PADD 1 — the East Coast — represents about 31% of total U.S. consumption of refined products (and 37% of its population) but is home to just 5% of U.S. refinery capacity. With only minimal in-region crude oil production, PADD 1 refineries are almost entirely dependent on imported and domestic inflows of both crude oil and products like gasoline, diesel and jet fuel. In the early years of the Shale Era, large volumes of domestic crude were railed or barged to these refineries, but in recent years they’ve again become largely reliant on imports from OPEC, Canada and other foreign sources. In today’s RBN blog, we’ll look into PADD 1’s changing crude oil and refined products supply and demand balance.

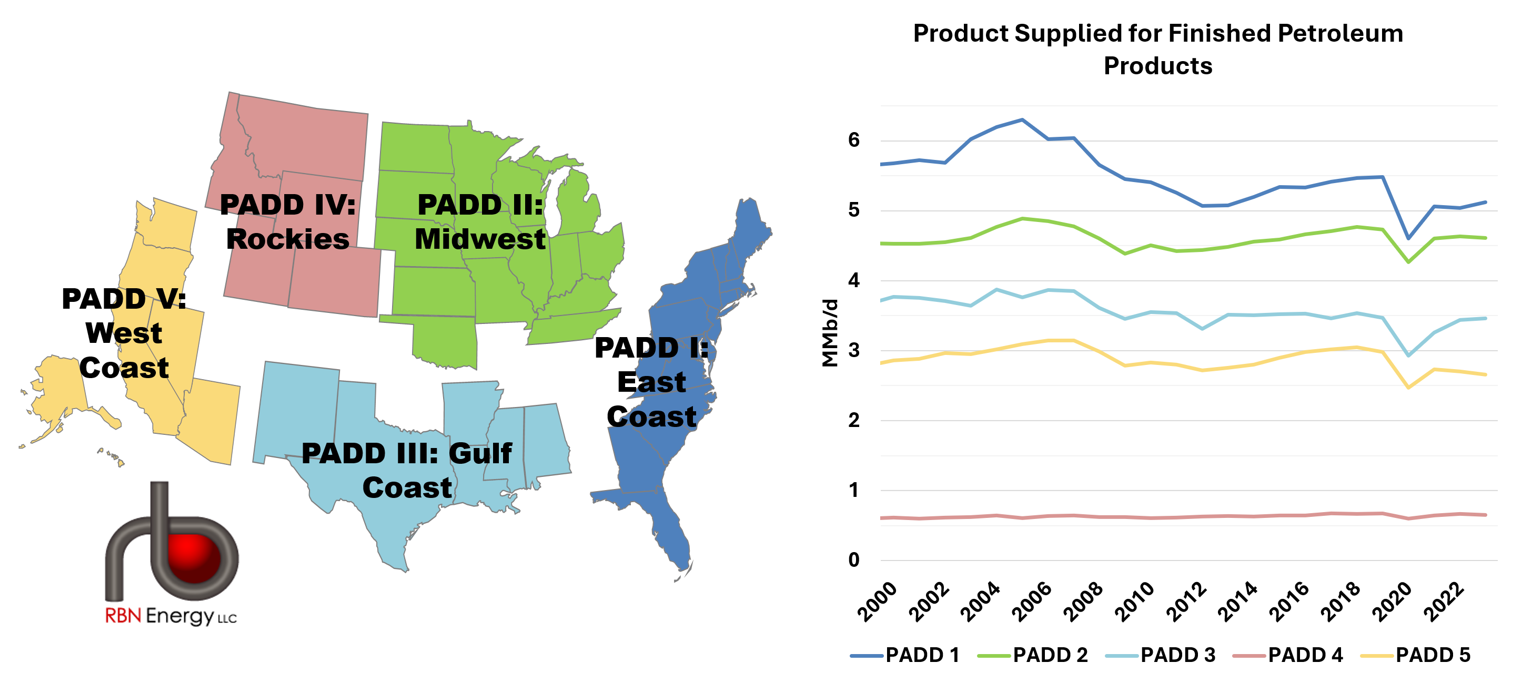

Figure 1. U.S. PADD Map and Product Supplied for Finished Petroleum Products by PADD. Source EIA

