Natural gas production seems totally dependent on NGLs. In turn, NGLs are highly dependent on petrochemical crackers. How does this work? What could go wrong? That’s the topic of this multi-part series on NGLs in the petrochemical industry. Part I is an overview of the market dynamics involved and will set us up for going deep into the math of petrochemical feedstocks. So let’s get cracking.

In the shale era - circa 2012, the economics of natural gas are being driven by natural gas liquids. Where there is high BTU production (“wet” gas that contains a large quantity of NGLs), producer rates of return are in the 50% - 100%+ range. Where there is low BTU (“dry”) gas, producer rates of return are negative or low-single-digits at best, rig counts are falling, and production is declining (Except for one stellar exception, discussed in the “Defying Gravity” box at the bottom of this post). This disparity in natural gas returns is a function of the price differential between natural gas and crude oil. Natural gas is cheap. Crude oil is expensive. NGL prices are heavily influenced by the price of crude oil. So gas that contains a high percentage of NGLs (that can be extracted and moved to NGL markets) is simply worth a lot more than natural gas that has few NGLs.

But if natural gas liquids have become all-important in the natural gas industry, what sets the price of those products collectively called NGLs – ethane, propane, normal butane, isobutane and natural gasoline? The answer is that ‘it depends’. It depends on which NGL you are talking about, the season of the year and a complicated set of dynamics in the petrochemical industry.

Of all of these factors, none is more important than petrochemicals. That’s because the sector makes up more than half of the demand for all NGLs. For ethane, the petrochemical sector is 100% of the market for this product. About one-third of propane goes to the petchems (historically with higher volumes going to the petchems in the summer), and some butane and natural gasoline.

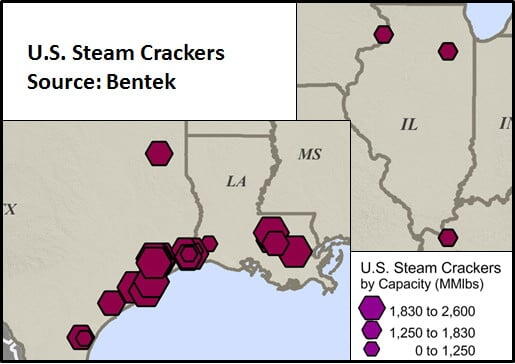

So it’s all about the crackers – a.k.a., ethylene crackers, steam crackers, olefin units. These are different names for the same plants. Most of these things are located along the Texas/Louisiana Gulf Coast, but there is one in Longview, TX and three in the Midwest. See map below.

What are these things, and what do they make? They are huge facilities. Each plant has a number of furnaces, which are multi-story infernos that heat the feedstock to extremely high temperatures in the presence of steam for a very short period of time. To stare into the view port in one of these furnaces is to look into the pit of hell – a giant space filled with pipes and fire.