For many years now, the U.S. has been buying — and piping or railing in — virtually all of the crude oil Canada has been exporting, in part because Canadian producers have only very limited access to coastal ports. More recently, greater pipeline access from the Alberta oil sands to the U.S. Gulf Coast (USGC) has created an attractive pathway — a “Carefree Highway,” if you will — for Canadian crude oil to be “re-exported” to overseas customers. This year, much stronger international demand has sent re-export volumes to record highs — and provided Alberta producers very attractive price differentials for their oil sands crude. That overseas demand appears to be sustainable, but with the looming startup of the 590-Mb/d Trans Mountain Expansion Project (TMX), which will increase the capacity of the Trans Mountain Pipeline system to 890 Mb/d and enable much more Alberta crude to be exported from docks in British Columbia, the re-export surge from the USGC may be in for a pullback, as we discuss in today’s RBN blog.

It looks like Canada’s crude oil exports are finally showing off their stuff and stepping out on the town. For a couple of decades, the U.S. has been the overwhelmingly dominant buyer of Canada’s crude oil exports, funneling millions of barrels per day into Midwest refineries and, in recent years, sending more down to refineries in the Gulf Coast region. In the past couple of years — and most especially this year — this near-exclusive export relationship has finally begun to diversify from the standpoint of Canadian producers, who have been finding other customers in increasing quantities in overseas markets.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

