Permian crude production increased by 26 percent between January 2012 and May 2013 according to Bentek. Production is now about 1.4 MMb/d - virtually the same as existing pipeline takeaway capacity and local crude consumption. That tight balance has caused considerable price volatility between Midland, TX in the production region and Cushing, OK in the past year. Today we begin an updated analysis of Permian production and takeaway capacity.

We posted our first blog on West Texas Permian Basin crude production back in September 2012 (see The New Adventures of Good Ole Boy Permian). Oil production in this historic and prolific basin is now close to 1.4 MMb/d (June 2013 – Bentek estimate) – an increase of about 100 Mb/d since that original post. The Permian Basin has been producing since 1920 and today’s high production levels are still down from its 1973 peak of 2.1 MMb/d. A lot of recent Permian production still uses conventional drilling and enhanced oil recovery techniques, but horizontal drilling is now making its mark as well. As Permian output has rebounded in recent years pipeline takeaway capacity has come under increasing strain and midstream players have been building new pipelines and rail terminals. Most of the new infrastructure flows crude to the Gulf Coast where it will join 1 MMb/d from the Eagle Ford and as much as 2MMb/d from Canada and the Bakken in an ever growing flood of crude looking for refineries. So it is definitely time to revisit the Permian and update our analysis of crude production, takeaway capacity and the refining market. This first episode in our new series covers the production forecast, local refining capacity and existing takeaway pipelines.

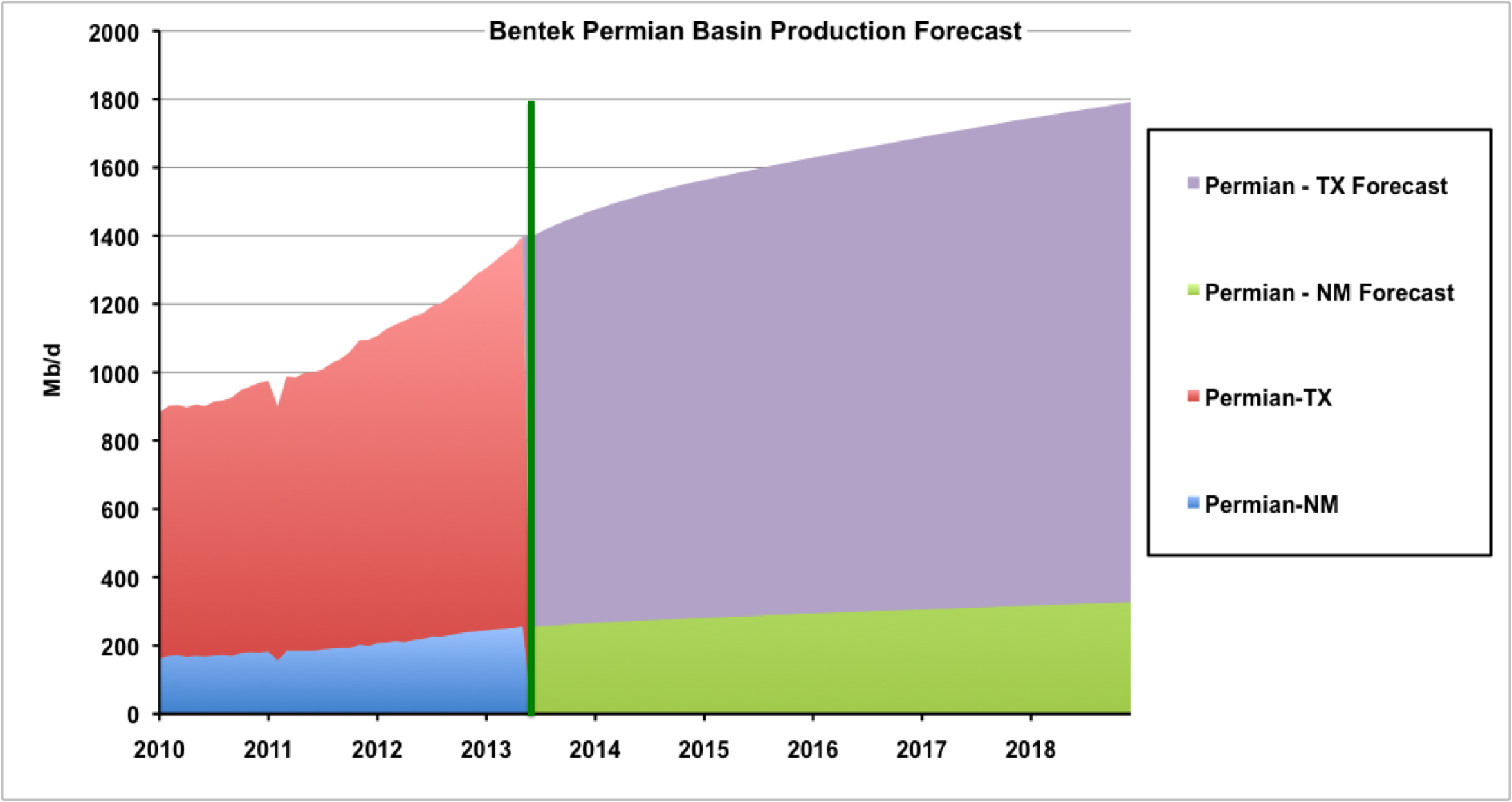

The chart below shows crude production for the Permian basin in Texas and New Mexico. Historic production is to the left of the green line - expanding from 880 Mb/d in January 2010 to 1.4 MMb/d in June 2013. The forecast is to the right of the green line and shows an expected increase to 1.8 MMb/d by December 2018. That is an expansion by 28 percent between now and the end of 2018. The majority of production comes from the Texas part of the basin versus the smaller New Mexico output. But production in both States is forecast to grow equally rapidly.

