The Light Louisiana Sweet (LLS) crude market has evolved in recent years, due largely to the reversal of the Capline pipeline as well as limited production growth from the offshore fields that contribute to the LLS market. Yet the LLS premium against other U.S. grades remains strong, a sign that refiners aren’t ready to give up on it just yet, given its attractive yields of high-value transportation fuels like gasoline, jet fuel and diesel. In today’s RBN blog, we will revisit LLS and examine its production and demand outlook.

The Crude Oil Billboard keeps readers at the forefront of the U.S. crude oil market by offering access to data and information moments after its release. Say goodbye to PDF reports that come out after the market has already moved on.

Long before the Magellan East Houston (MEH) assessment was established in 2016, LLS — a light, low-sulfur regional benchmark that is often the priciest in the U.S. physical crude complex — was the preeminent marker that determined the balancing point between imports and exports. U.S. refiners would track the grade’s differential to global benchmark Brent crude to weigh the merits of taking barrels from the North Sea or the Middle East instead. LLS has an API gravity of 34-41 and 0.4% (maximum) sulfur. (As we noted in The Weight, crude’s gravity or density is usually measured in terms of its API number; the higher the API, the lighter, or less dense, the crude). Even though LLS is considered a superior grade to most other U.S. crudes because of its lucrative fuel yields, its profile diminished after the Shale Revolution unleashed much higher volumes of similar, light, low-sulfur (sweet) crudes that compete with it. While some of this bountiful shale production is blended into LLS, keeping it amply available may not be as easy, as there are headwinds coming up for the grade over the next few years, which we will address in today’s blog.