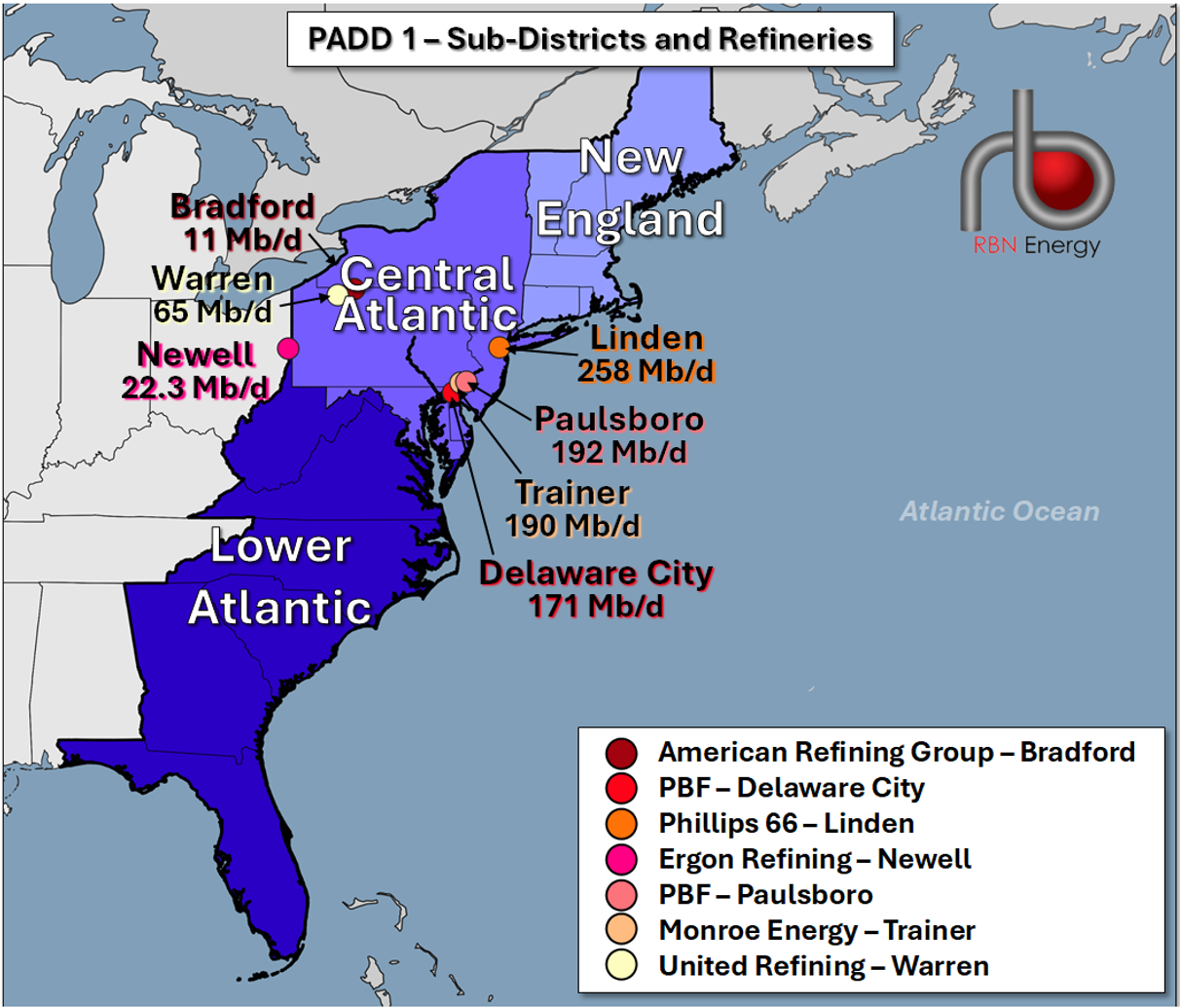

The U.S.’s Atlantic Coast, stretching from picture-perfect coastal towns in Maine to the tropical Florida Keys, is the home of New York City’s iconic skyline, Philadelphia’s historic landmarks, and Atlanta’s vibrant nightlife — and more than 125 million people, almost all of them relying on refined products for many aspects of their lives. The East Coast also represents the first of five Petroleum Administration for Defense Districts (PADDs; colored regions in Figure 1). Created in World War II to manage the country’s refined product demand, PADDs now serve the purpose of regionalizing data. PADD 1 (blue region in map on left side of Figure 1 above) is further divided into three regional groupings: PADD 1-A (New England; light-blue area in Figure 2 below), PADD 1-B (Central Atlantic; medium-blue area), and PADD 1-C (Lower Atlantic; dark-blue area).

