With the electric power sector in many other states turning to natural gas-fired generation to replace retired coal and nuclear capacity, gas interests were understandably optimistic the same would happen in California when the plan to retire the 2,200-MW San Onofre Nuclear Generating Station (SONGS) was announced in June. But California’s aggressive efforts to promote renewable energy and combined heat and power (CHP), improve energy efficiency, and reduce greenhouse gas emissions make it likely utilities and independent power companies there will use less natural gas going forward—not more. Today in the second part of our of series on California gas demand we examine why gas use by large-scale power plants in the Golden State is likely to decline, why CHP-related gas use by commercial and industrial firms will rise, and why the state’s gas pipeline infrastructure may need beefing up.

In Part 1, we looked at the decision by Southern California Edison and SONGS’s other co-owners to retire the station’s two nuclear units, and at California’s various pro-environment policies and how, taken together, they essentially undo the possibility of a one-for-one replacement of the retired nuclear capacity with new gas-fired power. What it comes down to is this: California envisions an energy future with more renewable energy, more energy-efficient homes and businesses, and limited use of gas-fired capacity by the state’s utilities and independent power companies. Gas surely will maintain a major role in California’s electric sector; after all, with nuclear power on the wane and solar and wind power variable in their output, gas-fired capacity is the one go-to source for power that’s available at the flip of a switch. (California years ago essentially banned coal-fired power; only 200 MW of it is currently operating there.) But with the state’s 33%-by-2020 renewables mandate and its greenhouse gas-reduction and energy-efficiency goals, solar power in particular will take center stage, with gas-fired power serving largely as a supplemental source during the day and the primary source only at night.

As we noted in Part 1, California regulators and the state’s grid operator have reached a consensus on what they think is the best way to deal with the loss of SONGS, the need to retire about 3,800 MW of older gas-fired units in southern California with ‘once-through’, less efficiient cooling, and the likelihood that another 1,200 MW of older gas-fired capacity will be retired as well. Their plan (details of which must still be worked out) would have about half of the incremental power needs in the region (or about 3,250 MW) come from a mix of renewables, CHP, energy efficiency, energy storage, and demand response (under which some electricity consumers agree—for a price--to cut their use when power supplies are short). The rest of the needs would come from enhancements to the transmission system and the development of about 3,000 MW of new, conventional generating capacity, all of it presumably gas-fired. With the 5,000 MW of older gas-fired capacity expected to be retired, that’s a net loss of 2,000 MW of plants fired by gas by 2020 or so.

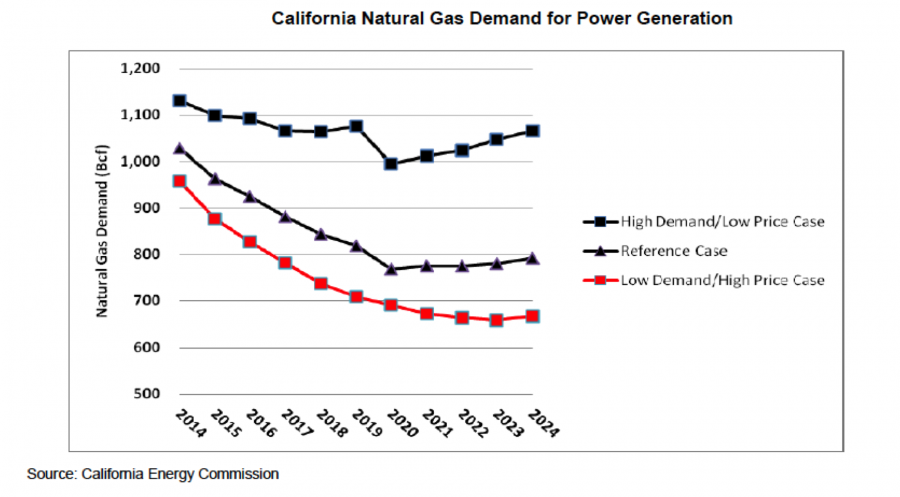

The increasing role of renewables in California also is changing how the state’s gas-fired plants are being used. As of January 2013, more than 12,000 MW of renewable capacity was in operation in California, about 3,000 MW of it solar and the rest a mix of wind farms, biomass-fired plants and geothermal facilities. Regulators expect another 8,000 MW of utility-scale solar capacity and 5,000 MW of non-utility, rooftop solar capacity to be added by 2020. That flood of solar capacity could provide as much as half of California’s power needs on a mild spring day, and as much as a third on a hot summer day, leaving gas-fired plants, hydroelectric plants, the Diablo Canyon Nuclear Station (the state’s only remaining nuclear facility), and power imports from other states and Mexico to provide the rest. So, what’s happening more and more, year by year, is solar and other renewables are squeezing out gas-fired power, and holding down the need for natural gas to fuel utility-scale power plants. The California Energy Commission (CEC), which oversees both the electric and gas sectors, sees gas consumption by these larger plants declining under every scenario—that is, no matter the levels of gas demand or price (see Figure 1). The reference case sees annual demand for gas slipping from more then 1,000 Bcf in 2014 to less than 800 Bcf in 2020, with essentially flat usage levels after that.

Figure 1 (Click to Enlarge)

It’s worth noting that there is a big difference between projected gas demand for utility-scale power plants in California’s electric sector and for the rest of the western U.S. California is part of the Western Electricity Coordinating Council (WECC) region (which also includes 13 other states, plus British Columbia, Alberta and Mexico’s Baja California). In most of the WECC states there is less emphasis on renewables, energy efficiency and greenhouse gas reduction, and—more important—there is a lot of coal-fired capacity being retired and replaced by new gas-fired plants. As a result, power-sector gas demand in WECC is likely to rise, particularly in the 2020s, even with the deflating effect of California (see Figure 2). The CEC reference case sees WECC gas demand rising by about 400 Bcf over the next 10 years—from about 1,800 Bcf in 2014 to 2,200 Bcd in 2024.

Join Backstage Pass to Read Full Article