The bitter, eight-year battle to control CITGO Petroleum’s three U.S. refineries could soon be coming to an end. A Delaware court has recommended a $7.38 billion bid from Dalinar Energy Corp., the U.S. subsidiary of Canadian miner Gold Reserve Ltd. There’s opposition, but a final decision could be just weeks away. In today’s RBN blog, we’ll discuss what a resolution would mean for the three refineries, which have a combined capacity of more than 800 Mb/d.

Let’s start with some background. As we detailed in I’ll Be Around, there’s been a primarily below-the-radar battle playing out in the U.S. District Court for the District of Delaware since 2017 about how best to help satisfy the claims of a dozen-plus creditors who collectively lost more than $20 billion when the government of Venezuela — the de facto owner of CITGO Petroleum and its parent company, PDV Holding (PDVH) — defaulted on its bonds. (In 2019, control of CITGO was transferred away from the ruling Maduro regime in Venezuela to the opposition “shadow” government, then led by Juan Guaidó.) In May 2021, U.S. District Court Judge Leonard P. Stark appointed Robert B. Pincus as a special master tasked with devising a plan to sell PDVH/CITGO. After a two-round bidding process that concluded in June 2024, Pincus recommended on September 27, 2024, that the district court approve Amber Energy and its $7.3 billion bid for CITGO and its three refineries (Lake Charles, LA; Lemont, IL; and Corpus Christi, TX). However, instead of ending the drama, the court restarted the bidding from scratch in December 2024, citing issues with the auction process.

