Brent physical traders are members of an exclusive club that transacts roughly fifty 600 MBbl cargoes of crude a month representing about 1 MMb/d of production. ICE Brent futures traded an average of 500 MMb/d during 2012. These two markets are linked together by the ICE Brent Index that allows for cash settlement of futures. Today we explain the Brent futures delivery mechanism.

This is part 2 in our series on the physical Brent crude market. What follows will make more sense if you read part 1 first. In that first episode (see Crazy Little Crude Called Brent – The physical Trading Market) we explain that the Brent crude used as a benchmark for international pricing and that underlies the ICE Brent futures contract – is made up of crude oil produced in dozens of different North Sea fields and delivered to market in four different streams – Brent, Forties, Oseberg and Ekofisk (BFOE). Multiple crudes are included in the Brent stream definition because the original Brent crude production is almost played out. That meant the number of cargoes that could be traded in the Brent physical market was constrained meaning that the price setting process was subject to manipulation. We described the forward physical price setting process that involves 600 MBbl parcels of crude selling for delivery in future months and the way those parcels become “dated” when their loading dates are notified to buyers. In this episode we explain the linkage between the Brent physical market and the Brent ICE futures contract.

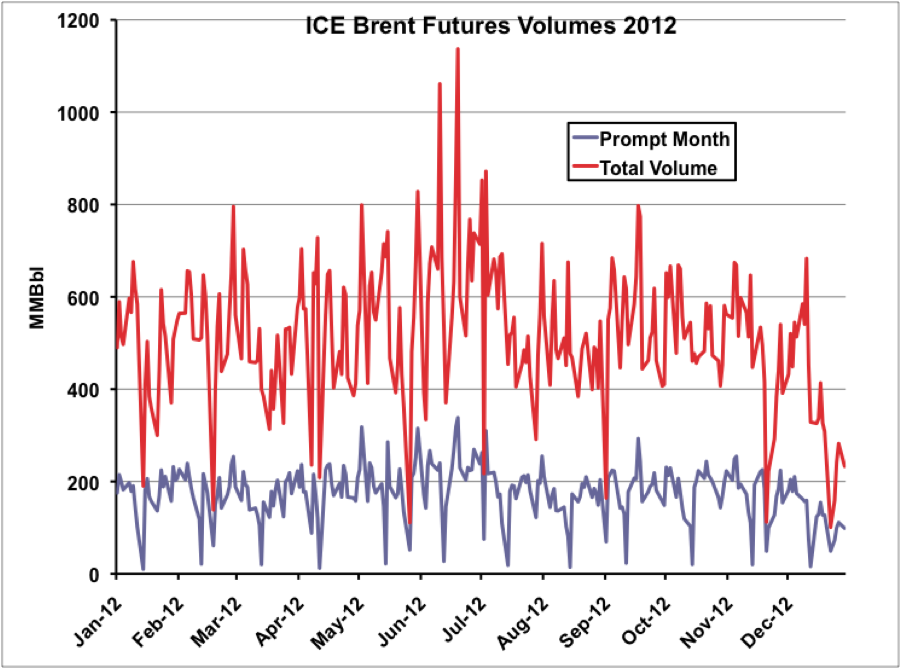

Intercontinental Exchange (ICE) Brent futures are traded in 1000 Bbl contracts. The size of the ICE contract therefore differs markedly from the physical Brent market where cargo parcels are 600 MBbl. Having a smaller futures contract reduces the cost of entry into the futures market – since buying 600 MBbl of crude costs upward of $60 MM at today’s prices. The 1000 Bbl futures contract is a more manageable $100 M. A smaller contract size also makes the futures market more accessible and increases the volume of transactions, thus liquidity. The chart below shows the 2012 volume of ICE transactions for prompt month and total futures. The total volume of 500 MMb/d dwarfs the smaller 1 MMb/d physical market by a factor of 500X.

Source: ICE Futures Data from Morningstar

We have previously discussed the way that futures markets facilitate the transfer of price risk between participants (see Henry the Hub I Am I Am Part II). One of the key concepts that make a futures market successful is convergence. This is the process that links the futures market to the underlying physical commodity and it is usually accomplished by a delivery mechanism. Delivery allows futures market participants holding open buy or sell positions after the contract they own ceases trading on the futures exchange (expires), to exchange their futures contract for the underlying physical commodity. Provided that this exchange occurs at contract expiration then futures and physical prices should converge at that point. In other words the futures contract is worth the same as the physical commodity.