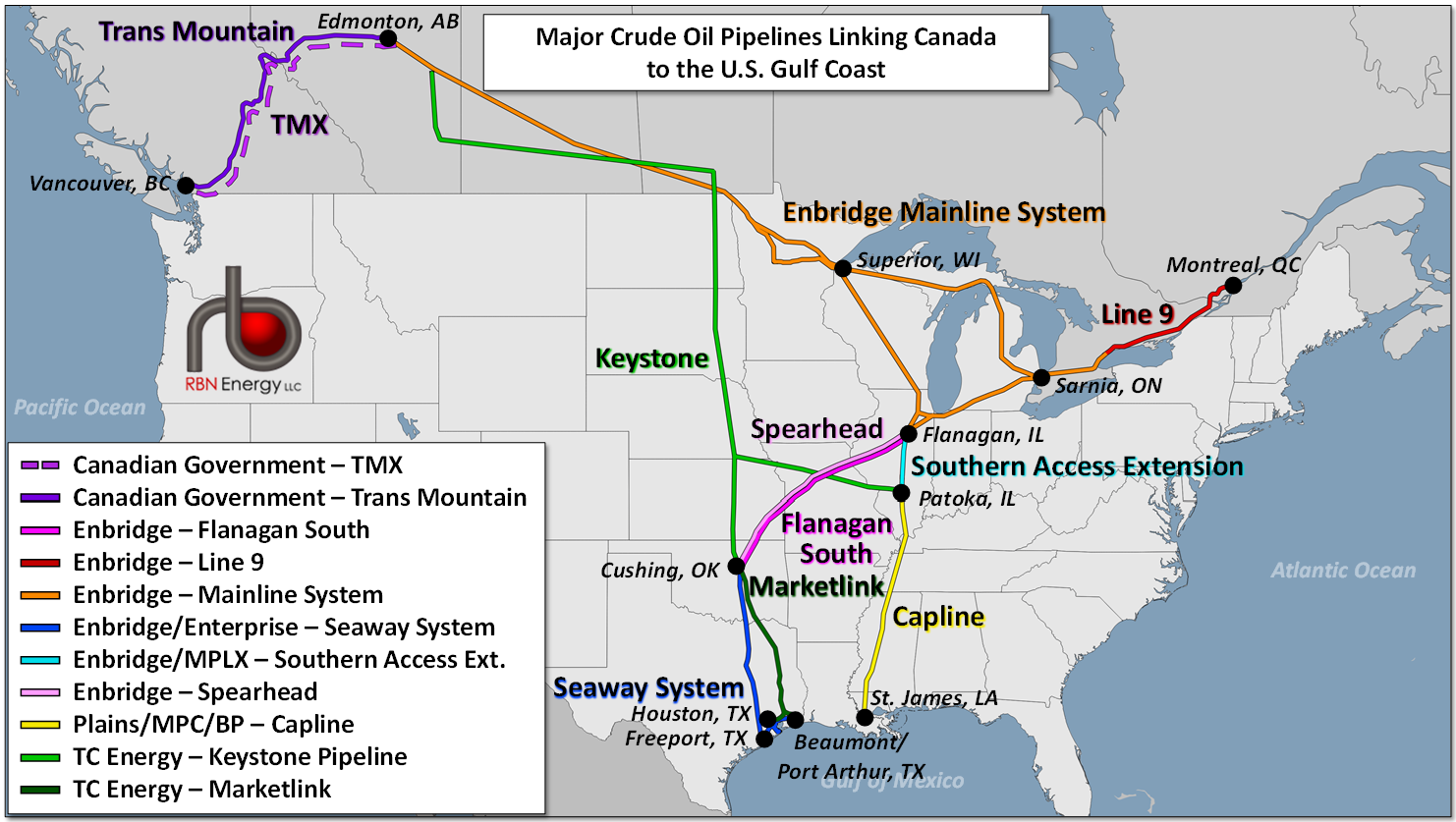

Although Canada since the late 1950s has been exporting very small amounts of crude oil to countries other than the U.S. from the Westridge Terminal just outside of Vancouver, BC, and began to export more from Canada’s East Coast when offshore production there began to ramp up in the 1990s, those export volumes have generally remained very modest — under 100 Mb/d. In addition, expanding these exports has been usually handcuffed by either severely constrained export capacity at Westridge or by production declines on the East Coast. With the completion and startup of the TMX project (dashed purple line in Figure 1) slated for early 2024, export capacity from Canada’s West Coast will be increased considerably, perhaps by as much as 500 Mb/d.

But we’re getting ahead of ourselves. Canadian crude oil exports — or, more accurately, crude oil re-exports because they are exported from Canada to the U.S. and then exported again from the U.S. to other countries — have been finding their way to overseas customers in increasing quantities the past few years and have surged this year thanks to two factors that have nicely aligned. First, the expansion of previously constrained pipeline access from Canada to the U.S. has resolved, for now at least, the problem of pipeline apportionment, where too much crude supply was competing for too little crude pipeline capacity, creating lower pricing conditions in Canada for its flagship heavy crude oil, while constraining the amount of crude reaching the Midwest and Gulf Coast. With the completion of the Enbridge Mainline Line 3 Replacement Project in 2021 (orange lines in Figure 1), and additional access via Enbridge’s Spearhead, Flanagan South, and Seaway pipelines (light pink, dark pink and blue lines, respectively), combined with TC Energy’s Keystone Pipeline (light green line) and Marketlink Pipeline (dark green line), as well as the reversal of the Capline Pipeline (yellow line) from Patoka, IL, to St. James, LA, Canadian crude now has wide-open pipeline access from the Alberta oil sands of northeast Alberta all the way to the export docks along the USGC. Put simply, pipeline capacity limitations appear to be a thing of the past, allowing still-increasing production of oil sands crude to reach customers along the Gulf Coast and, now, across the rest of the world.

Figure 1. Major Crude Oil Pipelines Linking Canada to the U.S. Gulf Coast. Source RBN

About the song

“Carefree Highway” was written by Gordon Lightfoot and appears as the third song on side two of Lightfoot’s ninth studio album, Sundown. Released as the second single from the album in August 1974, it went to #1 on the Easy Listening chart and #10 on the Hot 100 Billboard Singles chart. Lightfoot said the song title came to him first as he was driving along Arizona State Route 74 in Phoenix. Personnel on the record were: Gordon Lightfoot (lead, backing vocals, six- and 12-string acoustic guitar), Terry Clements (acoustic guitar), Rick Haynes (bass), Jim Gordon (drums), and Nick DeCaro (orchestration).

Sundown was recorded in November 1973 at Eastern Sound Studios in Toronto, with Lenny Waronker producing. Released in January 1974, it went to #1 on the Billboard 200 Albums chart. Two Top 10 singles were released from the LP.

Gordon Lightfoot was a Canadian singer-songwriter and guitarist who achieved success in folk, folk-rock, and country music. Besides his own catalog of hit records, his songs have been covered by many other successful artists. Lightfoot released 20 studio albums, three live albums, 19 compilation albums and 47 singles. He received 16 Juno Awards and is a member of the Canadian Music Hall of Fame and Canadian Country Music Hall of Fame. Bob Dylan has said, “I can't think of any Gordon Lightfoot song I don't like. Every time I hear a song of his, I wish it would last forever.” Lightfoot passed away in May 2023 in Toronto at the age of 84.