environmental song … this thread that goes through a lot of my songs has a time-travel thing.” The English group Prelude released an a capella version of the song in 1974 that was an international Top 40 hit. Dolly Parton, Emmylou Harris, and Linda Ronstadt covered the song on their 1999 LP, Trio II. Personnel on the record were: Neil Young (vocals), Nils Lofgren (piano), and Bill Peterson (flugelhorn).

The album After the Gold Rush was recorded between August 1969-June 1970 at Sunset Sound in Hollywood, Sound City in Van Nuys, and Redwood Studios (Neil Young’s basement studio in his home in Topanga Canyon) in Topanga California. Produced by Neil Young and David Briggs, the album was released in September 1970. It went to #8 on the Billboard 200 Albums chart and has been certified 2x Platinum by the Recording Industry Association of America. Two singles were released from the LP. The songs on the album were inspired by the unproduced Dean Stockwell and Herb Bermann screenplay “After the Gold Rush.” The album cover features a photo of Neil Young walking past the New York University School of Law in the West Village in New York City taken by Joel Bernstein. The whole frame of the original photo included Graham Nash walking with Young. The LP was inducted into the Grammy Hall of Fame in 2014.

Neil Young is a Canadian American singer, songwriter and musician. After starting his professional career in the mid-sixties in Winnipeg, Young moved to Los Angeles in 1966 and helped form the group Buffalo Springfield. He has enjoyed five decades as a solo artist in addition to being a member of Crosby, Stills, Nash & Young. As a solo artist he has released 45 studio albums, 12 live albums, four soundtrack albums, three compilation albums, two EPs, and 62 singles. He released three studio albums and nine singles with Buffalo Springfield, and eight studio albums, five live albums, six compilation albums, and 19 singles with Crosby, Stills, Nash & Young. He has won three Grammy Awards and is a member of the Canadian Music Hall of Fame. He has been inducted into the Rock and Roll Hall of Fame twice, in 1995 for his solo work, and in 1997 as a member of Buffalo Springfield. He continues to record and tour.