Figure 2. Map of PADD 1 Sub-Districts and Refineries. Source: RBN

With PADD 1’s population density, it should come as no surprise that the region is the largest consumer of refined products. As shown in the chart on the ride side of Figure 1, demand for petroleum products (blue line) refined from crude oil (primarily gasoline, diesel and jet fuel, and excluding biofuels) has diminished somewhat, from an annual average of 6.3 MMb/d in 2005 to 5.1 MMb/d in 2024. That being said, the PADD’s regional refinery capacity has also been dwindling, which has led to its continued reliance on imported gasoline and diesel, as well as increasing amounts of refined products being piped in from PADD 3 (Gulf Coast) — up by roughly 500 Mb/d since 2010. As those inflows, transported on Colonial Pipeline and Kinder Morgan’s PPL (formerly known as Plantation), have become increasingly important in meeting the region’s needs, it has heightened the risk should a disruption affect either. And we’ve seen that happen in the past, such as the ransomware attack on Colonial (see On The Dark Side) in 2021 or the gasoline leak in Georgia just two weeks ago. (However, as we’ll get to in a moment, flows on those pipelines may decrease significantly as regional demand declines post-2030.)

About the song

“Bring the Noise” was written by “Chuck D” Ridenhour, Eric “Vietnam” Sadler and Hank Shocklee and appears as the second song on side silver of Public Enemy’s second studio album, It Takes a Nation of Millions to Hold Us Back. The song first appeared on the soundtrack of the 1987 film Less Than Zero and was released as a single in February 1988. It went to #56 on the Billboard Hot R&B/Hip-Hop Singles chart. Produced by the Bomb Squad, it features a mix of samples, drum machines, scratching, sirens, sound effects, and industrial noise. Personnel on the record were: Chuck D, Flavor Flav, Harry Allen, Fab 5 Freddy, Erica Johnson, Professor Griff (vocals), Johnny Juice Rosado, Terminator X (turntables), and the Bomb Squad (production, programming, sampling, mixing). New York City thrash metal band Anthrax did a version of the song with Chuck D that was released as a single and appeared as the second song on Anthrax’s compilation album, Attack of the Killer B’s, which was released in June 1991. It also appears as the fourth song on side four of Public Enemy’s fourth studio album, Apocalypse 91 ... the Enemy Strikes Back, released in October 1991. One can’t help but wonder if this collaboration inspired Ice T to form Body Count and influenced the proliferation of rap/metal bands in the 1990s.

It Takes a Nation of Millions to Hold Us Back was recorded in 1987-88 at Chung King House of Metal, Greene Street Recording in New York City, Sabella in Roslyn, and Spectrum City in Hempstead. Produced by Chuck D, Hank Shocklee, Rick Rubin, and the Bomb Squad, the album was released in June 1988 and went to #1 on the Billboard Top R&B/Hip-Hop and #42 on the Billboard 200 Albums charts. It has been certified Platinum by the Recording Industry Association of America. Five singles were released from the LP.

Public Enemy is an American hip-hop group formed by Chuck D and Flavor Flav in Roosevelt, NY, in 1985. Their highly charged political hip-hop struck a chord with fans of the genre, resulting in Gold and Platinum records and an induction into the Rock and Roll Hall of Fame and a Grammy Lifetime Achievement Award. They have released 15 studio albums, two live albums, one soundtrack album, four compilation albums, and 41 singles; 23 members have passed through the group since its formation, with Chuck D and Flavor Flav always on board. The group’s last studio album was What You Gonna Do When the Grid Goes Down? released in September 2020. Chuck D released a four-part documentary on PBS, Fight the Power: How Hip-Hop Changed the World, in 2023. Flavor Flav has appeared in several television shows and VH1 reality TV series.