A dramatic increase in crude-by-rail shipments over the past two years as well as surging lease rates for hard to come by tank cars encouraged an 18 month backlog of new orders – even while crude shipments only represent a small fraction of total rail carloads. Changes in the crude price differentials that encouraged the growth of crude by rail have reduced both the demand for tank cars and lease rates. Today we present analysis from PLG Consulting that shows rail tank car oversupply is quite possible - barring a few "wild cards".

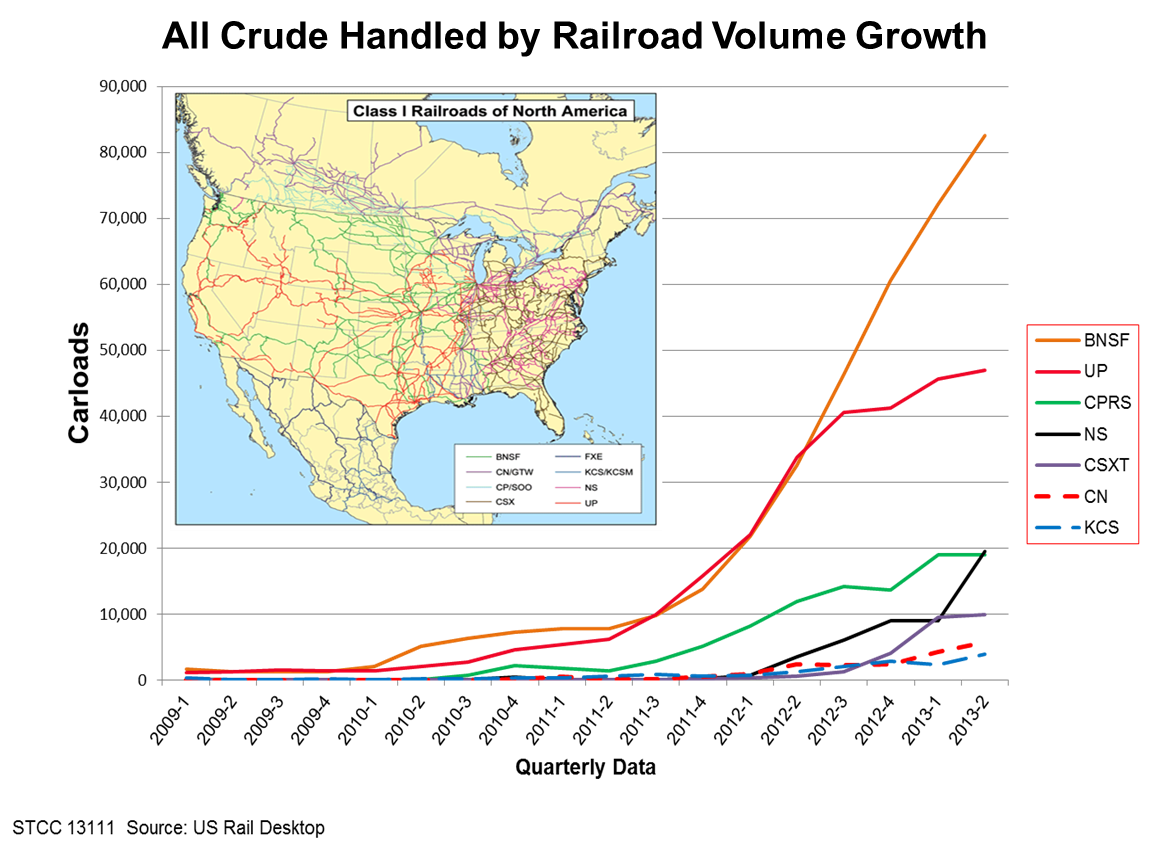

The surge in tank car orders over the past couple years is specifically attributable to the dramatic increase in movements of crude-by-rail (CBR). As demonstrated in the graph below, CBR shipments were almost non-existent on the Class I railroads as recently as late 2009, but have increased exponentially in subsequent years. Short-term (~one year) lease rates for tank cars went from around $400/month in 2010 to over $3,000/month in late 2012 and early 2013 in some cases. The railcar tank builders couldn’t supply the extra demand coming from crude by rail. The high lease rates that crude shippers were willing to pay took a significant amount of tank cars from ethanol service as they could be quickly transitioned to light/sweet crude oil without modifications.

