Alaska North Slope (ANS) crude oil production has been sliding for years — decades really — but that is poised to change in the second half of the 2020s. Two long-planned ANS projects — Pikka and Willow — are slated to start up in 2026 and 2029, respectively. By the early 2030s, these and other projects in the works could return North Slope production to levels not seen since the turn of the century. In today’s RBN blog, we’ll discuss these projects and our new, long-term forecast for ANS oil production — a topic in our upcoming Future of Fuels report.

The Future of Fuels bi-annual report by RBN's Refined Fuels Analytics provides an in-depth analysis of the U.S. and global refinery industries, focusing on crude oil and fuel market dynamics, supply and demand, alternative fuels, refinery capacities, and price forecasts to help stakeholders navigate the evolving energy landscape.

Let’s start with the main source of Alaska’s crude oil production: Prudhoe Bay on Alaska’s North Slope. As we discussed in Keep Holding On, more than a half-century ago the 49th state was seen as the next big thing for U.S. oil. Massive oil deposits were discovered at Prudhoe Bay in the late 1960s –– and that promise soon became reality. With the completion of the 800-mile Trans-Alaska Pipeline System (TAPS) from Prudhoe Bay to Valdez, AK, in 1977, ANS production took off like a rocket and by 1988 it exceeded 2 MMb/d. Not only did Alaska account for one-quarter of total U.S. crude oil output that year, it also briefly knocked Texas off its perch as the #1 oil-producing state.

Alaskan oil didn’t give the U.S. “energy independence” -– a rallying cry in the Ford, Carter and Reagan years –– but it helped. The physical characteristics of the North Slope’s medium sour-ish crude, with a 31.5 API gravity and about 1% sulfur (generally the cutoff we use to differentiate sweet and sour crude), were (and are) a plus. West Coast refineries were configured to run it, and the crude was — and is — very marketable in Asia too.

