The Energy East pipeline project proposes to convert part of the TransCanada Mainline natural gas system and add new pipeline in eastern Canada to connect oil receipts in Alberta with refineries in Ontario, Quebec and on the Atlantic seaboard. The proposal competes with existing plans by Enbridge to feed eastern Canadian refineries with light crude but does offer the prospect of supplying heavy crude for export from Canada’s East Coast. Today in Part 2 of a series on the project we review destination markets.

In Part 1 of this series (see What Becomes of the Empty Pipelines?) we described TransCanada’s plans to convert part of their massive Mainline natural gas pipeline to oil. The Energy East Pipeline project would convert 1865 miles of existing natural gas pipeline and require construction of a further 870 miles of new pipeline to deliver oil from Hardisty Alberta and Saskatchewan as far East as St John, New Brunswick on the Eastern seaboard. If approved by Canadian regulators the pipeline will flow between 500 Mb/d and 850 Mb/d of heavy crude oil starting in 2017. The TransCanada open season on the project will end later this month on June 17, 2013.

If the Energy East pipeline gets built there should be no lack of crude production in Western Canada to be transported on it. Last year the Canadian Association of Petroleum Producers (CAPP) forecast Western Canadian oil sands production to rise from 1.6 MMb/d in 2011 to almost double at 3.1 MMb/d by 2020, 4.2 MMb/d by 2025 and 5.0 MMb/d by 2030 (see Production Stampede – Where Will Canadian Oil Production Go). Right now very little Western Canadian oil production reaches the Eastern seaboard where the majority of Canadians live. The TransCanada pipeline conversion offers the potential to feed refineries in this region from domestic production instead of imports. According to Statistics Canada, Eastern Canadian refineries consumed about 1.17 MMb/d of crude in 2012 of which 0.8 MMb/d was imported.

As we explained in the first episode of this series, Eastern Canadian refineries are largely configured to process light sweet crudes. So if the crude moving east on the proposed Energy East pipeline is destined to feed these refineries it will have to be light crude rather than heavy. There are supplies of light crude in Western Canada – Bentek estimate current light crude production in Saskatchewan at about 490 Mb/d growing to 600 Mb/d by the end of 2016. Much of this crude is produced from the Canadian part of the Williston Basin – aka the Bakken and it is currently being moved to market in the US either by rail or via the Enbridge Lakehead pipeline system into the Midwest.

