If the flood of new crude arriving at the Gulf Coast during the first six months of 2014 overwhelms refiners in the region, then the pricing consequences may very well be quite radical. Could prices at the Gulf Coast flip to trade at a discount to West Texas Intermediate (WTI) crude delivered at the Cushing hub that is home to the CME NYMEX contract? Even if Gulf Coast crude retains its premium over WTI, deep discounts may be required to encourage refiners to process increasing quantities of light sweet crude. A downward spiral of crude prices could ensue. Today we lay out possible price scenarios.

This is Part 2 of a two-part review of Gulf Coast crude price differentials that extends a series on the impact of the flood of new crude expected to arrive at the Gulf Coast that we started back in November (2013). In Part 1 of this review we covered the evolution of Gulf Coast price differentials since 2012 and our base case scenario for 2014 where Light Louisiana Sweet (LLS) at the Gulf Coast maintains a $3/Bbl premium to WTI and international crude Brent trades at a $10/Bbl to WTI. Earlier in the series we described how 4 MMb/d of current and planned expansions to crude transportation capacity are coming to the Texas Gulf Coast region (see Handling The Texas Gulf Coast Crude Flood). Our analysis showed that the new incoming light crude capacity will exceed Texas Gulf Coast demand by somewhere north of 0.5 MMb/d by the end of 2015. In episode two we described how some of these excess crude supplies would move east on the reversed Ho-Ho pipeline (see Gulf Coast Crude West to East Flows). In episode three we looked at how shippers could divert supplies away from Texas Gulf Coast congestion (see Texas Gulf Coast Bypass Options). Episode four looked at progress bringing TransCanada’s Keystone XL Gulf Coast extension (a.k.a, Cushing Marketlink Pipeline (CMP)) online (see Keystone Marketlink Comes to Texas). Episode five looked at the impact of the twin Seaway Pipeline from Cushing to Freeport expected online during the second quarter of 2014 (see Impact of the Seaway Expansion).

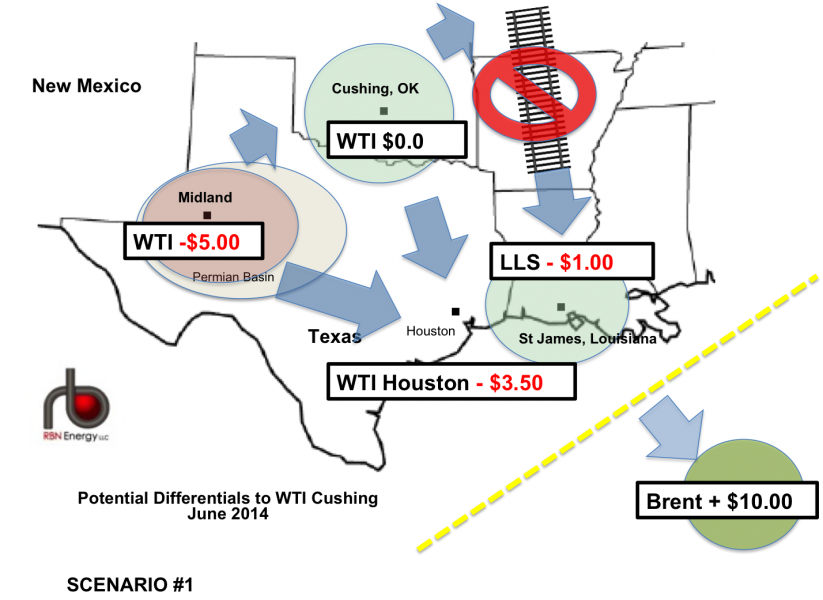

Scenario #1 – A Houston Flood of Crude Oil Sends Gulf Coast Prices Diving

In our first 2014 light sweet crude price scenario (see the map below) the flood of supplies arriving on new pipelines pushes down prices in Houston and St James Louisiana below those for WTI at Cushing. Prices for WTI in Houston – the center of the “flood” of light sweet crude are pushed $3.50/Bbl below Cushing. Refiners are oversupplied at the Gulf Coast while there is a shortage of crude at Cushing as producers scramble to find supplies to fill their commitments to ship to Houston on the new pipelines and to feed the Midwest market. The worst impact of this scenario is felt at Midland, TX the trading hub close to Permian Basin production in West Texas. Low prices in Houston create a strong disincentive for crude to flow from Midland to Houston and a strong incentive for crude to flow from Midland to higher priced Cushing. However, the available capacity from Midland to Cushing is far less than production so pipeline congestion causes Midland WTI to trade at a $5/Bbl discount to WTI Cushing. This price spread incentivizes Permian producers to use rail alternatives to ship crude away from the Gulf Coast to the West Coast or to the Midwest.

