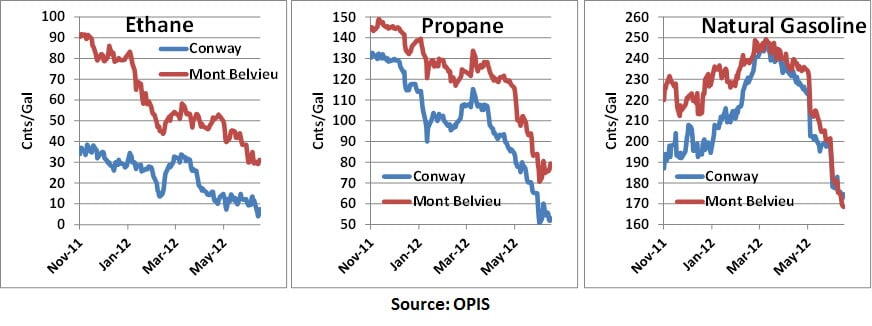

On Wednesday of last week, Conway ethane dropped to 4 cnts/gal, another multi-decade low for any natural gas liquid and an 86% decline in the ethane price since the first of the year. But Conway ethane is not the only NGL that has been suffering. As shown in the graph below, ethane propane and natural gasoline are all off hard as high propane inventories combined with a $20/bbl decline in the price of crude oil rippled through NGL markets. What do changes in the prices of these NGLs mean for the relative value of each NGL as a petrochemical feedstock? Could we see natural gasoline start competing against ethane and propane? To answer these questions and to understand how natural gasoline petrochemical feedstock economics compare to ethane and propane numbers, we’ll dive one last time into our petchem spreadsheets.

This is Part V of our series on petrochemical feedstock economics. The first two parts were background information covering the fundamentals of ethylene crackers and how feedstock economics work. In Part III we went into the details of ethane economics and in Part IV did the same for propane. These are the ‘light’ ethylene feedstocks. (You’ll probably have a hard time following this one if you didn’t read Parts III and VI.) There are several ‘heavy’ feedstocks, including normal butane, natural gasoline, light naphthas, heavy naphthas, and gas oil. Rather than looking at each of these we are going to focus on natural gasoline as our representative heavy feedstock. We noted in Part IV that almost 90% of U.S. ethylene feedstocks in 2012 are either ethane or propane. Of the remaining 10%, most of that is either light naphtha or natural gasoline, which we are going to treat here as the same thing.

Natural Gasoline and Light Naphthas

Essentially both of these streams are predominately C5 and C6 with small percentages of heavier hydrocarbons. Natural gasoline is the C5/C6 stream that comes from natural gas processing plants. Naphthas come from refineries. While there are some differences in the olefin content, sulfur and various impurities in each of these streams, from an ethylene yield perspective the streams are essentially equivalent, assuming the ethylene cracker is can handle the quality specifications of the stream.

A few other miscellaneous facts about natural gasoline before we get into the numbers. First, natural gasoline is the only NGL which is liquid at atmospheric pressures and temperatures. It is similar to a very low octane motor gasoline, and in fact a primary market for natural gasoline is as a motor gasoline blendstock. Second, traditionally natural gasoline is much cheaper than motor gasoline and thus is used to lower the cost of the overall motor gasoline pool for gasoline blenders. Over the past few years that has been somewhat less true because of a new source of demand for natural gasoline – oil sands diluent. That’s our third miscellaneous fact - There is a lot of natural gasoline that moves into Alberta for use as a diluent (see It’s a Butumen and various other RBN blog postings). Fourth, natural gasoline is the NGL who’s price is the most highly correlated to crude oil prices. So note in the graphic above that natural gasoline fell from $2.50s/gallon in March to $1.70s/gallon last week, but that’s only down about 30% from the highs in March versus the much larger percentage declines for ethane and propane. Also note that Conway and Mont Belvieu prices are about the same versus significant differentials for ethane and propane. That is because Conway natural gasoline is being supported by the diluent market in Canada and thus Conway natural gasoline does not need to move south into Mont Belvieu to balance supply and demand. The impact of that difference between the light and heavy feedstocks will become apparent as we get into the feedstock equivalence numbers.

One final note. In this series we are ignoring the economics for cracking normal butane and gas oil. Together these feedstocks make up less than 2.5% of feedstocks run in the U.S., and as such can be ignored in our simplified analysis. If it were 10 years ago in the U.S. or if we were looking at cracking economics in Europe or the Far East, it would be necessary to include these feedstocks in our analysis.