For some time, U.S. motor fuel exports to Mexico had been increasing at a healthy pace, reliably filling the void created by a series of production setbacks at Pemex’s refineries south of the border. From 2014 to 2018, U.S. gasoline exports to Mexico soared by more than 160%, from an average of 197 Mb/d five years ago to 517 Mb/d last year. Diesel exports rose by nearly 130%, to 279 Mb/d, over the same period. But that export-growth momentum has since sagged — in fact, export volumes for both gasoline and diesel actually declined in the first few months of 2019, primarily due to logistical challenges within Mexico. Also, Mexico’s new president has proposed ambitious plans to boost state-owned Pemex’s refining capacity, possibly posing a longer-term threat to U.S. exporters. So, is the boom in refined-product exports to Mexico over? Today, we examine what’s behind the downshift, and what the Mexican government’s effort to reinvigorate Pemex’s existing refineries — and build an entirely new one — may mean for U.S. gasoline and diesel exports in the 2020s.

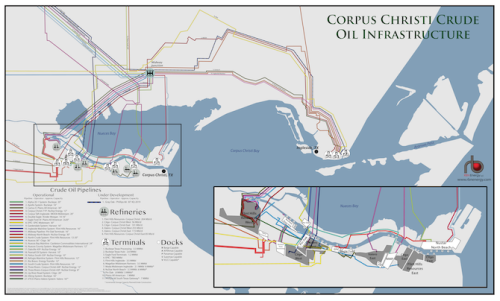

Gain insight and clarity into one of the United States’ most strategic Crude Oil Export Markets with RBN Energy’s Corpus Christi Crude Oil Infrastructure wall map.

Mexico’s shift from net energy exporter to the U.S. (primarily in the form of crude oil) to net importer (lots of U.S.-sourced gasoline, diesel and LPG, plus growing volumes of natural gas) has been a frequent topic in the RBN blogosphere. Back in 2015, in our With a Little Help from My Friends Drill Down Report, we noted that Mexico has tremendous potential to become energy self-sufficient, but troubles at state-owned Pemex had slowed efforts to develop new oil fields and left its half-dozen refineries operating at only about 60% of their 1.6-MMb/d capacity. Well, it turns out that those were the good ol’ days — as we pointed out late last year in our Runnin’ Down a Dream blog series, Mexico’s crude production (which averaged 3.3 MMb/d in 2005 and 2.3 MMb/d in 2015) had fallen to less than 1.8 MMb/d by then (it’s since dropped further to less than 1.7 MMb/d), and Pemex refineries were operating at less than 40% of their capacity. The decline in Mexico’s energy fortunes has been a boon to U.S. refineries, motor fuel marketers and shippers. We’ll start with gasoline.

Figure 1 below contrasts the drop in Mexican production of gasoline since 2014 (yellow line) with the rise in imports of gasoline from the U.S. (orange line). (Note that Pemex provides only the annual average production volumes for the 2014-16 period.)

About the song

“Slow Down” was written by Larry Williams and originally released as a single by Williams on Specialty Records in 1958. Williams’s version features a funky shuffle beat from drummer Earl Palmer and a raunchy honking tenor sax solo by Plas Johnson. The Beatles had been covering “Slow Down” in their live sets from 1960-62 and revived it for a live taping for the BBC’s “Pop Go The Beatles” television show in 1963. They recorded it in the studio, with George Martin producing, in June 1964, and it originally appeared in the UK on The Beatles Long Tall Sally EP later that summer. The song’s first appearance in the U.S. came on Something New, Capitol’s third Beatles album, which was released in July 1964. Capitol released “Slow Down” as a single, backed with a cover of Carl Perkins’s “Matchbox” (another early cover from The Beatles repertoire), where it went to #25 on the Billboard Hot 100 chart. Personnel on the recording were: John Lennon (lead vocal, lead guitar), Paul McCartney (bass), George Harrison (rhythm guitar), Ringo Starr (drums) and George Martin (piano). The Something New cover photo was a picture of The Beatles taken from “The Ed Sullivan Show.” The album also features the group covering another Larry Williams song, “Dizzy Miss Lizzy.” The album spent nine weeks at #2 on the Billboard Top LP's chart, right behind the band’s A Hard Day’s Night, at #1. “Slow Down” has also been covered by British neo-mod group The Jam and Dutch rockers Golden Earring.

The Beatles were an English rock band formed in Liverpool in 1960 that changed the course of musical history. They made 13 studio albums, five live albums, 53 compilation albums, 21 EPs, and 63 singles; they also made four feature-length films. The Beatles have sold more than 800 million physical and digital records worldwide, and have won one Academy Award, one American Music Award, four Brit Awards, 11 Grammy Awards, 15 Ivor Novello Awards, 17 NME Awards, and 3 World Music Awards. They are members of the Rock and Roll Hall of Fame, the UK Music Hall of Fame, and the Vocal Group Hall of Fame. Paul McCartney was knighted in 1997 and Ringo Starr (Richard Starkey) in 2017. John Lennon died in 1980 and George Harrison in 2001. McCartney and Starr both record and tour to this day.