After thoroughly alienating their investor base over more than two decades of boom-and-bust cycles, U.S. E&Ps won investors back in the early 2020s by radically transforming themselves from high-risk to high-yield vehicles. Fueled by surging crude oil and natural gas prices in 2022, producers generated massive free cash flows — and spectacular shareholder returns that topped 10% during the late-2022 peak. Prices and cash flows subsequently retreated, however, and skeptics worried about the sustainability of producers’ high-return strategy. Would debt repayment, dividends and share buybacks sink? In today’s RBN blog, we‘ll review the Q1 2024 cash allocation of the major U.S. E&Ps with a spotlight on current dividend yields.

NATGAS Billboard is a daily, early morning email and report that provides an up-to-the-minute view of the natural gas market outlook, including storage injections/withdrawals and price. Billboard’s models incorporate pipeline flow data, weather models, electricity demand data and more.

First, let’s quickly review how far the E&P sector has come. The S&P E&P Index — formally known as the S&P Oil & Gas Exploration & Production Select Industry Index — retreated from its peak of over 12,000 in mid-2014 to between 4,000 and 6,000 for most of the 2015-19 period and plunged to a low of just 1,224 in March 2020. However, after seven years of negative returns, the shift to a shareholder focus in the wake of COVID resulted in a near doubling of that index through the balance of 2020 and 67% and 46% total returns in 2021 and 2022, respectively, that helped quadruple the index to the 5,500 range. The index remains there today, despite a decline in cash flows that resulted in a very modest 3.8% return in 2023. And, as we recently outlined in Devil’s in the Details, Q1 2024 earnings stabilized at a historically solid level. But what about shareholder returns and dividend yields?

