The economics of natural gas production in the dry Marcellus, the wet Marcellus and the Utica are so favorable—and the shale gas resource so bountiful—that the only real limit on how much the Marcellus/Utica plays can produce is the capacity of the pipeline network in the Northeast and neighboring regions to take gas to market. And there’s the rub, because the region’s gas transmission infrastructure was designed decades ago to deliver large volumes of gas to the Northeast, not away from it. That’s why the midstream sector has made “a new plan, Stan,” and is now in the midst of a major reworking of the pipeline system—not just within and near the Marcellus/Utica but just about everywhere east of the Mississippi. The $30 billion re-plumbing effort and its effects on the gas market as a whole are the subject of RBN’s latest Drill-Down Report, “50 Ways to Leave The Marcellus” which is available today to Backstage Pass members. In today’s blog, we provide an overview.

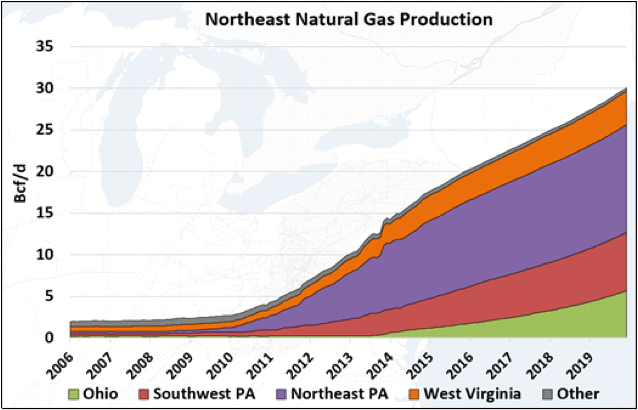

For decades, the US Northeast was a huge natural gas sponge, its residents, businesses and industry absorbing all the Gulf Coast, Midcontinent, Rockies and Canadian gas that pipelines into the region could deliver. In the past three years, however, gas production in the Northeast’s dry Marcellus, wet Marcellus and Utica has been growing by leaps and bounds. First, this burgeoning production started to displace inbound flows. Now Marcellus/Utica gas is pushing outward into neighboring areas like the Midwest and Ontario and, with total production in the region topping 18 Bcf/d and headed for 30 Bcf/d by 2019 (see Figure #1), the region has set its sights on still-bigger markets, including the Southeast and—the grand prize—the Gulf Coast itself, with what are expected to be dozens of gas-guzzling petrochemical facilities and liquefied natural gas export terminals.

Figure #1 – Northeast Natural Gas Production

The foundation for the projected growth in Northeast production is strong. Initial production rates and other factors suggest that the break-even gas price for dry Marcellus producers in northeastern Pennsylvania is somewhere around $2.50/MMBTU. The break-even price in the wet Marcellus in southwestern Pennsylvania and northern West Virginia—and in the NGL- and condensate-rich Utica in eastern Ohio—is even lower (about $2/MMBTU or below) because producers there bring in big bucks from the liquids side of their business; for them, revenue from gas is just gravy. But producer rates of return are only optimized if their gas (and their NGLs and condensate) can be delivered to market without constraints and without the basis penalties that come with pipeline congestion.

“The answer [to constrained Northeast gas] is easy if you take it logically,” as Paul Simon said (sort of), and involves adding new take-away capacity, lots of it. Relieving—and, in time, eliminating—the constraints Marcellus/Utica producers have been dealing with (and suffering financially from) is a primary aim of a dozen or more midstream companies that are now scrambling to rework their pipeline networks to reflect the Northeast’s fast-paced change-over from net consumer of gas to net supplier. This reworking involves a variety of projects, some to handle increasing flows within the Marcellus/Utica, others to add bi-directionality to what had been one-way trunklines to the Northeast, and still others to augment existing lines with needed incremental capacity. The problem for Marcellus/Utica producers—in the near-term at least—is that re-plumbing much of the gas pipeline network in the eastern US requires a lot of planning and coordination, and in most cases lots of regulatory approvals, all of which take time (as does project construction).

Understanding the production, demand and pricing drivers behind the effort to develop new take-away capacity out of the Marcellus/Utica is critical to assessing how the markets for gas out of the regions will develop through the rest of this decade and into the 2020s. In the new Drill-Down Report, RBN reviews the evolution of the gas market in the Northeast; the pace of gas production growth in the dry Marcellus and, more recently, the wet Marcellus and the Utica; and the market signals that showed the region’s pipeline constraints were worsening (and fast). After this discussion of basis differentials and their effect on pipeline development and production, the report gets into the meat of the matter, namely, the 50 to 60 pipeline projects affecting Marcellus/Utica, and—most important—the 41 of these projects that will actually add take-away capacity out of the production areas (and when that capacity will be added). The projects are grouped in five corridors (see Figure #2 below): Northeast to the New England market (purple), Northeast into Canada (blue), Midwest via Ohio (green), the Gulf Coast via Ohio (red), and the Southeast along the Atlantic Coast (orange).

About the song

“50 Ways to Leave Your Lover” was written by Paul Simon and appears as the fourth song on side one of his fourth solo studio album, Still Crazy After All These Years. Released as the second single from the album in December 1975, it reached #1 on the Billboard Hot 100 Singles chart and has been certified Gold by the Recording Industry Association of America (RIAA). The song started out as a humorous way to document Simon’s divorce from his first wife, Peggy Harper. He wanted the song to be centered around the drum beat to “avoid clutter.” He recorded the song in Phil Ramone’s small demo studio above Manny’s music store in midtown Manhattan. Drummer Steve Gadd’s military ghost beats on the snare and prominent kick drum help set up the song’s groove beautifully. That beat has been sampled on many popular hip-hop records over the years. Personnel on the record were: Paul Simon (lead vocals, acoustic guitar), Steve Gadd (drums), Kenny Ascher (keyboards), John Tropea, Hugh McCracken (electric guitar), Tony Levin (bass), Ralph McDonald (percussion), and Patti Austin, Valerie Simpson, Phoebe Snow (backing vocals).

Still Crazy After All These Years was recorded in early 1975 at A&R Recording in New York City and produced by Paul Simon and Phil Ramone. Released in October 1975, the album reached #1 on the Billboard Top 200 Albums chart. It has been certified Gold by the RIAA. Four U.S. Top 40 singles were released from the LP.

Paul Simon is an American singer-songwriter with a career spanning six decades. He began performing with his school classmate Art Garfunkel in 1956 under the name Tom & Jerry. After changing the act’s name to Simon & Garfunkel, they came to prominence in the 1960s with their close harmonies and catchy folk-rock songs. After the Simon & Garfunkel mega-hit album Bridge Over Troubled Water in 1970, the pair broke up, each going on to successful solo careers. Paul Simon released five studio albums, four live albums, 13 compilation albums, one EP, and 26 singles as a member of Simon & Garfunkel. As a solo artist, he has released 15 studio albums, four live albums, 11 compilation albums, and 61 singles. He has won two Brit Awards, 16 Grammy Awards, is the recipient of a Gershwin Prize, Polar Music Prize, and has been inducted into the Rock and Roll Hall of Fame twice, once as a member of Simon and Garfunkel, and once as a solo artist. Simon continues to write songs and record.