Source: RBN Energy (Click to Enlarge)

Meanwhile the discounted price at Houston leads to flows out of the region on the newly opened Ho-Ho reversal that will ship 375 Mb/d to St James, LA. However, partly because of the Ho-Ho flows, the Houston oversupply is also affecting St James. Prices for LLS at St. James are therefore $1.00/Bbl lower than WTI but still $2.50/Bbl higher than WTI in the flooded Houston market – the difference being the cost of transport on Ho-Ho. So long as crude is being pushed out of Houston to Louisiana, no imports of light sweet are needed at the Gulf Coast and Brent remains detached from Gulf Coast crude prices – as it has been since September 2013.

We put a nominal price of $10/Bbl on the Brent premium to WTI for Scenario #1 but note that premium depends on world oil market supplies. If there are shortages of light sweet crude outside the US, then the Brent premium will be higher. As long as Brent is at a premium to WTI of $10/Bbl and the US East and West Coast markets are still importing light sweet crude, there will be incentives for US producers to ship crude to these coastal markets where prices will be higher than Cushing or the Gulf Coast. Crude volumes sent by rail from the Bakken to the East and West Coasts will be far higher than volumes sent to the Gulf Coast (hence the “no entry” sign on the railroad on the map). Permian producers will ship crude by rail to the West Coast whenever the netback is better than selling at Midland or shipping to the flooded Houston market. Eagle Ford producers will be incentivized to move crude from South Texas to East Coast refineries and to increase exports to Canada.

Even though Gulf Coast prices are lower than Cushing in Scenario #1, the Houston flood continues because of the lack of takeaway alternatives for crude from the Eagle Ford and Permian Basins meaning that these crudes have no option but to flow to the Texas Gulf Coast. New pipeline capacity by mid-2014 from the Permian to Houston (Expansion to the Longhorn – 50 Mb/d, Permian Express Phase 1- 150 Mb/d and BridgeTex - 300 Mb/d) will increase flows into Houston and Port Arthur. In addition, shippers unable to avoid moving contracted volumes (without paying a “take or pay” penalty) on the expanded Seaway (+450 Mb/d) and the Cushing Marketlink Pipeline (+700 Mb/d) will maintain downward pressure on crude prices at the Coast.

If the price differentials in Scenario #1 are maintained for long, they could cause a downward spiral in US crude prices. That is because the higher Cushing price could attract too much crude to that hub pushing Cushing WTI prices down and with them the Gulf Coast crudes. The more Cushing barrels that flow to the Gulf Coast the greater the downward pressure on WTI prices in Houston and in turn on LLS at St James. The only “cure” for the price discounting will come when Gulf Coast refineries that were not designed to process light crude start to process these crudes anyway because they are so cheap. So long as crude prices are low enough these refiners may be able to accommodate more light crude by reducing their total throughput volumes – eventually soaking up the excess supply. The sixty four thousand dollar question is – at what absolute crude price will supply and demand balance in 2014? Given this scenario, our outlook would be for prices less than $85/Bbl.

Scenario #2 – Gulf Coast Refiners Soak Up the Flood

Scenario #2 is a little less frightening and shown in the map below. In this case, Gulf Coast prices retain pretty much their current premium over Cushing. WTI at Houston and LLS at St James trade at a $3/Bbl premium over WTI at Cushing – roughly equivalent to the pipeline transport cost. WTI at Midland is $2/Bbl lower than the price at Cushing – encouraging flows to Houston over flows to Cushing. In this scenario crude is encouraged to flow to Houston on the new capacity opening up that we mentioned earlier. The Gulf Coast still has sufficient light sweet crude not to need any imports – so Brent remains disconnected. However, Gulf Coast refiners are soaking up enough domestic light sweet crude to keep Gulf Coast prices from collapsing in the way we described in Scenario #1.

The big difference in this scenario is that the Brent premium to WTI is only $5/Bbl rather than the $10/Bbl in Scenario #1. As we said earlier – so long as the Gulf Coast does not need imports of light sweet crude then the price of Brent is not material to that market (assuming that international prices are higher than domestic prices). However, the size of the Brent premium is an important consideration. That is because a weak Brent premium reduces the incentive for producers to ship light crude to the East and West Coast markets by rail. That lack of incentive will cause supplies of crude in the Bakken to back up – meaning prices in North Dakota will be discounted to WTI. Producers in the Bakken will be incented to ship supplies by pipeline to Cushing and (via Seaway and Cushing Marketlink) to the Gulf Coast.

Join Backstage Pass to Read Full Article