The transition of U.S. E&Ps to capital discipline has led to historic shareholder returns and won back legions of investors who had virtually abandoned the industry until a few years ago. But while it might be tempting to conclude producers must finally have their financial houses in good order, a lot of us have witnessed a few boom-and-bust cycles in our time and remain hypervigilant for any signs of financial instability, especially considering that commodity prices could weaken at any time. In today’s RBN blog, we analyze the impact of lower price realizations and capital allocation decisions on the balance sheets of the major U.S. independent oil and gas producers.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

As we reviewed in If You’ve Got the Money, Honey, lower price realizations and higher capital spending reduced free cash flow for the 44 E&Ps we cover by about 50% to $45.6 billion in 2023. Understandably, producers weren’t able to sustain the record shareholder returns of 2022 as share repurchases and dividends fell by 43% and 25%, respectively. However, buybacks and dividends were still significantly higher than any year prior to 2022. To partially fund these returns and help finance a record wave of E&P M&A activity, our companies added about $8.5 billion in net debt. The question is, what impact did all this have on their balance sheets?

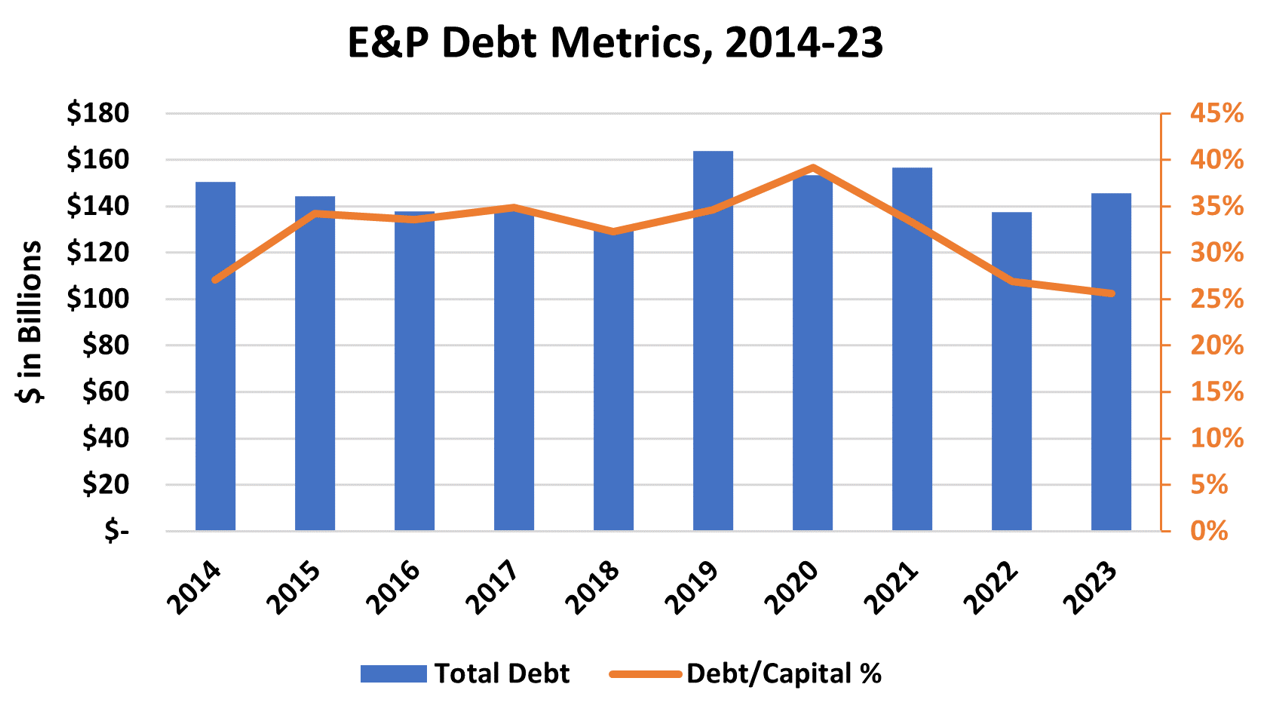

The answer is E&P credit metrics held remarkably steady in 2023 and remained historically strong. As shown in Figure 1 below, the debt-to-capital ratio (orange line and right axis) for the companies we cover actually dipped to a decade-best 26% in 2023, down slightly from 27% in 2022, despite the increase in total debt (right-most blue bar and left axis) as investor support for the industry stayed robust. The debt-to-capital ratio had exceeded 30% in every year from 2015 to 2021, peaking at 40% in the pandemic-influenced 2020.

Figure 1. E&P Debt Metrics, 2014-23. Source: Oil & Gas Financial Analytics, LLC

About the song

“Like a Rock” was written by Bob Seger and appears as the second song on side one of Bob Seger’s 13th studio album of the same name. The song is best known for being featured in Chevy truck TV commercials during the 1990s and early 2000s. Ironically, Seger’s father worked for Ford Motor Company in Detroit while Seger was growing up. Released as a single in May 1986, it went to #12 on the Billboard Hot 100 Singles chart. Personnel on the record were: Bob Seger (lead vocals), Chris Campbell (bass), Craig Frost (organ), Dawayne Bailey (acoustic guitar), Rick Vito (slide guitar), Russ Kunkel (drums), Billy Payne (piano), and Douglas Kibble, The Weather Girls (backing vocals).

The album, Like a Rock, was recorded in early 1986 at Criteria in Miami and Capitol in Hollywood, with production by Punch Andrews, David N. Cole and Bob Seger. The live version of CCR’s “Fortunate Son” was from a recording at Cobo Hall in Detroit done in 1983. Released in April 1986, it went to #3 on the Billboard 200 Albums chart and has been certified Platinum by the Recording Industry Association of America. Four singles were released from the LP.

Bob Seger is an American rock singer, songwriter and musician from Detroit. He started playing professionally while a student at Ann Arbor High School in 1961. His first Detroit-area hit single was “East Side Story,” released by Bob Seger and the Last Heard in January 1966. His commercial breakthrough was the album Night Moves, released in October 1976. It remains Seger’s best-selling LP. He has released 18 studio albums, two live albums, five compilation albums and 68 singles. He has sold more than 75 million records worldwide. He was inducted into the Rock and Roll Hall of Fame in 2004 and the Songwriters Hall of Fame in 2012. After his farewell tour of 2018-19, Seger retired from the music business.