To everything there is a season. And this spring is the season for plant turnarounds in the NGL industry. Fractionators will be offline. Petrochemical plants will be down. And NGL market prices, already buffeted by huge production increases from the shale phenomenon will feel the brunt of the outages.

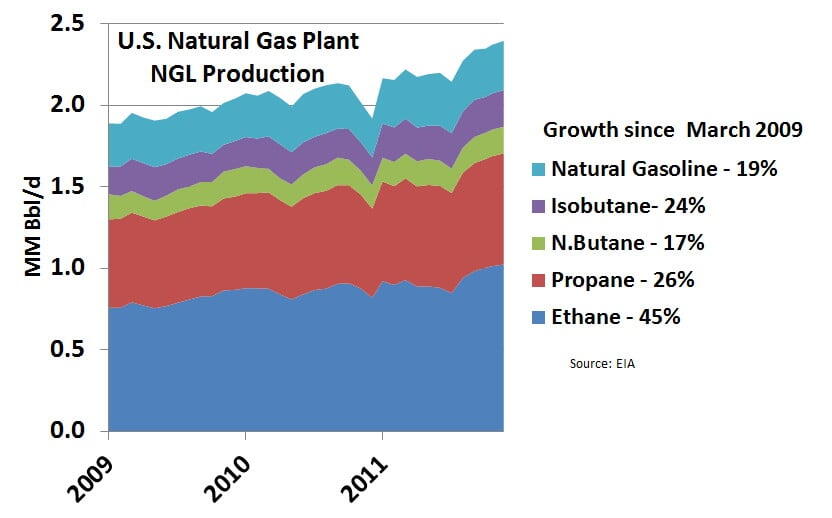

NGL production is on a tear. Check out the growth rates for natural gas plant production over the past 3 years based on EIA numbers in the graph below. Natural gasoline – 19%. Isobutane – 24%. Normal butane – 17%. Propane – 26%. And of course, ethane – 45%. NGL production is approaching 2.5 MMb/d. Ethane alone broke the 1.0 MMb/d ceiling in December. With the emphasis by producers on wet gas and crude oil (with wet associated gas) these growth rates show no sign of slowing down anytime soon.

Although NGL prices as a whole are lower relative to crude oil (due primarily to increases in supply), prices are within 7-8% of last year – well above historical levels. The market seems relatively balanced. Ethane is being chewed up by ethylene crackers at historically high rates. Excess propane supplies due to production and lack of demand (no weather, like natural gas) are being shipped to Latin America. (see The Long Way Around: Propane from shale gas gets to the Far East). Natural gasoline is moving up Capline for use as Canadian tar sands diluent. Normal butane is being isomerized into isobutane, and isobutane is moving into refinery alkylation. All is well in the NGL markets, right? Possibly not.

A time to break down, and a time to build up. Plant turnaround season approacheth. The turn-arounds will hit NGLs from two angles. The first is fractionation capacity. Raw mix (a.k.a., Y-grade, or mixed NGLs) must be split into the five purity product NGLs in a fractionator. There are almost 70 of these things scattered around the country. But the big, important ones are mostly located along the Gulf Coast, specifically in and around Mt. Belvieu, Texas – center of the NGL universe. Capacity of the five major Mt. Belvieu fractionators is about 900 Mb/d. Two of these fractionators, Oneok’s MB-1 (160/Mb/d) and GCF (Gulf Coast Fractionators, 100Mb/d, owned by Targa, Devon, and ConocoPhillips) are scheduled for turnaround in Q2. So capacity in an oversupplied market will be cut by almost 30%. At the same time, ONEOK’s Bushton, KS fractionator will be down for a few days.

A time to get, and a time to lose. Two things will happen. #1 – raw mix will get backed up to the processing plants supplying these fractionators, likely resulting in some ethane rejection or other cutbacks. #2 – purity products will be in short supply, likely pushing prices higher. Depending on the timing of these turnarounds, it is quite possible that offtakes will be cut enough to result in shortages of NGLs deliverable into key markets. Marketers caught short can do weird things to prices.

A time to rend, and a time to sew. There’s more. A number of petrochemical facilities – the largest single market for NGLs – are also going on turnaround. These include LyondellBassell/Equistar Channelview, INEOS Chocolate Bayou, BASF/FINA Port Arthur, and ChevronPhillips Sweeny. These turnarounds will cut demand for ethane and a few other NGLs, putting downward pressure on prices.

What are the odds that the fractionator turnarounds will sync up with the petchem turnarounds? Tiny.

What are the chances that NGL prices will bounce between over and under supply on a daily basis? Not tiny.

What are the chances of unplanned plant shutdowns happening in the middle of all this? Almost guaranteed.

A time of war, and a time of peace. What if an Israeli strike against Iran happens in the midst of all of this? I don’t even want to think about it.

To Everything There Is a Season, and this spring is the season of volatility for NGLs. Spring is 14 days away. Fasten your seatbelts and place your tray tables in their upright, locked position.

Comments

Consensus expectations seem to be that ethane prices will move back up when crackers come back on line. So why is the ethane forward curve in backwardation? Or am I mistaken?