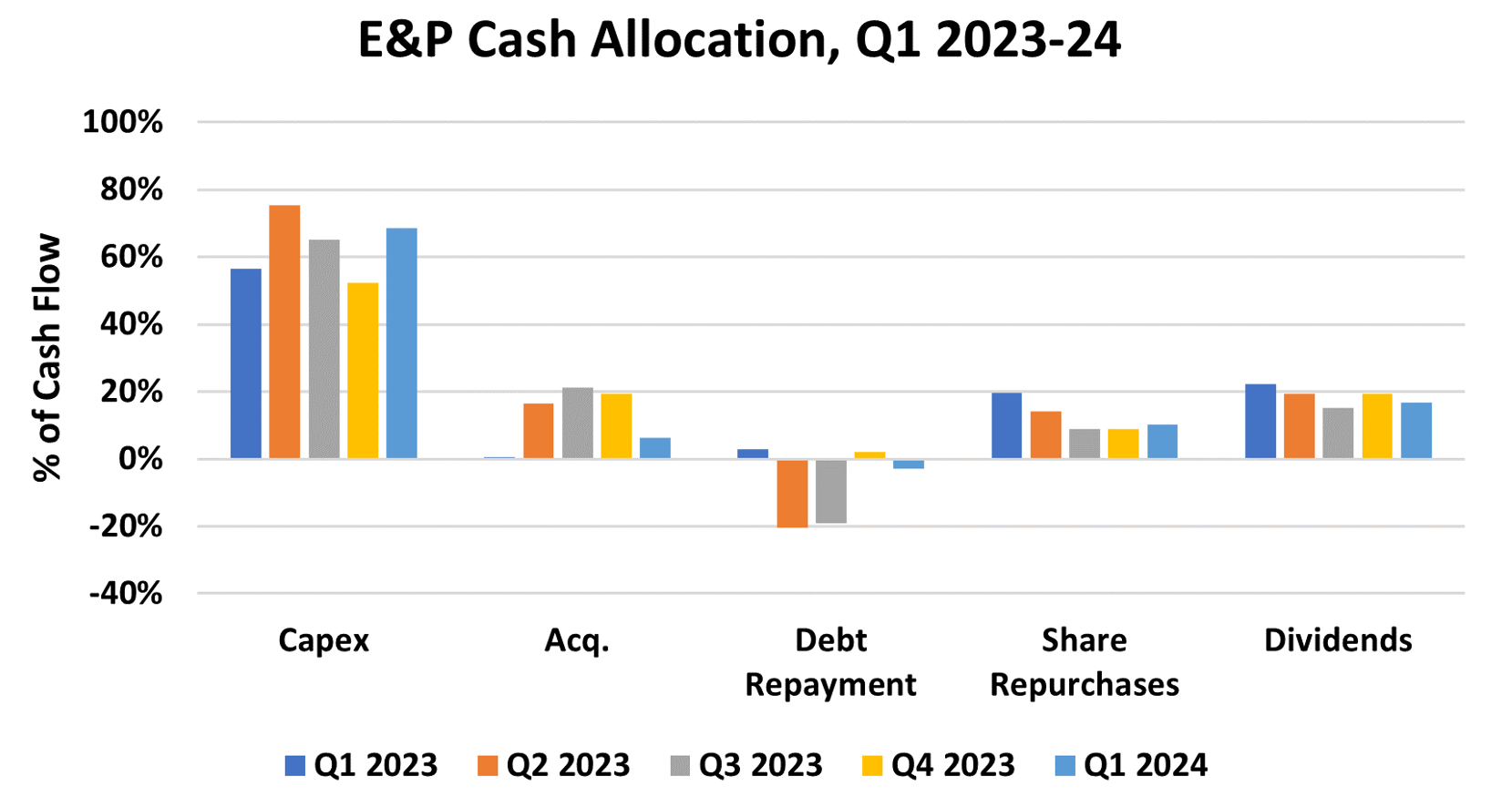

The 42 U.S. E&Ps we cover generated a combined $27.3 billion in cash flow from operating activities (CFOA) during Q1 2024, down 16% from Q4 2023 and 14% less than the $31.9 billion generated in Q1 2023. But capital outlays rose to $18.7 billion in the first three months of 2024 — 10% higher than Q4 2024 and 4% more than Q1 2023. As shown in Figure 1 below, the capital spending and CFOA data yielded a 68% reinvestment rate during Q1 2024 (light-blue bar in Capex grouping to far left), higher than the 52% recorded in Q4 2023 (gold bar) and 57% in Q1 2023 (dark-blue bar). Lower CFOA and higher capex resulted in a 45% drop in free cash flow (FCF) to $8.6 billion in Q1 2024, 45% below the $15.6 billion reported in Q4 2024 and 38% below the $13.8 billion recorded in Q1 2023. Acquisition spending (second grouping in chart) was $1.7 billion in Q1 2024 — or only 6% of E&P cash allocation (light-blue bar) — nearly three quarters less than the $6.3 billion reported in Q4 2023. As we mentioned recently in Like a Rock, while E&P balance sheets remain strong, debt repayment (third grouping) on a mass scale has ended. To that end, debt increased by $859 million in Q1 2024, compared with a $710 reduction in Q4 2023 and a $918 million reduction in Q1 2023.

Figure 1. E&P Cash Allocation, Q1 2023-24. Source: Oil & Gas Financial Analytics, LLC

About the song

“I Want to Pay You Back (For Loving Me)” was written by Chi-Lites producer, arranger and lead vocalist Eugene Record. It appears as the third song on side one of The Chi-Lites’ third studio album, (For God’s Sake) Give More Power to the People. It keeps in line with the group’s penchant for long titles, including parenthesis in their work. Released as a single from the album in September 1971, it went to #25 on the Billboard R&B and #95 on the Billboard Hot 100 Singles charts. Personnel on the record were: Eugene Record (lead vocal, production, arrangement), Robert “Squirrel” Lester, Creadel “Red” Jones, and Marshall Thompson (backing vocals). Unlisted session musicians and string players provided the musical accompaniment.

(For God’s Sake) Give More Power to the People was recorded between 1970-71 for the Brunswick record label. Released in July 1971, it went to #3 on the Billboard Top Soul and #12 on the Billboard 200 Albums charts. It produced the hit single “Have You Seen Her,” which went to #1 on the Billboard R&B and #3 on the Billboard Hot 100 Singles charts. The album’s songwriting reflected the group’s interest in social change exemplified at the time by Sly and the Family Stone and fellow Chicagoan Curtis Mayfield. Three singles were released from the LP.

The Chi-Lites are an American R&B vocal group formed at Chicago’s Hyde Park High School in 1959 by seven student vocalists. The group became a quartet during their hit-making years of the late 1960s and early 1970s consisting of Eugene Record, Marshall Thompson, Creadel Jones and Robert Lester. They have released 18 studio albums, 15 compilation albums, and 64 singles. They are members of the Vocal Group Hall of Fame, Rhythm and Blues Foundation, and have a star on the Hollywood Walk of Fame. Eighteen members have passed through the group since its formation. Founding member Marshall Thompson, along with four other vocalists, still tour as The Chi-Lites. They will be performing a few select concerts in July and August in the U.S. Founding member Creadel Jones died in Glendale, CA, in August 1994. Eugene Record died in Chicago in July 2005. Robert Lester died in Chicago in January 2010.