It may be easy to forget in these days of Permian this and Permian that, but crude oil production in the offshore Gulf of Mexico (GOM) set a number of new, all-time records in the past couple of years. Better yet, with a handful of key producers in the Gulf planning low-cost, subsea tiebacks to existing platforms — and still discovering more oil — it’s a good bet that offshore production will continue its upward trajectory into the early 2020s. And, unlike U.S. shale wells, whose production peaks early then trails off, wells in the GOM typically maintain high levels of production for years and years. Where do offshore production and drilling activity stand in the Shale Era, and where are they headed? Today, we review recent production gains in the Gulf and examine why the GOM remains the oil sector’s Energizer Bunny.

Crude oil production in the Gulf of Mexico is a topic that generally flies below the radar, unless there’s a major hurricane that causes a big, downward spike in output or a man-made disaster like the Macondo/Deepwater Horizon blowout in April 2010, which effectively halted drilling in the Gulf for more than a year. In The Crude Genie? in early 2016, we noted that crude production in the federal GOM dropped by ~500 Mb/d (to ~1.1 MMb/d) between March 2010 (the month before the blowout) and September 2011, and it took almost four years (until August 2015) for Gulf production to return to pre-Macondo levels. (All data is from our friends at Drillinginfo.) And it took another year and a half — until February 2017 — for GOM output to top the all-time record of 1.75 MMb/d hit in September 2009 (see Don’t You Forget About Me).

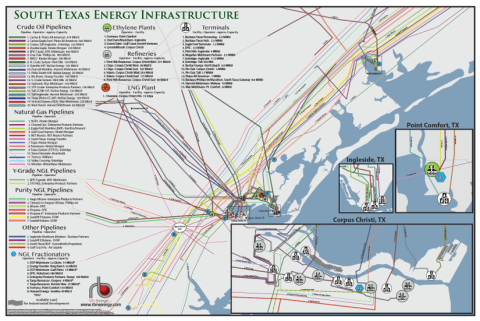

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

Given the time it takes to develop new crude-oil infrastructure in the deepwater and ultra-deepwater Gulf, the ~650-Mb/d production rebound in the 2011-17 period was largely the result of investment decisions that exploration and production companies (E&Ps) made in the first half of the 2010s, a period during which crude was often selling for $90 or $100 (or more) per barrel. Like their E&P counterparts on terra firma, though, producers in the GOM have learned to survive and ultimately thrive in an era of relative supply abundance and lower crude prices. For shale players, that has meant focusing on production sweet spots, improving drilling efficiency, boring longer laterals and using more frac sand, among other things. GOM producers, in turn, have shifted their focus almost entirely to low-cost subsea tiebacks that allow production at new deepwater wells without the need to install topside (above-water) production platforms. Instead, the new wells are tied back to existing topside platforms using subsea flowlines. As we’ve said in earlier blogs, we understand that, depending on how much oil the new well can access (and other factors), the breakeven cost for many subsea tieback projects already has fallen enough to put them on par with breakevens in some of the best onshore shale plays. And, as we’ll get to in a moment, the cost of greenfield projects in the Gulf that involve new topside production platforms has been coming down sharply too, indicating that there may still be a lot of life in the old GOM yet.

About the song

“Against All Odds (Take a Look at Me Now)” was written and recorded by Phil Collins as the title song for the 1984 movie Against All Odds. Produced by Arif Mardin and released in February 1984, the single went to #1 on the Billboard Hot 100 Singles chart, #1 on the Mainstream Rock Tracks chart, and #2 on the Adult Contemporary list. Originally an unreleased song of Collins’s titled “How Can You Just Sit There,” written about the breakup between Collins and his first wife, the song was rewritten to reflect what the film was portraying. In addition to the single, the song appears on the 1984 soundtrack album, Against All Odds, and also on Collins’s 1998 Hits album and Love Songs: A Compilation, released in 2004. Personnel on the recording were: Phil Collins (vocals, drums), Rob Mounsey (piano, keyboards), and an orchestra conducted by Arif Mardin. The song won a Grammy Award for Best Pop Vocal Performance by a Male in 1985.

Phil Collins is an English singer, songwriter, drummer, multi-instrumentalist, record producer and actor. He started in show business as a child actor, and his professional musical career began as the drummer, and later lead vocalist for the British rock band Genesis. He recorded nine studio and two live albums with Genesis. Since going solo in 1979, he has released eight studio albums, one live album, and three compilation LPs, along with 45 singles. He has sold more than 150 million records worldwide. Collins has won eight Grammy Awards, six Ivor Novello Awards, four Billboard Music Awards, three American Music Awards, two Golden Globes, one MTV Video Music Award, and one Academy Award. He is a member of the Songwriters Hall of Fame, was inducted into the Rock and Roll Hall of Fame as a member of Genesis, and has a star on the Hollywood Walk of Fame. In March 2022, at the last date of Genesis’s The Last Domino? Tour, at O2 Arena in London, Collins announced that “It’s the last show for Genesis.” A five-LP Box set was released in September entitled Both Sides (All the Sides).