No doubt about it, most of the headline-grabbing oil and gas M&A activity lately has involved large, publicly owned producers gobbling up other good-sized E&Ps, lock, stock and barrel. But there are other ways to increase scale and improve operational efficiency, as evidenced by privately held WildFire Energy’s bolt-on acquisition frenzy in the relatively sleepy northeastern Eagle Ford, aka the East Eagle Ford. In less than three years, with one bolt-on acquisition after another, WildFire — named in anticipation of the company’s aggressive expansion strategy — has morphed from a small player in the often-overlooked area into one of the largest producers there, with a laser focus on maximizing returns to its management and private-equity owners. In today’s RBN blog, we’ll look at the E&P and its rapid rise.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

We’ve been tracking M&A in the Eagle Ford for some time now — the number of deals happening there has warranted the attention. A comprehensive list would be too long, but some of the bigger, more notable acquisitions include:

- Devon Energy’s $1.8 billion purchase of Validus Energy, a privately held Eagle Ford producer, which closed in September 2022.

- Marathon Oil’s December 2022 acquisition of Ensign Natural Resources’ Eagle Ford assets for $3 billion (discussed in Come Back Song).

- Spanish energy giant Repsol’s February 2023 purchase of the South Texas acreage and production of Japan’s INPEX Corp. for an undisclosed amount.

- U.K.-based INEOS’s purchase of some of Chesapeake Energy’s South Texas assets for $1.1 billion — a deal that was finalized in May 2023.

- Canadian producer Baytex Energy’s June 2023 acquisition of Eagle Ford pure-play Ranger Oil in a cash-and-stock deal valued at $2.2 billion.

- The $551 million purchase by privately held Ridgemar Energy of Callon Petroleum’s Eagle Ford assets, which closed in July 2023.

- The $22.5 billion plan by ConocoPhillips to acquire Marathon Oil — both companies have a significant presence in the Eagle Ford — which is expected to close in Q4 2024.

Most recently, in We Could Be So Good Together, we delved into Crescent Energy’s plan — announced in mid-May — to acquire SilverBow Resources for $2.1 billion in cash and stock to create what will likely be the third-largest operator in the Eagle Ford, with about 200 Mboe/d of pro forma production. That would put the company well behind the prospectively combined ConocoPhillips and Marathon Oil, whose production in the region would total about 380 Mb/d, and current Eagle Ford leader EOG Resources, with about 300 Mboe/d.