Source: US Rail Desktop

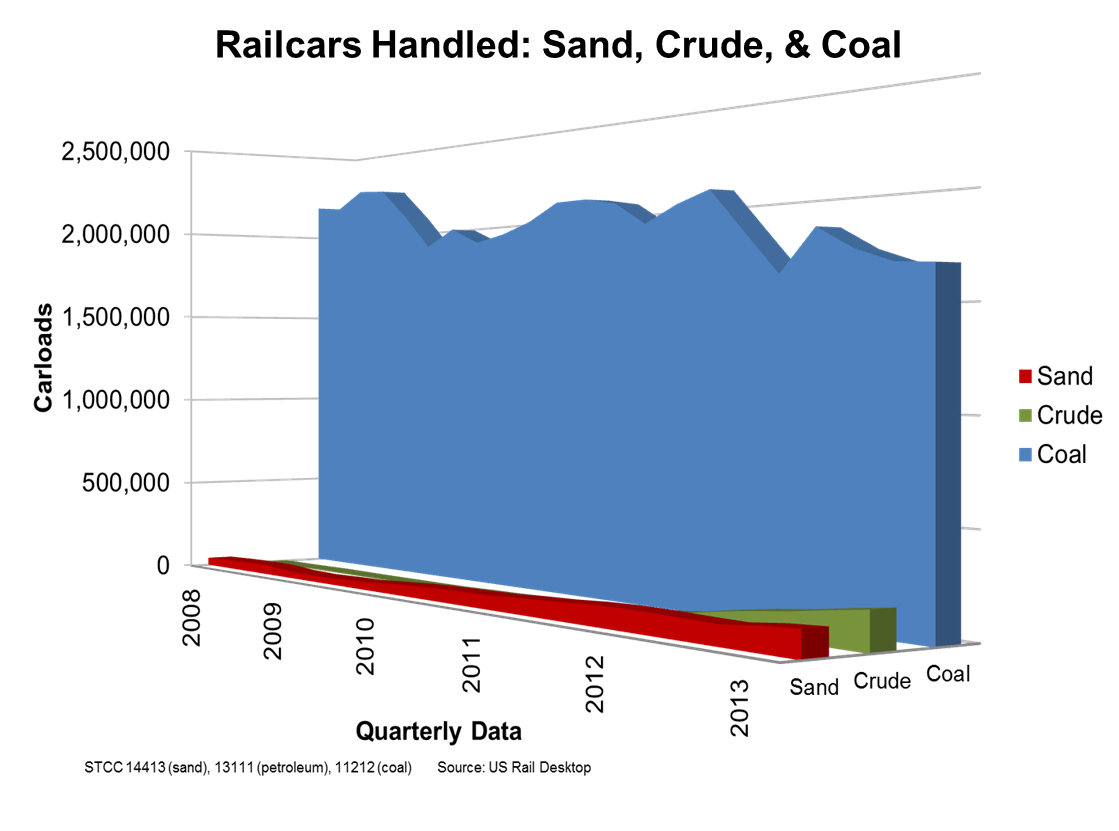

The amazing growth in oil (and gas) production due to hydraulic fracturing has been one of the major business stories of the past few years, but it’s worth noting that the overall rail volumes from both inbound frac sand and outbound CBR are still small when compared with rail volumes for coal (see graph below). So CBR receives it’s attention because it is a growth area both for the tank car manufacturers and for the railroads, but in the big picture, it is only approximately 1 - 2% of the rail car market and approximately 2 - 3% of the current rail traffic (including intermodal).

Source: US Rail Desktop

The major tank car builders in North America are Greenbrier Companies, American Railcar Industries, Inc., Union Tank Car and Trinity. The major tank car leasing companies in North America include Union Tank Car, GATX, Trinity, CIT Leasing and GE Railcar. The business of both manufacturing and leasing tank cars has been particularly attractive over the last few years not only because of the crude-by-rail phenomenon, but also the growth of agricultural, chemical, and refining sectors. These industries can expect continued growth as new manufacturing capacity that takes advantage of abundant, low-cost fuels and feedstocks comes on-line. However, for CBR in particular there are several nuances to this tank car market that may cause some turbulence going forward.