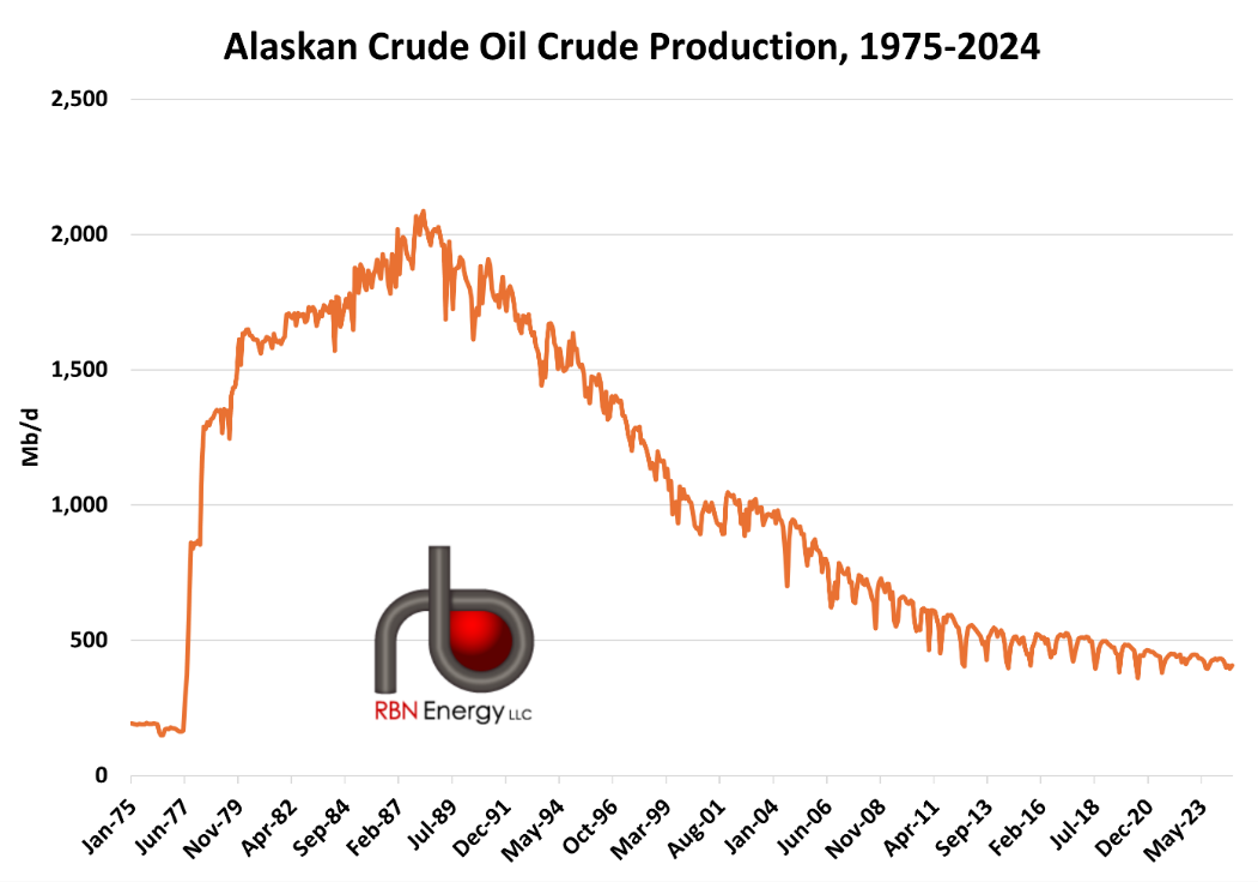

Figure 1. Alaskan Crude Oil Production, 1975-2024. Source: EIA

However, as shown in Figure 1 above, the picture quickly turned gloomy. Alaskan oil production peaked in 1988 and has headed downhill ever since as additional rounds of investments for new production ceased to materialize (see A Change Is Gonna Come). By 1995, Alaskan crude production had fallen to less than 1.5 MMb/d, and by 2000 it was down to less than 1 MMb/d. The slide didn’t end there. By the 2010s, production was hovering around 500 Mb/d, and in September 2024 (the most recent EIA stats available) it stood at about 408 Mb/d — or only 3% of total U.S. output (down from a peak of around 25% in 1988), which in August was at 13.4 MMb/d (right end of orange line in Figure 2 below). The issue isn’t that Alaska is running out of oil — far from it, as significant reserves still exist under the frozen tundra on the North Slope. However, Alaska’s energy industry has been thwarted by federal policies (most of the reserves were located on federally controlled land) as well as competition from shale producers in the Lower 48 who were largely unhindered by similar restrictions.

About the song

“Holding Out for a Hero” was written by Jim Steinman and Dean Pitchford. It appears as the fourth song on Footloose: Original Soundtrack of the Paramount Motion Picture and as the eighth song on Bonnie Tyler’s sixth studio album, Secret Dreams and Forbidden Fire. A music video for the song, directed by Doug Dowdle and featuring Tyler at the Grand Canyon, was released to promote the film Footloose. The song was released as a single off her album in January 1984 and went to #34 on the Billboard Hot 100 Singles chart. It’s been used in multiple movies, television shows and commercials. Personnel on the record were: Bonnie Tyler (lead vocals), Jim Steinman, Sterling Smith, John Philip Shenale (keyboards, synthesizer, programming), Art Wood (Simmons and Linn drums), and Hiram Bullock (guitar).

Secret Dreams and Forbidden Fire was recorded between 1983 to 1986 and produced by Jim Steinman, Roy Bittan, Larry Fast, John Jansen and John Rollo. Released in April 1986, it went to #106 on the Billboard 200 Album chart. Five singles were released from the LP, two of which had been released previously. The album, Footloose: Original Soundtrack of the Paramount Motion Picture, was released in January 1984 and went to #1 on the Billboard 200 Albums chart and has been certified Diamond by the Recording Industry Association of America. Seven singles were released from the LP.

Bonnie Tyler (Gaynor Sullivan) is a Welsh singer known for her husky vocal stylings. She started singing professionally in 1969. She signed a record deal with RCA Records in 1975 and released her debut single in 1976 and her debut album in 1977. She has released 18 studio albums, three live albums, 14 compilation albums, four EPs and 83 singles. She has sold more than 100 million records worldwide. In 2022, she was appointed an MBE for services to music. She continues to record and tour.

Comments

There have been decades of property tax litigation between the owners of TAPS and the various boroughs/Valdez beginning in 2006 or so. The parties were billions apart in their perception of value, with one of the main areas of dispute centering on end-of-life estimates. New oil fields and increased oil volumes and reserves will lend more stability to the tax base.