The U.S. is still years away from establishing a national carbon tax or cap-and-trade system — and it’s certainly possible it will never take either step. But there are state and regional cap-and-trade programs in place to incentivize refiners and others to reduce their greenhouse gas (GHG) emissions. In today’s RBN blog, our fourth and final on carbon emissions and the refining sector, we look at state and international efforts to reduce GHG emissions and their prospective impact on the U.S. refining industry.

In Part 1 of this series, we gave an overview of emissions from refineries, technical ways to mitigate them, and how those policies might ultimately influence refining competitiveness. In Part 2, we investigated the policy options deployed in Europe and how its Emissions Trading System (ETS) is affecting the European Union’s (EU) refining industry as a whole, then looked at Canada’s carbon tax in Part 3, including how it works and the future impacts on oil sands producers, bitumen upgraders and refiners.

First, a reminder: A carbon tax and a cap-and-trade system are two distinct approaches to reducing GHG emissions. A carbon tax sets a fixed price on GHG emissions that is paid by all identified participants — typically fossil-fuel suppliers, power plant operators and other emission-intensive industries. Under a cap-and-trade system, in turn, the government sets a GHG emissions cap and then issues allowances, which permit a certain amount of emissions over a specific period. Covered entities can buy, sell, or trade those allowances to meet their emissions targets. This approach is designed to help ensure that the combined efforts of all participants are as cost-effective as possible.

To date, no state has implemented a carbon tax and neither has the federal government. There are two cap-and-trade programs currently employed in the U.S. — one regional and the other a single-state effort. The first to be developed was the Regional Greenhouse Gas Initiative (RGGI), which covers the Mid-Atlantic and Northeastern states but only applies to the emissions from fossil fuel power generators. The second system is the California Air Resources Board’s (CARB) cap-and-trade program, which covers about 80% of California’s emissions, especially large power and industrial emitters, including refineries.

Since the RGGI doesn’t impact refineries, we will focus on the CARB program, which as you would expect affects only refineries in that state. After that, we’ll look at a second way that a larger share of U.S. refineries and other industrial emitters may be impacted by carbon pricing, namely carbon border adjustment mechanisms (CBAM) in other countries.

California’s Cap-and-Trade Program

California’s Assembly Bill 32 (AB 32), enacted in 2006, directed CARB to establish a plan for the state to reduce its GHG emissions to 1990 levels by 2020, beginning in 2012. The cap-and-trade program established by the law is similar to the overall structure of the EU’s ETS, although there are some differences when you dig into the details. (We should also note that the CARB program is similar to the cap-and-trade system of Quebec, which we mentioned in Part 3.) AB 32 was also responsible for creating the state’s Low Carbon Fuel Standard (LCFS) program, which we’ve discussed in numerous blogs over the years.

