Guyana’s crude oil production is surging, a trend that is expected to continue through the rest of the decade, and with no domestic refining industry its exports are booming. Shipments of Guyana’s medium-density, sweet-ish crude to the U.S. have ramped up and are increasingly making their way to the West Coast, which relies on imports given its lack of easy access to domestic shale crudes and limited regional output. In today's RBN blog, the second in a series, we‘ll examine where Guyana’s barrels are ending up and how they stack up against competing grades.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

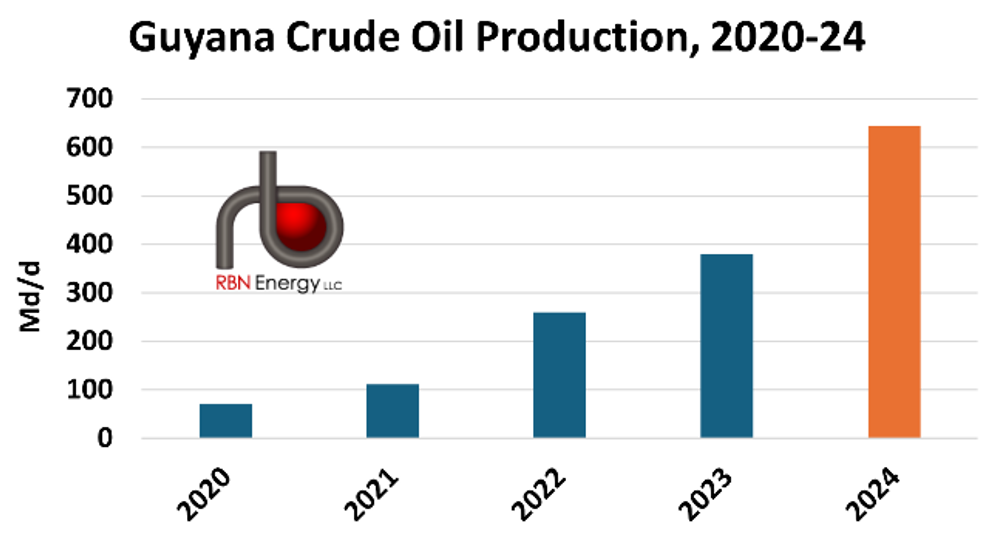

As we discussed in Break My Stride, Guyana’s crude oil production has accelerated from 70 Mb/d in 2020 to 380 Mb/d in 2023 (blue bars in Figure 1 below) and is expected to reach 645 Mb/d this year (orange bar). All of Guyana’s output comes from a single offshore block known as Stabroek, which spans 6.6 million acres and has reserves most recently estimated at 10 billion barrels of oil equivalent (boe). Stabroek (the old name for Georgetown, Guyana’s capital city) is being developed by partners ExxonMobil (45%), Hess (30%) and China’s CNOOC (25%). ExxonMobil, which also serves as the operator, began oil and gas activities there in 2008, collecting and evaluating 3D seismic data. It drilled its first well in 2015, leading to the group’s first significant oil find, which is known as the Liza project. Phase 1 of Liza began production in late 2019; then came Liza Phase 2, which began service in 2022; and then Payara in 2023. The consortium has since identified over 30 oil and gas discoveries in Stabroek. (All of this is happening as the three partners are embroiled in a legal fight and the government deals with a years-long territorial dispute with Venezuela.)

Figure 1. Guyana Crude Oil Production, 2020-24. Source: EIA

Three floating production, storage and offloading vessels (FPSOs) named Liza Destiny, Liza Unity and Prosperity have been extracting oil and gas from the Liza 1, Liza 2 and Payara projects, respectively. The extracted oil is temporarily stored in the FPSOs, then transferred to export tankers using hoses. The production facilities can receive a wide variety of ship classes, including Very Large Crude Carriers (VLCCs; capacity about 2 MMbbl), Suezmaxes (800 Mbbl-1 MMbbl) and Aframaxes (500-750 Mbbl).

About the song

“My Guy” was written by Smokey Robinson and appears as the third song on side one of Mary Wells’s fourth studio album, Mary Wells Sings My Guy. It was produced by Smokey Robinson and recorded at Hitsville U.S.A. Studio A in Detroit in 1964. Released as a single in March 1964, it went to #1 on the Billboard Hot 100 Singles chart. Many artists have covered the song, including Petula Clark, Sister Sledge, Aretha Franklin and Melba Moore. The song was inducted into the Grammy Hall of Fame in 1999. Trombonist George Bohanon and keyboardist Earl Van Dyke came up with the opening intro by combining “Canadian Sunset” with “Begin the Beguine.” Personnel on the record were: Mary Wells (lead vocals), The Andantes (backing vocals), Earl Van Dyke (keyboards), Johnny Griffith (piano), Eddie Willis, Robert White (guitars), James Jamerson (bass), Benny Benjamin (drums), Dave Hamilton (vibes), Herbert Williams, John Wilson (trumpet), and Paul Riser and George Bohanon (trombone).

Mary Wells Sings My Guy consists of songs Mary Wells recorded for Motown at Hitsville U.S.A. in Detroit in 1963-64 and features the hit single “My Guy.” It was Mary Wells’s last album for Motown as she signed with 20th Century Fox Records at the beginning of 1965. Produced by Smokey Robinson, the album was released in May 1964.

Mary Wells was an American R&B singer and songwriter who helped define the sound of Detroit's Motown Records in the early 1960s. She released 13 studio albums, one live album, two compilation albums and 44 singles. She had 18 Top 40 R&B hits in her career. In 1989 she was awarded a Pioneer Award from the Rhythm & Blues Foundation. She was inducted posthumously into the National Rhythm & Blues Hall of Fame in 2017. Mary Wells died in Los Angeles in July 1992 at the age of 49.