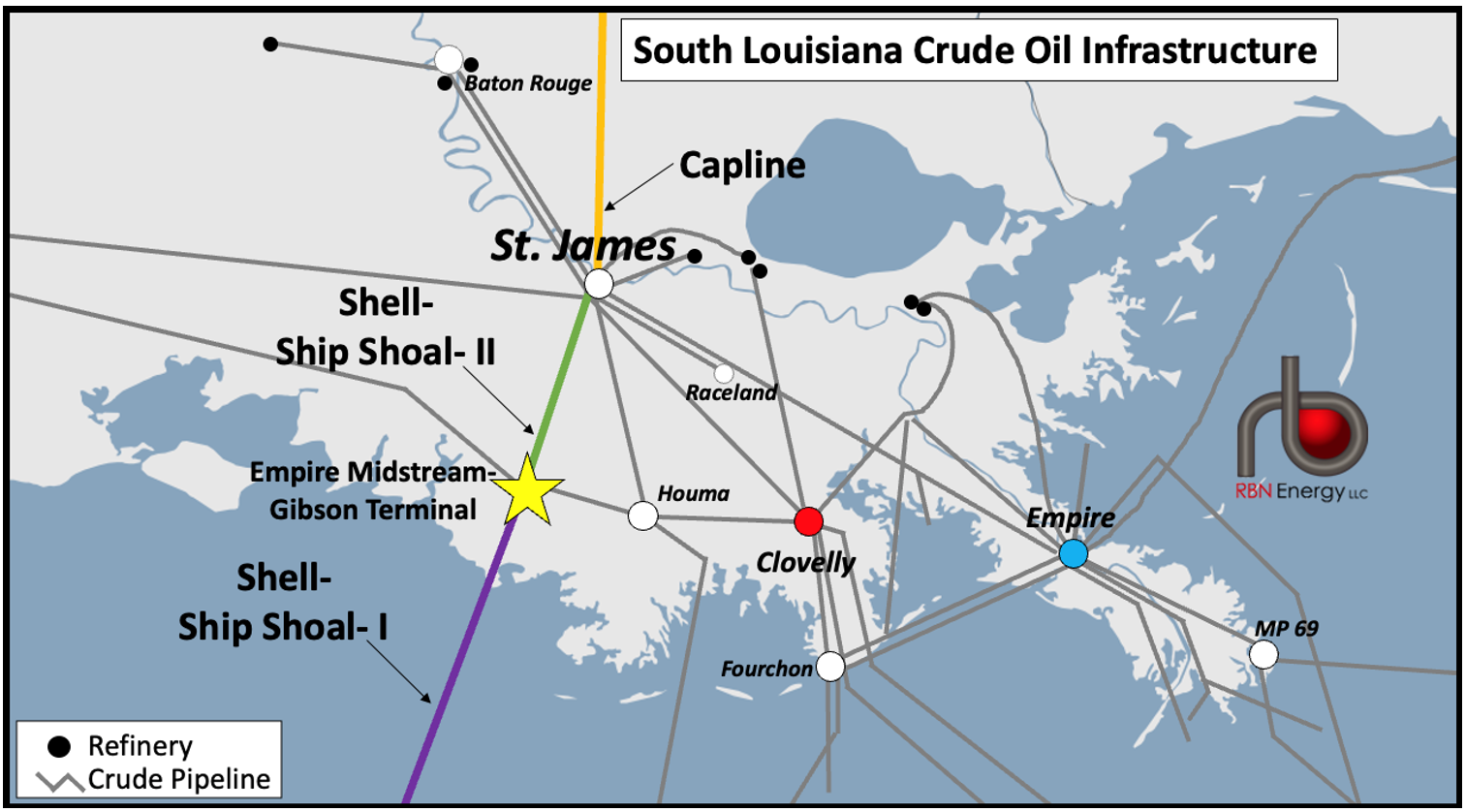

Figure 1. South Louisiana Crude Oil Infrastructure. Source: RBN

Let’s start with the crudes that make up LLS. Its sources have broadened significantly beyond field production in the Gulf of Mexico (GOM) in recent years. In fact, blended volumes have long dominated the LLS pool, with the grade’s output from offshore fields (known as pure LLS) accounting for only a small fraction of total supply. LLS availability is estimated at 300-350 Mb/d, of which roughly 10% (~30 Mb/d) comes from offshore fields. A decade ago, pure LLS contributed up to 30% of the blend. There may have been quality issues in blended LLS, but not severe enough to keep buyers away, with the market largely accepting the two versions — pure and blended — as intrinsically part of the overall grade. LLS usually trades for delivery at St. James, LA, (see Figure 1 above) a major U.S. oil hub that offers access to rail and water (it lies just 60 miles up the Mississippi River from the Gulf) and, most importantly, connectivity with multiple onshore and offshore pipes, a big bonus for LLS buyers and producers.

About the song

“Will You Still Love Me Tomorrow” (also known as “Will You Love Me Tomorrow”) was written by Gerry Goffin and Carole King. It appears as the fourth song on side one of The Shirelles’ debut album, Tonight’s the Night. It was recorded at Bell Sound in New York City and produced by Luther Dixon. When the song was first presented to Shirelles singer Shirley Owens, she thought it sounded “too country.” The subject matter in the lyrics dealing with young romance resulted in some radio stations refusing to play it initially, but that didn't last long. Released as a single in November 1970, it became #1 on the Billboard Hot 100 Singles chart. It was the first #1 single for a black, all-female group. The song has been covered by many artists including The Four Seasons, Smokey Robinson, Linda Ronstadt and the song’s co-author, Carole King, who included it on her multi-platinum album, Tapestry. Personnel on the record were: Shirley Owens (lead vocals), Doris Coley, Addie “Micki” Harris, Beverly Lee (backing vocals) and various unnamed New York studio musicians.

Tonight’s the Night is the first studio album released by The Shirelles. Recorded between 1959 and 1960 at Bell Sound in New York City and produced by Luther Dixon, the album was released in December 1960. In 2022, the album was selected by the Library of Congress for preservation in the National Recording Registry. Producer Luther Dixon, who also had a hand in the songwriting of the album with The Shirelles, helped produce a collection of songs that exemplified teenage angst and young love in the late 1950s and early 1960s. Two singles were released from the LP.

The Shirelles were formed in 1957 at the high school in Passaic, NJ, that the quartet attended. They released 13 studio albums, eight compilation albums, and 49 singles. They are members of the Rock and Roll Hall of Fame, Vocal Group Hall of Fame, and have a Pioneer Award from the Rhythm and Blues Foundation. Founding Member Micki Harris died in June 1982, and Doris Coley died in February 2000. Original members Shirley Owens (now Shirley Alston Reeves) and Beverly Lee still tour separately with various members as The Shirelles.