Another round of big changes are coming to the markets for natural gas, natural gas liquids (NGLs) and crude oil. The surging production growth that has characterized these markets has slowed and in some basins is starting to fall as the mass exodus of drilling rigs begins to take its toll on shale production. But what about all that infrastructure that has been and continues to be built? Billions of dollars are going into pipelines, processing plants, petrochemical plants, terminals, storage, etc. based on a much higher production growth scenario than now seems likely. Where are the opportunities in this new energy market reality? The answer depends on a discernable pattern of events tied to production volumes, infrastructure capacity, commodity flows and project expenditures. Those are the themes of our latest State of the Energy Markets Conference scheduled for October 28, 2015 in Denver, CO as well as the subject of today’s blog – also an advertorial for the conference.

Before we get into the details of today’s blog, we need to let you know that the next RBN Fundamentals Webcast is scheduled for this coming Wednesday, September 23rd at 2:30pm central time. In this session available to Backstage Pass subscribers, Rusty Braziel will review RBN’s latest production forecasts, consider the consequences for pipeline projects and introduce a new RBN online database for monitoring infrastructure developments. This is the prequel not only for the State of Energy Markets in Denver, but also for some of the most important topics to be covered at RBN’s renowned School of Energy to be held a week from today in Houston, TX.

Production Declines Are Finally Starting to Show Up

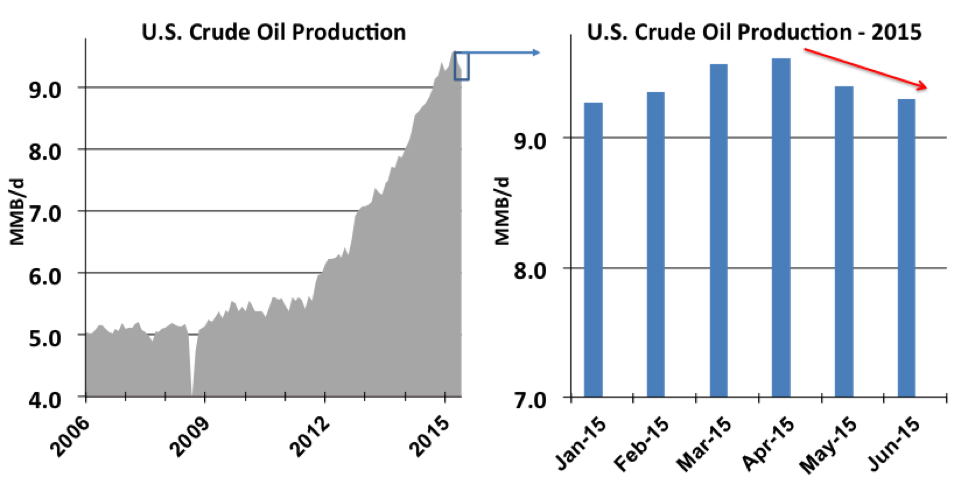

It had to happen eventually. There is only so much magic dust that U.S. producers can sprinkle on shale basins to counteract the impact of sustained low prices. After falling steadily from $100/Bbl plus last June to just over $40/Bbl in January 2015 and recovering to $60/Bbl between March and June of this year, U.S. benchmark West Texas Intermediate (WTI) crude prices have languished in the mid $40’s/Bbl this month (September 2015) and there seems to be nothing on the horizon that would make you think that even a return to the $60s is in the offing anytime soon. Low prices have prompted a dramatic pullback in drilling rig deployment and despite remarkable resilience in crude production, we have certainly witnessed a convincing end to the 1 MMb/d year growth experienced between 2012 and 2014 shown in the left graph in Figure #1.

Monthly Energy Information Administration (EIA) crude production data shows declines in May and June (red arrow on the right hand chart in Figure #1). It is reasonable to assume that downward trend will be with us for a while. Even the robust math of wells being completed out of inventory (wells drilled months ago, only now being brought online) and very high “sweet spot” initial production rates that have been mostly responsible for sustaining production until now can’t offset the natural declines in shale wells forever, at least not at today’s rig count.

Figure #1 – U.S. Crude Oil Production; Source: EIA

It’s a similar story for NGLs. Total NGLs from gas processing plateaued since January at 3.2 MMb/d this year, with May and June production below the peak month of April 2015. Lower-48 natural gas production has also been flat, with declines in most of the country supported only by strong production growth this year from Marcellus/Utica.

That slowdown has been a bit of a surprise for some midstream infrastructure developers. Take what has happened to developers of new pipeline capacity to the Gulf Coast over the past couple of years. As we covered in Stairway to Houston, new pipelines into Houston are – on average – running about half full today based on daily average flow rates from our friends at Genscape. As shown in Figure #2, when you stack up the seven major pipeline systems that move crude to the broader Gulf Coast market (Seaway, Seaway Twin, Enterprise Eagle Ford, Kinder Morgan Eagle Ford, Bridgetex, Longhorn and TransCanada MarketLink, capacity utilization looks a bit better recently, but still collectively those pipes are only about two-thirds utilized. Which begs the question, how many more pipes are really needed?

About the song

“Rocky Mountain Way” was written by Joe Walsh, Joe Vitale, Rocke Grace and Kenny Passarelli. It appears as the first song on side one of Joe Walsh’s second studio album, The Smoker You Drink, The Player You Get. Released as a single in June 1973, the song went to #23 on the Billboard Hot 100 Singles chart. Walsh said the lyrics came to him as he was mowing the lawn at his Colorado home. “I looked up and there’s the Front Range of the Rocky Mountains and it knocked me back because it was just so beautiful.” The song features Walsh using one of the original talk boxes designed and manufactured by Bob Heil. Walsh gave songwriting credits to all four members of his band Barnstorm, since they helped transform what began as a blues jam in the studio to a fully realized song. The Colorado Rockies Major League Baseball team plays “Rocky Mountain Way” after every home win at Coors Field. The Denver Broncos National Football League team plays Godsmack’s version of the song at home games at Empower Field at Mile High Stadium. Personnel on the Joe Walsh record were: Joe Walsh (lead vocal, guitar, keyboards), Kenny Passarelli (bass, backing vocals), Joe Vitale (drums, percussion, backing vocals), Rocke Grace (keyboards, backing vocals), and Joe Lala (percussion).

The Smoker You Drink, The Player You Get was recorded between late 1972 and early 1973 at Caribou Ranch in Nederland, CO, and the Record Plant in Los Angeles. Produced by Joe Walsh and Bill Szymczyk, it was released in June 1973. The album went to #6 on the Billboard 200 Albums chart and has been certified Gold by the Recording Industry Association of America. The cover art for the album features a British Sopwith Snipe fighter plane with French colors that appears to be flying upside down as the blue sky is at the bottom and the brown ground is at the top of the illustration. One single was released from the LP.

Joe Walsh is an American guitarist, singer, songwriter and record producer. He started his professional career as the lead singer and guitarist of the James Gang, a rock and roll trio formed in Cleveland, OH, in 1966. He left the band in 1972 to pursue a solo career. In 1975, Walsh joined The Eagles. He released four studio albums with the James Gang and has released five albums with The Eagles so far. As a solo artist, he has released 20 studio albums, one live album, six compilation albums, and eight singles. He has appeared on more than 40 albums by other artists. Walsh continues to record and tour, with six upcoming shows with the James Gang booked in November.