General-Purpose vs. Coiled/Insulated

The differences between the two widely used CBR tank car designs are worth further discussion. The higher volume tank car is the general-purpose non-coiled non-insulated car with nominal capacities of 30,000 gallons (GP30) and 31,800 gallons (GP31.8) used for light/sweet crude that is produced in the US shale oil plays. The GP31.8 is a crude optimized car that started being manufactured in 2011. These general-purpose non-coiled non-insulated cars have a lower tare (empty) weight, a higher usable capacity (up to 286,000 lbs. gross-weight-on-rail), and cost less to manufacture. A GP31.8 car has an ability to haul about 720 Bbl of light crude oil, while a GP30 with a 263,000 lb. gross weight is able to haul about 675 Bbl of light crude oil. GP31.8 cars currently cost about $130,000 - $135,000 new with short-term lease rates at about $1,350 - $1,700 per month. GP30 cars currently have a short-term lease of $1,000 - $1,350 per month.

The heavier Canadian Oil Sands type crude requires a more complex coiled and insulated railcar because the commodity is more viscous and needs to be heated to help it flow (see Heat It). The coils and insulation decrease a tank car’s usable capacity and make it both heavier and more expensive to build. The optimized “heavy crude” style car has a nominal capacity of 28,800 gallons and ability to haul about 600 Bbl of heavy crude oil. This type of railcar currently costs about $140,000 new with short-term lease rates at about $1,200 - $1,600 per month. Another tank car used to haul heavy crude oil is the 263,000 lb. gross weight coiled and insulated tank car with a nominal capacity of 25,500 gallons and a realistic payload of about 550 Bbl of heavy crude oil. These cars currently have short-term lease rates at about $1,100 - $1,400 per month. The recent increase in interest and announcements about moving heavy crude from the Canadian Oil Sands by rail has increased the demand for coiled and insulated tank cars.

Railcar leasing companies must give serious consideration to which type of tank car to be built because they are committing to own an asset with a 40 or 50 year life expectancy in a tank car market with increased uncertainty due to the volatile price and demand swings in the CBR world. In general, the leasing community will prefer to own the smaller cars with coils and insulation because they have far more flexibility across numerous commodities (chemicals, etc.), whereas the larger GP cars are more limited in scope (with ethanol, methanol and some refinery chemicals being the only sizeable alternative markets to crude).

About the song

“You've Got Another Thing Comin’” was written by Rob Halford, K.K. Downing and Glenn Tipton and appears as the second song on side two of Judas Priest’s eighth studio album, Screaming for Vengeance. Released as a single in August 1982, it went to #67 on the Billboard Hot 100 Singles chart, making it the only Judas Priest single to make it into the Hot 100 to date. Singer Rob Halford said the single was “a song of hope about rising above the difficulties that come your way.” Personnel on the record were: Rob Halford (vocals), Glenn Tipton (lead guitar), K.K. Downing (rhythm guitar), Ian Hill (bass), and Dave Holland (drums).

Screaming for Vengeance was recorded between January and May 1982 at Ibiza Sound Studios in Ibiza, Spain, and Beejay Studios in Orlando, FL. Produced by Tom Allom, the album was released in July 1982. It went to #17 on the Billboard 200 Albums chart and has been certified 2x Platinum by the Recording Industry Association of America. Two singles were released from the LP.

Judas Priest is an English heavy metal band formed in Birmingham in 1969. The group has sold over 50 million records worldwide and is considered an iconic heavy metal band. The synchronized guitar player moves that every hair metal band has copied over the years originated with Judas Priest. They have released 18 studio albums, six live albums, seven compilation albums, and 29 singles. They have won one Grammy Award and received an Award for Musical Excellence from the Rock and Roll Hall of Fame in 2022. Twenty members have passed through the band since its inception. The current lineup of Judas Priest — Rob Halford on vocals, Ian Hill on bass, Richie Faulkner and Andy Sneap on guitars, and Scott Travis on drums — continues to record and tour.