In the case of Brent futures, the delivery mechanism and the convergence process are complicated because it is not practical to deliver 1000 Bbl lots of Brent crude oil. As we have learned – the physical market operates using larger parcels of 600 MBbl. To overcome this complication the Brent ICE futures contract is “cash” settled against an index price. That means that participants with outstanding contracts when trading expires are able to exchange their futures contracts for cash based on a calculated index price. The Brent Index is calculated by the ICE futures exchange using assessments for market prices in the Brent forward market. This is the Brent physical market that we described in the first part of this series (see Crazy Little Crude Called Brent – The physical Trading Market).

The Brent Index is an average of the following elements:

1. A weighted average of first month (meaning next calendar month) cargo trades in the 25-day BFOE market.

2. A weighted average of second month (meaning two calendar months out) cargo trades in the 25-day BFOE market plus a straight average of spread trades between the first and second months. [Although it doesn’t sound like it, this second element of the Index is a first month “implied” price because it is the second month assessment plus (or minus) the spread between second and first month prices. This element allows the exchange to include spread assessments in the calculation.]

3. The midpoint average of designated assessments published by price reporting services (e.g. Platts, Argus, etc.).

The elements used to “converge” the ICE Brent futures contract with the physical market are therefore prices for crude to be delivered in the next calendar month in the BFOE 25-day market. It is important to understand that although only a very small percentage of futures contracts are actually cashed out against the Brent Index, the $/Bbl price of the Index needs to be as close as possible to what a participant would have had to pay if they purchased a physical cargo in order to fulfill the convergence requirement. To this end ICE use first forward month assessments in the index because that is the first available crude for purchase that could be physically delivered during the expiring futures contract delivery period.

One anomaly that currently exists in the ICE Brent futures market is that contracts expire on the last business day prior to the 15th of each calendar month (allowing 15 days to arrange delivery) but they really should expire on the 5th of the month. Here is why. Since the ICE contract was created in 1988 the physical trading market has evolved to increase the number of trading days in the forward market (the notice period before cargoes become “dated”) from 15 days to 25 days. We described in Part 1 how Brent physical market participants increased the quantity of crude by adding new grades – this more recent extension of the notice period from 15 to 25 days did the same thing by adding 10 day’s worth of physical cargoes to the trading market – another mechanism to increase liquidity. That extension of the notice period has yet to be incorporated into the Brent futures contract despite ICE’s best efforts.

ICE tried to bring Brent futures into line with the 25 day BFOE market by listing a new “Brent NX” futures contract that expires on the last business day prior to the 5th of each calendar month (allowing 25 days to arrange delivery). In December 2011 ICE listed a complete set of Brent NX (25-day) futures contracts that has traded in parallel to the original ICE Brent (15-day) ever since. ICE futures participants are apparently unwilling to bring themselves to make the transition to the new contracts and so far they have attained little or no volume. To be fair the process of weaning traders off a popular and liquid futures contract to “try something new” is not for the faint hearted. The first company to move over would have limited counterparties and volume and therefore be assuming unnecessary risk. It remains to be seen what happens to Brent NX contracts. In the meantime the ICE expiration calendar is an imperfect replica of the physical market.

Whether or not the Brent Index cash settlement process is a perfect example of convergence (it is not) the mechanism does contain an important market linkage between ICE Brent futures and physical Brent trading. That linkage can also be described as an exchange for physical (EFP) mechanism. An EFP mechanism is a tool commonly used in futures markets to allow participants to link their physical and futures markets transactions together conveniently. The Brent Index is an EFP mechanism because it allows futures participants holding ICE Brent contracts at expiry to exchange those contracts for a cash value equivalent to physical barrels. Although the Brent Index EFP mechanism only comes into play once a month after contract expiration - kind of an infrequent link - many other types of EFP transactions do occur on the ICE. We won’t get into how these additional EFPs work here (another blog topic) but their active use implies a strong relationship between futures and physical markets.

From this point the discussion of further links between Brent physical and futures markets becomes more complex because it involves the use of derivative markets to hedge differences between the prices of ICE futures, 25 day BFOE and dated Brent. We will head there in a future episode in this series. In our next installment we will return to the physical Brent market to explain why participants are currently engaged in heated discussion about how to handle quality differences between the four BFOE streams that are traded.

Comments

The total designing of cash settlements for future is a bit complicated procedure and includes several important clauses that must be carefully selected in order to avoid future contingencies.

sale of structured settlement