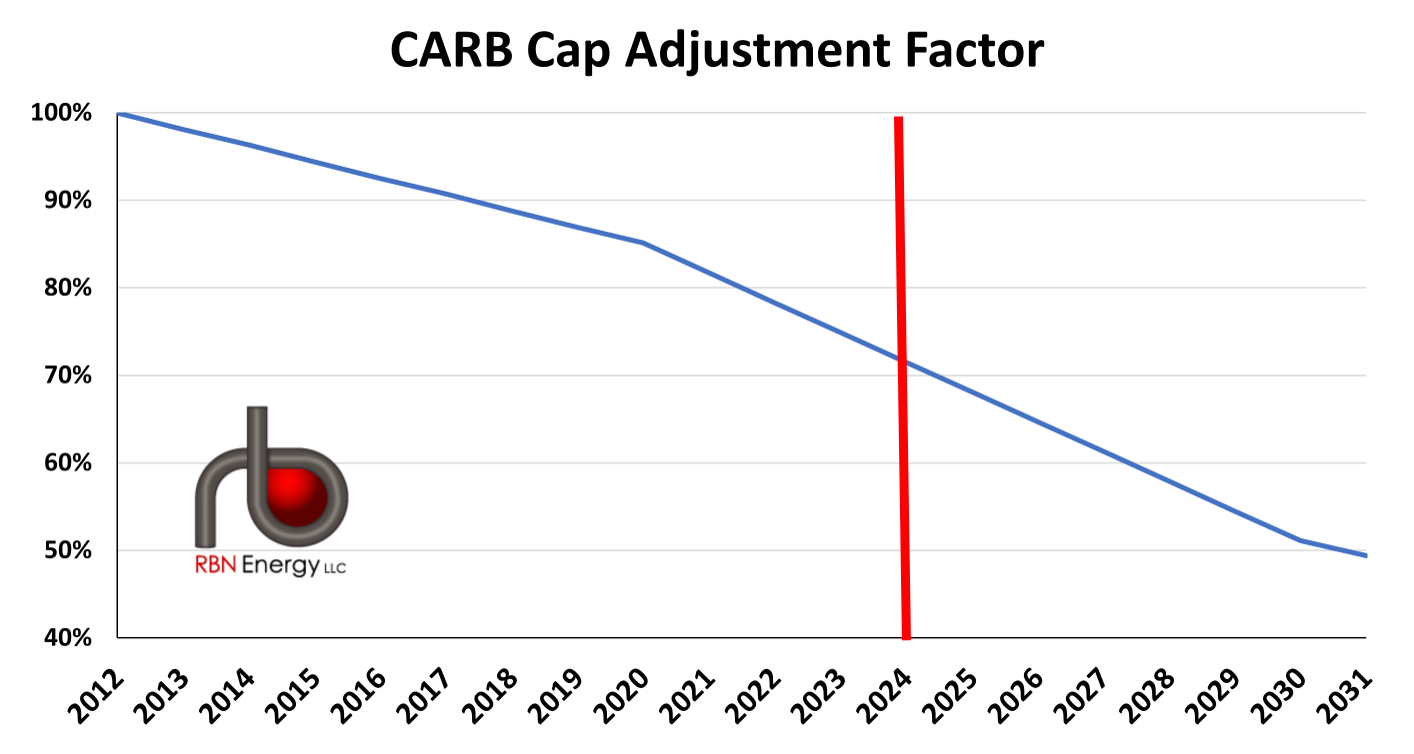

Figure 1. CARB Cap Adjustment Factor, 2012-31. Source: CARB

About the song

“Over the Hills and Far Away” was written by Jimmy Page and Robert Plant and appears as the third song on side one of Led Zeppelin’s fifth studio album, Houses of the Holy. Page and Plant wrote the song at Bron-Yr-Aur, a small cottage they rented in the Welsh countryside after finishing a massive North American tour with Led Zeppelin in 1970. The tune was originally called “Many, Many Times.” The intro section is played by Page on acoustic guitars, utilizing Eastern-influenced pull-offs in the key of G that Page is fond of. The midsection of the song is led by the band and guitar-driven riffs, followed by a quiet outro featuring Page on guitar and pedal steel guitar. The song was released as the first single from the album in May 1973 and went to #51 on the Billboard Hot 100 Singles chart. Personnel on the record were: Robert Plant (vocals), Jimmy Page (guitars, pedal steel), John Paul Jones (bass, piano, organ, Mellotron, synthesizer), and John Bonham (drums).

Houses of the Holy was recorded between December 1971-August 1972 with The Rolling Stones Mobile Studio at Headley Grange and Stargroves, and at Island and Olympic studios in London, with Jimmy Page producing and Eddie Kramer engineering. The album was released in March 1973 and went to #1 on the Billboard 200 Albums chart. It has been certified 11x Platinum by the Recording Industry Association of America. Two singles were released from the LP.

Led Zeppelin were an English rock band formed in London in 1968 by Jimmy Page, Robert Plant, John Paul Jones, and John Bonham. The iconic band is one of the best-selling bands of all time, with close to 300 million records sold worldwide. They have released eight studio albums, four live albums, 10 compilation albums, and 16 singles. They are members of the Rock and Roll Hall of Fame, UK Music Hall of Fame, and are recipients of Kennedy Center honors. They have Lifetime Achievement Awards from the Ivor Novello Awards and the Grammy Awards. In 2005, Page was appointed an Officer of the Order of the British Empire, and in 2009, Plant was honored as a Commander of the Order of the British Empire. After the death of drummer John Bonham in September 1980, the band broke up. The surviving members of Led Zeppelin have sporadically participated in one-off reunions, most notably in 2007, with John Bonham’s son, Jason, on drums. All three surviving members of the band have gone on to successful solo and collaborative careers. An upcoming documentary film, recently renamed Introducing Led Zeppelin, is awaiting a release date.