Source: Bentek

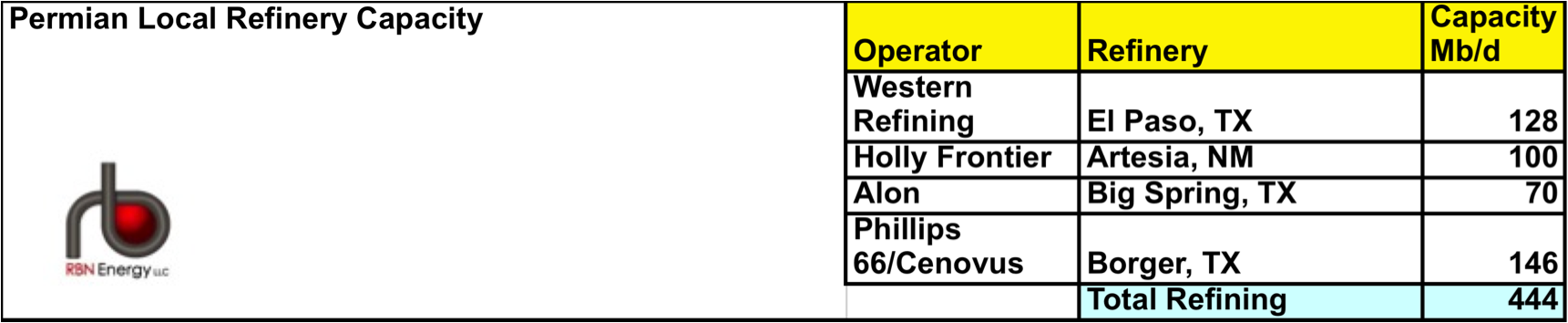

There are four local refineries in West Texas and New Mexico that consume a diet of Permian crude. Recall from our earlier posts that crude from the Permian comes in two flavors. Those flavors would be West Texas Intermediate (WTI) that has a typical API gravity of 38-40 degrees with a sulfur content of 0.3 percent – making it a light sweet crude and West Texas Sour (WTS) that has an API gravity of 32.8 degrees and a sulfur content of 1.98 percent – making it a light sour crude. Production volumes are split approximately 70 percent WTI and 30 percent WTS. The table below lists the four refineries that between them soak up close to 450 Mb/d of Permian crude production. The Western Refining El Paso refinery is fed by the Kinder Morgan Wink pipeline and has 128 Mb/d capacity. Holly Frontier process 100 Mb/d at their Navajo refinery in New Mexico and the Alon refinery in Big Spring has 70 Mb/d capacity. Two pipelines from the Permian Basin feed the Phillips 66/Cenovus 50/50 Borger refinery – the 118 Mb/d WA Line and the 30 Mb/d Line 80. The high volume of crude processed locally in the Permian poses a challenge for outbound crude takeaway capacity when one of these refineries goes offline unexpectedly – pushing its crude supply back onto the crowded takeaway pipelines out of the region. For example, last November the Borger refinery extended a maintenance turnaround unexpectedly and the resulting additional crude supplies were in part to blame for WTI and WTS prices at Midland, TX (in the production region) being discounted by $20/Bbl versus crude delivered to Cushing, OK. The deep discounting reflected lack of capacity on the pipelines from Midland to Cushing, which only charge shippers a $0.69/Bbl tariff – if you have pipeline reservations.

Source: RBN Energy

Existing pipeline capacity out of the Permian basin is slowly expanding as new infrastructure comes on line (see map below). This year saw the opening in April of the Magellan Longhorn pipeline from Crane to Houston and Texas City (purple line). The initial capacity on Longhorn was 75 Mb/d – expected to increase to 225 Mb/d by the end of 2013. The Sunoco Logistics/Energy Transfer Partners West Texas Gulf (WTG, red line) pipeline has also been expanded this year from 250 Mb/d to 340 Mbd. The expansion includes the addition of 40 Mb/d into Houston and 40 Mb/d into Nederland from the Sunoco Wortham, TX terminal. The remaining barrels on the WTG pipeline are directed east at Wortham to the Longview, TX intersection with the Mid Valley pipeline that runs through the Midwest. The largest conduit out of the Permian is the Plains All American Basin pipeline that carries 450 Mb/d to Cushing (green line). The last of the 4 existing takeaway pipes is the Occidental operated Centurion pipeline that flows 140 Mb/d from Midland to Cushing (blue line).

About the song

“Rock the Casbah” was the highest charting hit worldwide for The Clash - recorded in 1982

Comments

The list of refineries does not include Valero at Mckee