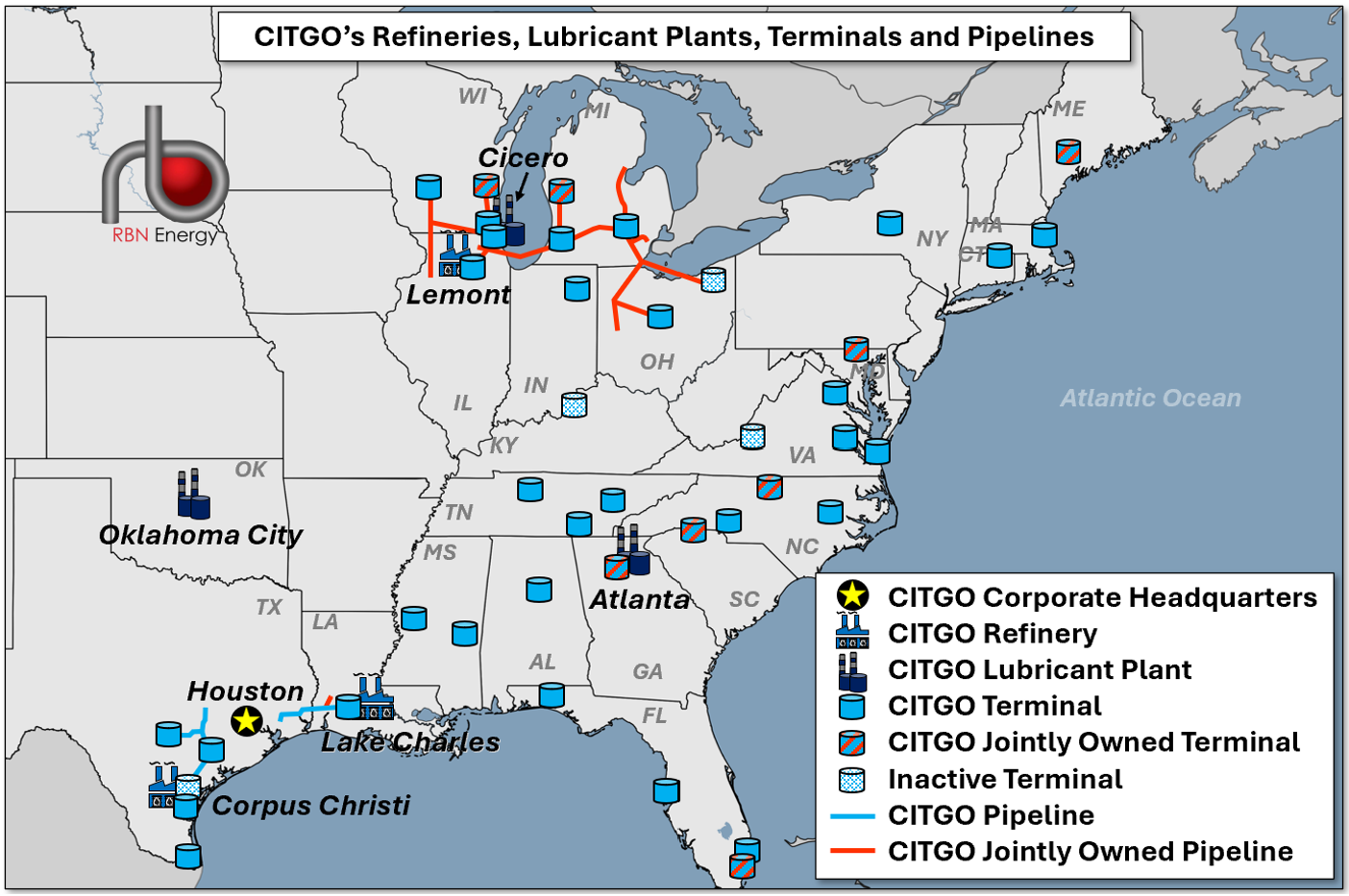

Figure 1. CITGO’s Refineries, Lubricant Plants, Terminals and Pipelines. Source: CITGO

The winner of the auction will get three impressive U.S. refineries (dark-blue refinery icons in Figure 1 above) in addition to a number of lubricant plants, terminals and pipelines. While we predict there will be refineries shutting their doors in the coming years, we expect all three of the CITGO refineries to be survivors over the next two decades. We also see them benefiting from a variety of market factors we expect to develop, including a modest widening heavy/light crude differential from the record tightness seen so far this year, strong middle distillate margins, and continuing demand for U.S. products in key export markets.

About the song

“Changes” is one of the best-known songs by Britain’s own David Bowie and is ranked #128 on Rolling Stone magazine’s list of “The 500 Greatest Songs of All Time.” “Changes” was a track on Bowie’s fourth studio album, Hunky Dory, which was released in late 1971. Hunky Dory was produced by Ken Scott and Bowie and is the first album to feature players that would end up being the legendary Spiders from Mars band that recorded Bowie’s next LP, The Rise and Fall of Ziggy Stardust and the Spiders from Mars.

The “Changes” track features Bowie on vocals and saxophone, future Yes band member Rick Wakeman on keyboards, and string arrangements by guitarist Mick Ronson. The song is an autobiographical tale describing Bowie-s often chameleon-like career, with its many changes of direction in style and substance. Ironically, the song never cracked the U.S. Top 40 upon its release in January 1972, topping out at #66. Later, the song became an iconic Bowie tune — always a crowd favorite at live concerts, and featured in movies and TV shows.

David Bowie (David Robert Jones) was an English singer, songwriter, musician and actor. He is considered an iconic figure in popular music in the 20th century. Raised in London, he got his professional start in his teens with the King Bees, who released one single, “Liza Jane,” in 1964. He signed with Mercury Records in 1969 and released “Space Oddity,” which became a top-five hit in the UK. He has released 27 studio albums, 27 compilation albums, 22 live albums, eight EPs, three soundtrack albums and 128 singles. He has sold more than 100 million records worldwide. He won six Grammy Awards, four Brit Awards, an Ivor Novello Award and a Saturn Award, and is a member of the Rock and Roll Hall of Fame and the Songwriters Hall of Fame. He starred in seven motion pictures and had a featured role in two others. Bowie died in New York City in January 2016 at the age of 69.