The CME NYMEX WTI crude futures contract is the underlying benchmark in nearly all US domestic crude price contracts. Differences between futures and physical trading arrangements make pricing physical WTI barrels complex. Two formula mechanisms are commonly used in physical transactions that link directly to the NYMEX settlement prices – the CMA average and WTI P-Plus. Today we conclude a two-part look at WTI spot crude pricing.

In Part 1 (see The Cost of Crude at Cushing – WTI and the NYMEX CMA) we reviewed the relationship between NYMEX WTI futures and physical crude delivery at Cushing, OK. This blog probably won’t make sense unless you read Part 1 first. We looked at the price components of a typical US domestic crude oil purchase contract. We then worked through a calculation of the NYMEX Calendar Month Average (CMA) that is the base pricing element for most crude purchases. This time we will cover the roll adjust mechanism that links the NYMEX CMA back to physical price timing and then the WTI Postings Plus (P-Plus) alternative mechanism used to price WTI at Cushing.

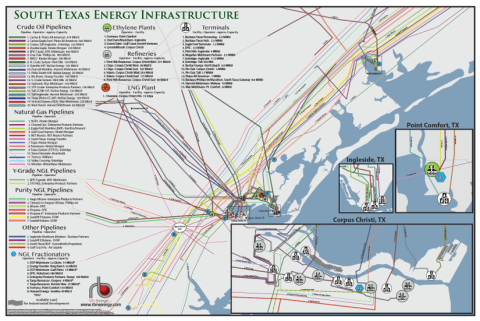

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

NYMEX CMA Roll Adjust

Recall that the basic NYMEX CMA average of settlement prices during the delivery period that we calculated in Part 1 (in our example we chose September 2012) is actually an average of futures prices for delivery in October and November. To adjust that pricing to reflect deals traded for delivery during September the NYMEX Roll Adjust is used. Its called the roll adjust because it adjusts the basic CMA up or down based on whether the prices for September trades were higher or lower than the October and November contract prices averaged in the basic NYMEX CMA. Put another way, the adjustment represents the cost of rolling September futures positions into October or November positions.

What follows is an explanation of how the roll adjust is determined. It gets quite complicated but the tables below should help. The first elements to calculate are the differences between the prices for September delivery futures during the last month that September traded before expiry and the prices for October and November delivery during the same time period. To get those price spreads we first go back to the period when September was the prompt NYMEX futures contract – between July 20, 2012 and August 20, 2012 (see table below). We calculate the average of settle prices during that period for September, October and November. These values are the trade month averages at the bottom of the table.