Crude oil and natural gas prices went through a lot of ups and downs in the 2014-18 period, but the general trend was down. The average price of WTI crude topped $100/bbl in the first half of 2014; by year-end 2018 it stood at $45/bbl. Similarly, the NYMEX natural gas price topped $6.00/MMBtu in early 2014 but fell to a low of about $2.50/MMBtu last year and averaged little more than $3.00/MMBtu. The 44 major U.S. E&P companies we track sought to weather this storm of declining prices by drastically repositioning their portfolios and slashing costs to stay competitive in a new, lower price environment. Their efforts appear to have worked: 2018 profits surged in comparison with 2017 results and approached returns recorded in 2014, when commodity prices were much higher. So why are E&P stock prices languishing? Today, we look at the divergence between investor sentiment and the actual financial performance of U.S. E&P companies.

U.S. exploration and production companies (E&Ps) have found it very difficult to shake the aura of doom and gloom that shrouded the industry after the 2014-15 oil price crash brought many to the brink of insolvency. Investor sentiment, as reflected in the S&P Oil and Gas E&P stock index, tells the tale. After reaching a high of more than 12,000 in mid-2014, the index plunged to as low as 3,600 in early 2016. With crude prices and profits rising after that, the index climbed back to about 6,600 in the fall of 2018, but plummeted nearly 40% to 4,000 — one-third of the 2014 high — in the second half of December (2018) on fears of a return to red ink as oil prices dipped to $45/bbl. But recently released 2018 financial results from our universe of 44 major U.S. E&Ps provided strong evidence that belied the negative sentiment about the sector. [For a listing of our 44 peer group companies, see Here Comes the Rain.] Despite the fourth-quarter oil price decline, the industry roared back to profitability in 2018. More tellingly, the industry has streamlined its cost structure so dramatically that overall 2018 profits were just 20% below those generated in the $100+/bbl environment in 2014. Remarkably, the Diversified E&P Peer Group — whose portfolios are roughly balanced between oil and gas — generated $14.10 per barrel of oil equivalent (boe) in profits in 2018, 7% higher than the $13.20/boe the group netted in 2014, when revenues were much higher. And with first-quarter 2019 oil prices rising 30% — the largest quarterly increase since 2009 — the industry appears to be on track for solid profitability again in 2019.

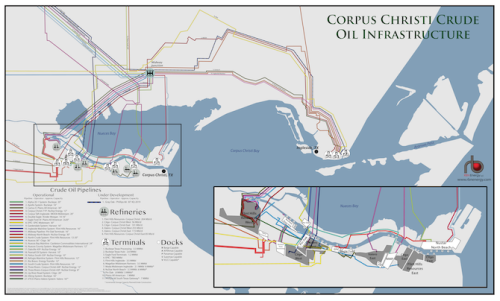

Gain insight and clarity into one of the United States’ most strategic Crude Oil Export Markets with RBN Energy’s Corpus Christi Crude Oil Infrastructure wall map.

After a dramatic plunge from $57 billion in pre-tax operating profit in 2014 to $128 billion in losses in 2015 and $30 billion in losses 2016, the industry clawed its way back to breakeven in 2017. As shown in Figure 1 below, which shows pre-tax operating revenues and profit comparisons on a per-boe basis for our 44-company universe, revenues in 2018 rose a solid 20% year-on-year to $35.86/boe, up from $29.95/boe in 2017. But the group netted a profit of $11.26/boe (blue segment in right bar), a far higher net profit than the $0.07/boe earned in the previous year. The disproportionate increase in net profit was the result of significantly lower costs, including DD&A (depreciation, depletion and amortization) expenses, Impairments, and Exploration/Other expenses, which fell 8%, 59%, and 38%, respectively. The only negative was in lifting costs (yellow segments), which rose 3% to $10.21/boe in 2018 on increased industry activity that placed upward pressure on some service costs as well as production taxes. Underscoring the health of the industry — and nudged by U.S. corporate tax reform — our universe of 44 E&Ps repurchased nearly $16 billion in common shares in 2018, about 50% more than in 2014.

About the song

"Surprise, Surprise" was written by Bruce Springsteen and appears as the 11th cut on his 16th studio album, Working on a Dream. The album was produced by Brendan O'Brien, and released in January 2009. Springsteen said about the album, "I hope Working on a Dream caught the energy of the band fresh off the road from some of the most exciting shows we've ever done." The LP debuted at #1 on the Billboard Top 200 Albums chart, and has been certified Gold by the Recording Industry Association of America. It has sold over 3 million copies worldwide to date. Personnel on the record were: Bruce Springsteen (lead vocals, guitar, harmonica, keyboards), Roy Bittan (piano, Hammond organ, accordion), Danny Federici (Hammond organ — this would be Federici's last recordings with the E Street Band before his passing in April 2008), Nils Lofgren (guitar, vocals), Patti Scialfa (vocals), Steven Van Zandt (guitar, vocals), Max Weinberg (drums), and Soozie Tyrell (violin, vocals).

Bruce Springsteen is an American singer-songwriter, musician, and leader of the E Street Band. He has made 18 studio albums, six live albums, and sold more than 135 million records worldwide. Springsteen has won 20 Grammy Awards, two Golden Globes, one Academy Award, and one Tony Award. He is a member of the Rock and Roll Hall of Fame and Songwriters Hall of Fame, and has received a Kennedy Center Honor and Presidential Medal of Freedom; he also has been named the MusiCares Person of the Year. “The Boss” still records and tours to this date.