As U.S. crude oil expands its foothold across the world, the markets that trade it have undergone some fundamental changes. Since the onset of the pandemic almost four years ago, these changes have included the shortening of the loading-date range for crude oil cargoes marketed along the U.S. Gulf Coast. Price reporting agencies (PRAs) like Argus have responded, launching crude oil assessments that reflect a narrower loading window. In today’s RBN blog, we take a closer look at the changes and the new assessments Argus has rolled out to help crude oil traders manage their market exposure.

Before we discuss Argus’s initiatives, let’s recap some of what was happening in the oil markets during the early days of COVID-19. In early spring of 2020, Russia and Saudi Arabia were locked in a price war that resulted in the Saudis shipping out massive quantities to customers globally. Around the same time, market participants were taking stock of the bleak demand outlook from the widespread pandemic lockdowns. It was a perfect storm for the market — a supply glut plus softening consumption — that sent benchmark oil prices plunging, including the infamous brief trip for NYMEX crude oil futures into negative territory (see Crazy). Short of shutting in production, storing unsold oil became the best option for producers, who had no clear indication of when governments would remove COVID restrictions that would resuscitate demand.

Canadian crude output is rising, requiring new export routes. As traditional pathways face constraints, the U.S. Rockies—especially the Guernsey, WY hub—are emerging as key corridors for moving Canadian heavy crude to downstream markets, including the Gulf Coast.

The bearish balances manifested in the oil futures market structure, reflecting a trend called contango where prices for immediate supply were cheaper than those in the forward months. As prompt oil prices weakened drastically, showing just how oversupplied the market really was, superlatives like super-contango and hyper-contango started to get thrown around. The last time we had witnessed a contango structure of that magnitude on the NYMEX oil complex was in 2008-09, when the Great Recession undermined consumer demand. As a result, E&Ps shut in hundreds of crude-producing wells (see Shut Down).

However, by the second half of 2020, the Saudis and Russians had ended their price spat and the OPEC+ group had agreed to major production cuts. Combined, these changes started to trim the fat off supply. Then toward the end of that fateful year, COVID vaccine developments had advanced enough that widespread inoculations were being planned in the new year. That raised hopes that an economic turnaround was in sight, paving the way for a recovery in demand. All in, these factors set off a rebound in crude prices, with some pondering a future with $100/bbl oil (see What a Fool Believes).

