When it finally came online in mid-2017, the Dakota Access Pipeline was a lifesaver for Bakken crude oil producers. For years, they had suffered from takeaway-capacity shortfalls that forced many shippers to rely on higher-cost crude-by-rail, sapping producer profits in the process. Then came DAPL, which provides straight-shot pipeline access to a key Midwest oil hub, and its sister pipe — the Energy Transfer Crude Oil Pipeline (ETCOP) — which takes crude from there to the Gulf Coast. Problem solved, right? Not exactly. Now, there’s at least an outside chance that a shutdown order is issued as soon as early April in connection with the ongoing federal district court process, with the timeline for a physical closure of the pipe still to be determined. A shutdown may last for only a few months but could potentially last much longer. Where does this uncertainty leave Bakken producers, many of whom have been hoping to benefit from the recent run-up in crude oil prices by ramping up their output this spring? Today, we discuss recent upstream and midstream developments in the U.S.’s second-largest shale/tight-oil play.

The title of the blog we posted in the weeks leading up to the Dakota Access Pipeline’s commercial start-up three-plus years ago said it all: What a Difference a DAPL Makes. As we noted then, the Bakken was one of the earliest — and biggest — successes of the Shale Era. Forecasters routinely underestimated how quickly crude oil production in western North Dakota would grow. For one thing, many failed to appreciate the ability of producers to increase their drilling and completion efficiencies; for another, it was remarkable how rapidly the midstream sector responded to the Bakken’s serious (and growing) pipeline takeaway shortfalls in the first half of the 2010s by building more than 20 terminals where oil could be loaded into rail tank cars for delivery via existing rail networks. In Slow Train Coming, our 2016 Drill Down Report on crude-by-rail, we discussed the fact that railroads by late 2014 were transporting more than two-thirds of the 1.2-MMb/d of oil then being produced in North Dakota, and that while incremental new pipeline capacity came online in 2015-16, DAPL would be the real game-changer. When the new pipe started up, crude-by-rail volumes plummeted to less than 150 Mb/d, mostly to serve refinery customers on the East and West coasts.

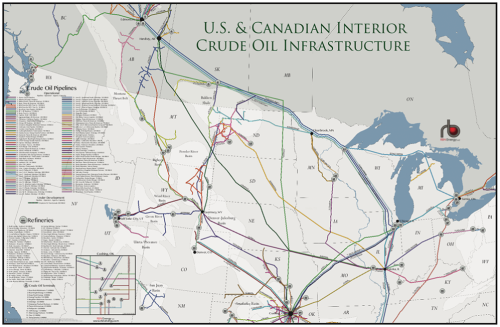

RBN's US & Canadian Interior Crude Oil Infrastructure Map features pipelines, refineries, and terminals that are new, existing, and under development from Canada to the Bakken Shale to Cushing.

Initially built to transport up to 470 Mb/d and most recently increased to a capacity of 570 Mb/d (with an expansion to approximately 750 Mb/d being planned), the 1,172-mile, mostly 30-inch-diameter pipeline begins with a hairpin turn through the core of the Bakken production area then makes a bee-line to the crude oil hub in Patoka, IL. There, most of the oil is either distributed to refineries in the Midwest or sent south to Nederland, TX, on the 744-mile ETCOP, which also started up in mid-2017. The two pipes, collectively known as the Bakken Pipeline System, are co-owned by Energy Transfer (with a ~36% share), Enbridge (~28%), Phillips 66 Partners (25%), MPLX (~9%), and ExxonMobil (~2%).

About the song

"Don't Wanna Lose You" was written by Gloria Estefan, and appears as the seventh song on Estefan's debut solo album, Cuts Both Ways. Released as a single in June 1989, the song went to #1 on the Billboard Hot 100 Singles chart and the Hot Latin Songs Singles chart. It has been certified Gold by the Recording Industry Association of America (RIAA). Personnel on the record were: Gloria Estefan (lead, backing vocals), Randy Barlow, Teddy Mulet (trumpet, backing vocals), Jorge Casas (bass, programming, backing vocals), Mike Scaglione (sax), Olay Ostwald (keyboards, programming); John DeFaria, Paco Fonta, and Michael Thompson (guitar); Robert Rodriguez (drums), Rafael Padilla (percussion), Emilio Estefan Jr. (congas), Paquito Hechavarria (piano), and John Slick (programming).

Cuts Both Ways was Estefan's final record made with the backing of Miami Sound Machine, whom she had been the lead singer with for a decade. It was her first album where she was featured as a solo artist. Recorded at Criteria Studios in Miami in 1988-89, it was produced by Emilio Estefan Jr., Jorge Casas, and Clay Ostwald. Released in July 1989, the LP went to #8 on the Billboard Top 200 Albums chart. It has been certified 3X Platinum by the RIAA. Five singles were released from the album.

Gloria Estefan is a Cuban-American singer, songwriter, actress, and businesswoman. She was the lead vocalist for the Miami Sound Machine from 1977 to 1989. As a solo artist, she has released 14 studio albums, 14 compilation albums, four EPs, and 49 singles, and has sold more than 75 million records worldwide. Estefan has won three Grammy Awards, a Lifetime Achievement Award from the American Music Awards, an MTV Video Music Award, a BMI Songwriter of the Year Award, and multiple Billboard Awards. She has received Kennedy Center Honors and the Presidential Medal of Freedom, and is a member of the Songwriters Hall of Fame. Estefan is also the owner of several successful restaurants in Florida. She continues to record and wants to do a final tour in Latin America when touring can safely resume.