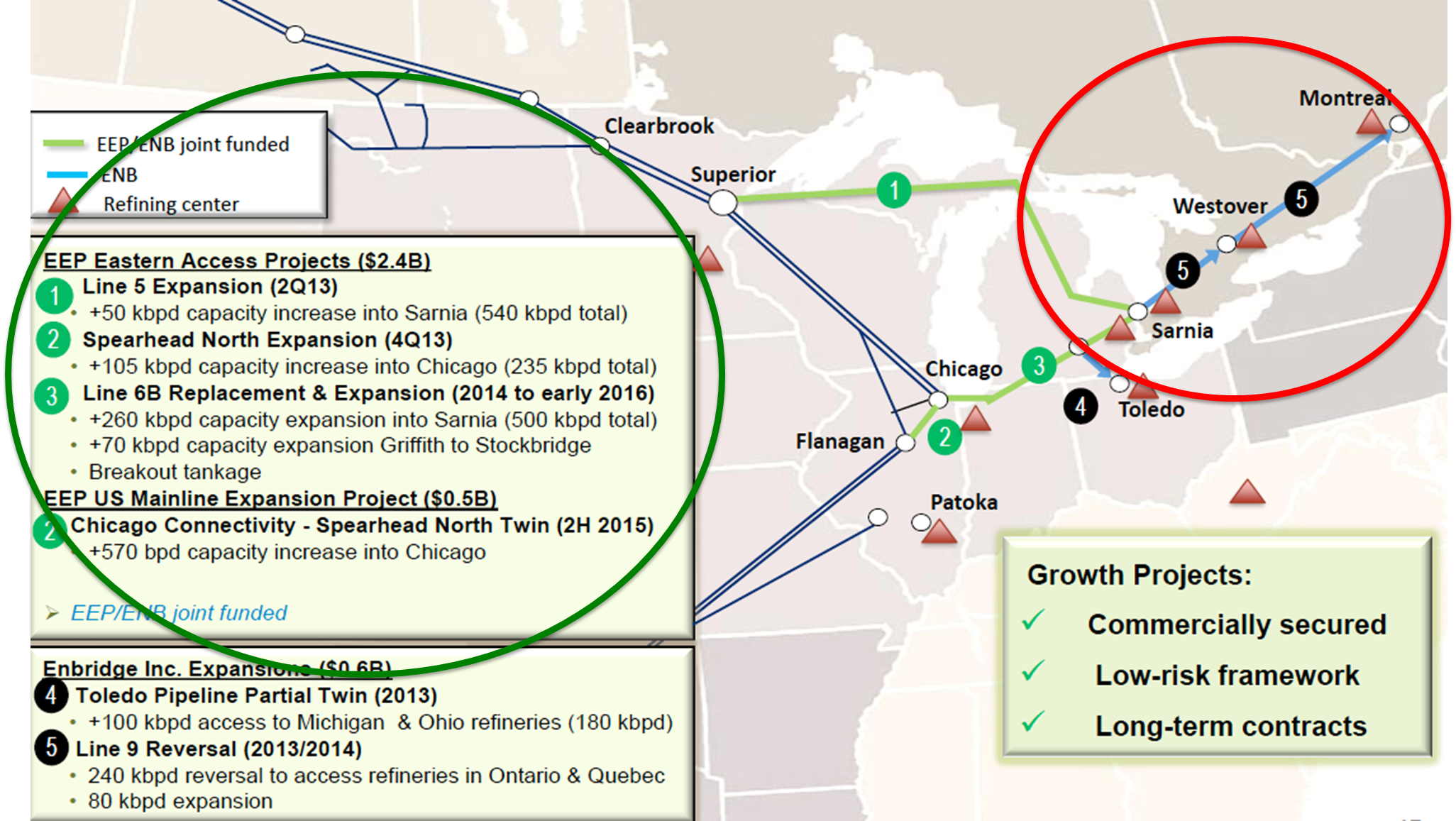

So if the TransCanada Energy East project is to attract light crude shippers it will have to compete head to head with the “incumbant” Enbridge Lakehead system. That competition will intensify at the end of 2013 when the Enbridge Line 9 reversal comes into service (see red circle on the map below). Enbridge Line 9 is a 240 Mb/d pipe that previously flowed crude oil westward from Montréal, Québec to Sarnia, Ontario. The first stage of the planned reversal of this pipeline will provide crude transport of Western Canada crude from Sarnia to Enbridge's North Westover Station in Ontario, and was approved by Canada’s National Energy Board (NEB) in July 2012. A second stage of the Line 9 reversal that would extend the pipeline from North Westover to Montreal and add an additional 80 Mb/d capacity has already secured shipper support in an initial open season, and is awaiting NEB approval. The target in-service date for phase 1 of this project is late 2013 and phase 2 for early 2014 – long before the Energy East pipeline comes online. Since Enbridge already has gathering systems collecting light crude barrels into the Lakehead system it would appear to have some competitive advantage over TransCanada. As you can see from the list inside the green circle on the map below, Enbridge has a number of Eastern Access pipeline projects planned or in progress to deliver increased volumes of crude to eastern Canada from Alberta and the Bakken.

Source: Enbridge Investor Presentation

If we assume that Enbridge Line 9 goes ahead and feeds 320 Mb/d to refineries in Montreal and Quebec, there will still be refining capacity in Quebec that TransCanada can supply. In part 1 of this series we estimated that light crude refining capacity in Eastern Canada including refineries in Ontario, Quebec and on the Atlantic seaboard (for example the 300 Mb/d Irving refinery at St John, New Brunswick) was about 1 MMb/d. That leaves scope for the Energy East pipeline to replace another 680 Mb/d of imported light crude in addition to 320 Mb/d of Line 9 supplies. If the Energy East pipeline is extended as planned all the way to St John then it will reach markets east of Montreal without direct competition from Enbridge Line 9.

The extent of eastern Canadian refiner support for the Energy East pipeline open season will also be an informative verdict on whether refiners are willing to sign up for longer term pipeline commitments in the light of their current and future potential access to crude by rail deliveries. On Friday Kinder Morgan conceded that they have not see enough shipper interest in their Freedom pipeline conversion project that was designed to feed California refineries from West Texas (see Is the Price of Freedom Too High). California refiners apparently preferred the flexibility of crude supplies by rail. Another of the concerns with the Freedom pipeline was the likely high cost of line fill when converting a pipeline from natural gas to crude. Committed shippers typically have to assume responsibility for buying an apportioned part of the crude that fills the pipeline – a cost of entry that reduces the appeal of pipelines over rail. Using the same pipeline fill calculation math for the Energy East pipeline that we used for the Freedom project we estimate that if the TransCanada pipeline has 500 Mb/d capacity (~ 32 inch diameter) the line fill would be 5,250 Bbl of light crude per mile. The proposed pipeline is 1865 Miles of converted line plus 870 miles of new pipe – a total of 2,735 miles. That would require approximately 14 MMBbl of crude costing $1.3 B at $90/Bbl or about $2.6MM per 1000 Bbl of shipper commitment. In other words if you commit to 50 Mb/d on the Energy East pipeline your line fill obligation would be about $130 MM upfront.

The Energy East pipeline could also be utilized to ship heavy crudes from Western Canada to the East Coast. This could be done in addition to transporting light crudes to Eastern Canadian refineries or instead of light crude. The TransCanada Open Season project description implies that the pipeline is aimed initially at providing crude for Eastern Canadian refineries – meaning light crude as we have just explained. However, there is an argument – especially if the initial proposal does not attract sufficient shippers, to using the Energy East project to carry heavy crude east. In that case, because Eastern Canadian refineries don’t need that crude, the target market would be exports.

Comments

I'm not sure this is correct: " In other words if you commit to 50 Mb/d on the Energy East pipeline your line fill obligation would be about $2 MM upfront."

I took a simplified approach, comparing your method on the Freedom Project, where the line fill obligation is the percent of the Mb/d commitment. 50Mb/d = 10% of the 500 Mb/d at $1.3B so it should be $130MM upfront.

In reply to Line Fill by Peter Warner

Thanks Peter - you are correct. I have made the change in the blog.

Sandy

Hi Sandy,

As usual, great post and thanks for all the work. I had a question regarding open seasons for pipelines. Are they only for new pipeline projects or are they held for existing pipelines as well? The reason I ask is that Spectra Energy just announced an open season for Express-Platte but I don't believe they have expanded its capacity or anything like that since acquiring it from Kinder Morgan et al. Is this just an attempt to raise tariffs by putting expiring contracts out to bid? Any thoughts on the matter would be much appreciated.

Best,

Matt

In reply to Open Season by mattdough

Hi Matt,

Not absolutely sure of the answer to your question. I do know that FERC require companies to hold an open season to make sure all interested parties are aware of changes to pipeline tariffs or service and that presumably includes changes to existing pipelines and tariffs as well as new pipes.

Sandy