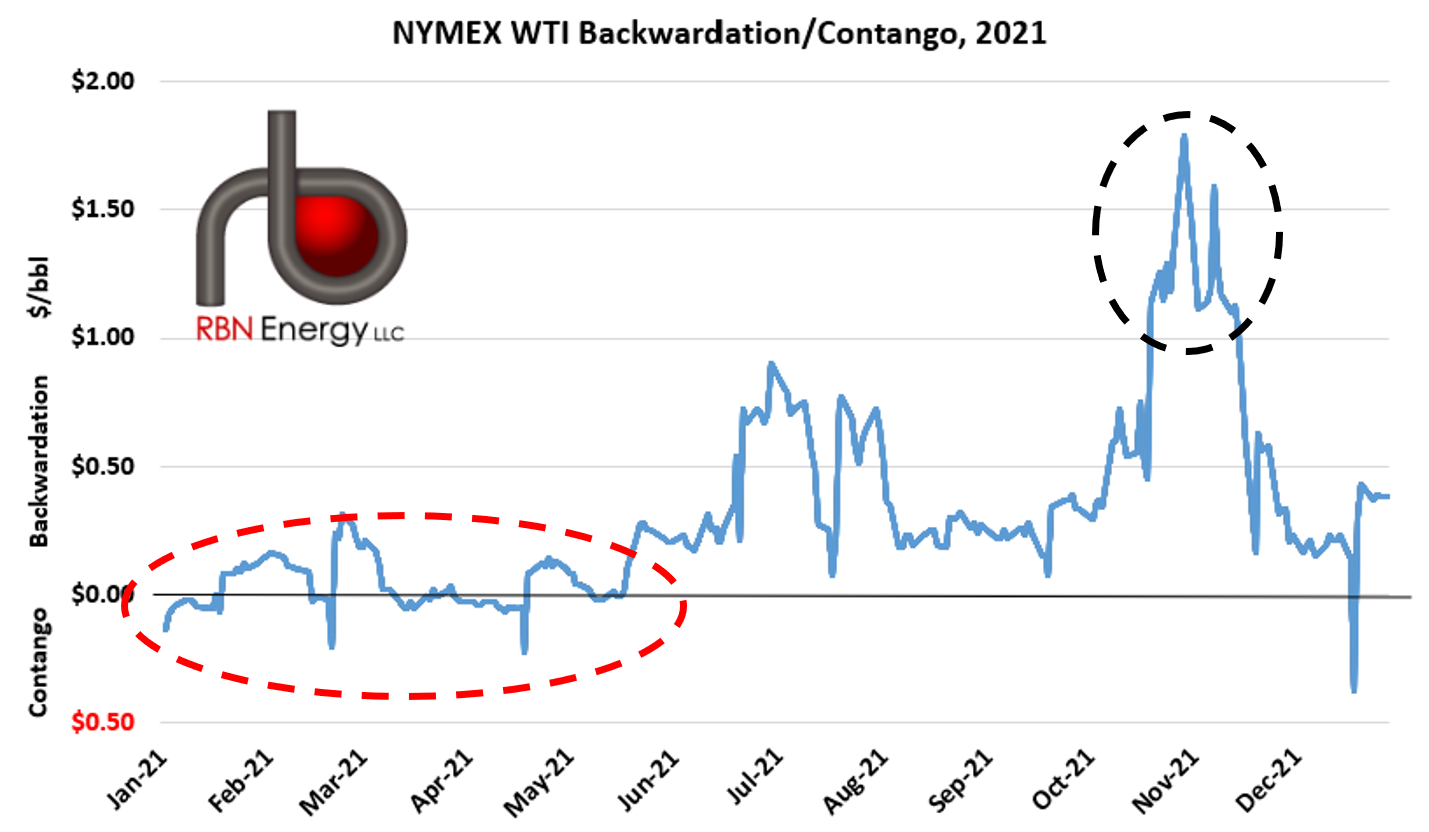

In 2021, the U.S. oil futures market structure slipped into backwardation — the opposite of contango — where near-term supply was getting priced above forward delivery. (Figure 1 below shows the difference between the prompt-month and second-month NYMEX WTI contracts.) Initially, the NYMEX crude oil curve kept flip-flopping between the two market structures (dashed red oval), but then backwardation latched on firmly from May, reaching a high of $1.79/bbl (dashed black oval) at the end of October. With the expanding backwardation, the market was telling us that while short-term fundamentals had strengthened, there was still apprehension about potential future COVID aftershocks or the impact from a push to speed up the energy transition.

Figure 1. NYMEX WTI Backwardation/Contango, 2021. Source: Bloomberg

About the song

“Call and Answer” was written by Steven Page and Stephen Duffy and appears as the seventh song on Barenaked Ladies’ fourth studio album, Stunt. Released as the third single from the LP in July 1999, it went to #17 on the Billboard Adult Top 40 Singles chart. Personnel on the record were: Steven Page (lead vocals), Ed Robertson (guitars, backing vocals), Jim Creeggan (bass, cello, backing vocals), Kevin Hearn (keyboards, backing vocals), and Tyler Stewart (drums, percussion, backing vocals).

Stunt was recorded at Arlyn in Austin and Phase One in Scarborough, ON, in early 1998. Produced by Barenaked Ladies, David Leonard and Susan Rogers, the album was released in July 1998 and went to #3 on the Billboard 200 Albums chart. It has been certified 4x Platinum by the Recording Industry Association of America. Five singles were released from the LP.

Barenaked Ladies is a Canadian rock band formed in Scarborough, ON, in 1988. The band became well-known for writing songs with a dry sense of humor and became more popular after writing the theme song for the hit sitcom The Big Bang Theory. They have released 14 studio albums, three live albums, four compilation albums, four EPs, and 41 singles. They have won two Billboard Music Awards and one World Music Award. Six members have passed through the band since its formation. Andy Creeggan left the band in 1995 and Steven Page left in 2009. The band continues to record and tour and will begin a tour of the UK beginning in April.