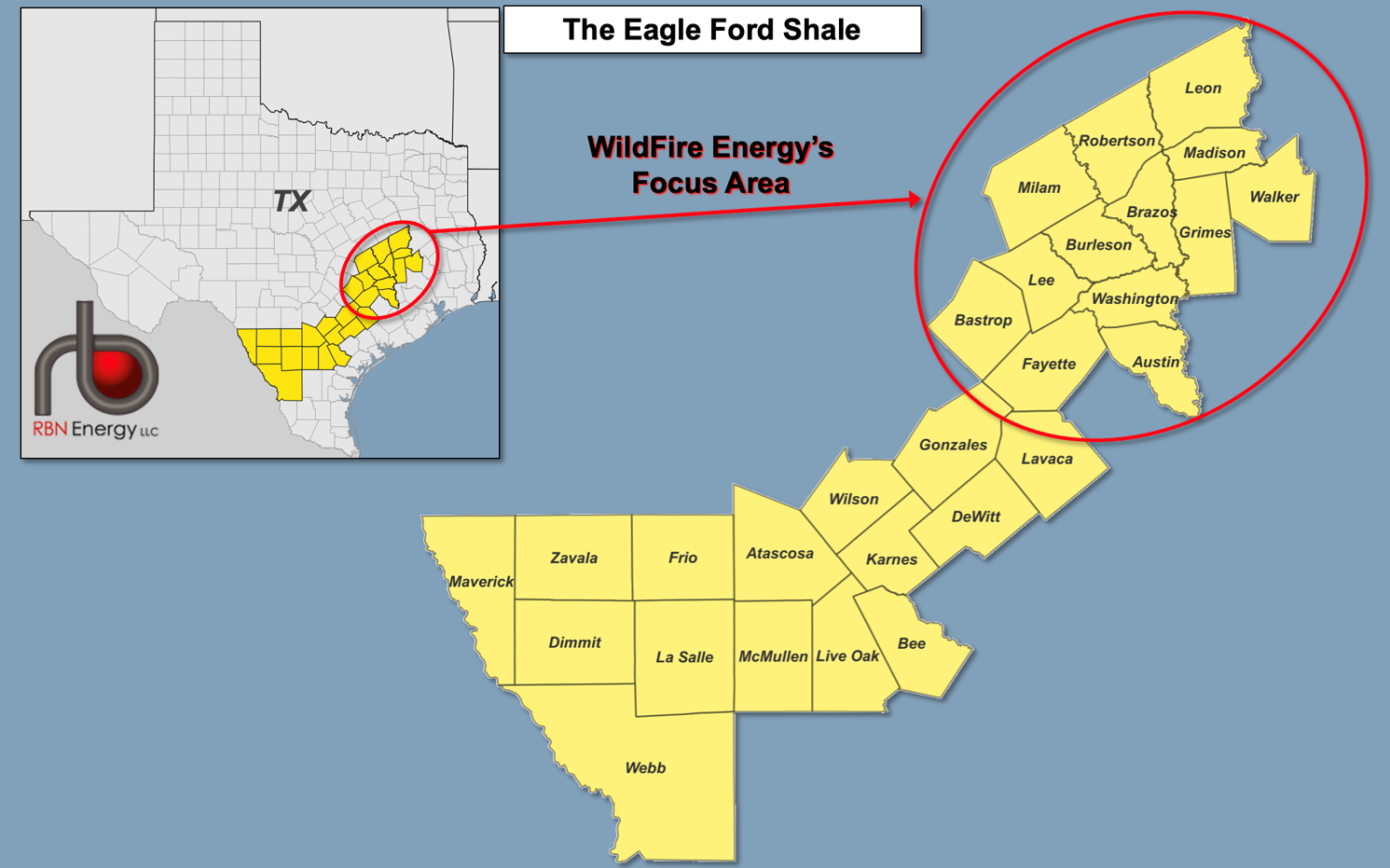

What all those producers and all those deals have in common is that their focus within the broadly defined Eagle Ford (yellow-shaded counties in Figure 1) is almost exclusively on the southwestern 60% of the massive shale basin — the fat swath from the Rio Grande to the counties east of San Antonio (Gonzales, Lavaca and DeWitt). That’s where the vast majority of Eagle Ford wells have been drilled and completed since the Shale Era started in earnest in the early 2010s, and where most of the basin’s production takes place. But the northeastern 40% of the Eagle Ford (area within red ovals) shouldn’t be forgotten — as we’ll get to next, that’s where privately held WildFire Energy has been rapidly accumulating acreage and production.

Figure 1. The Eagle Ford Shale. Source: RBN

About the song

“Wildfire” was written by Michael Murphey and Larry Cansler and appears as the first song on side one of Michael Murphey’s fourth studio album, Blue Sky-Night Thunder. Released as the first single from the album in February 1975, it went to #3 on the Billboard Hot 100 Singles chart and has been certified Platinum by the Recording Industry Association of America (RIAA). With its chorus of: “She ran calling Wildfire,” the refrain is ingrained into the memory of anyone who has heard the sad, somber tune. Murphey said that the song came to him in a dream and was perhaps drawn from a story his grandfather told him about a Native American legend about a ghost horse. Murphey rerecorded “Wildfire” on his 1997 Horse Legends LP. Personnel on the record were: Michael Murphey (lead vocals, piano), Jac Murphy (piano intro and outro), Sam Broussard (guitar), Richard Dean (guitar, backing vocals), Michael McKinney (bass, backing vocals), Harry Wilkinson (drums), John McEuen (mandolin), and Jeff Hanna, Jimmy Ibbotson (backing vocals).

Blue Sky-Night Thunder was recorded at Ray Stevens’s Sound Laboratory in Nashville in 1974-75 with Bob Johnston producing. Released in March 1975, it went to #18 on the Billboard 200 Albums chart and has been certified Gold by the RIAA. It remains Murphey's most successful album to date. Two singles were released from the LP.

Michael Murphey is an American singer and songwriter from Texas. He changed his name to Michael Martin Murphey in the late 1970s to distinguish his name from the actor Michael Murphy, thereby joining the tradition of Texas songwriters with three names. His first big break came in 1967 when his old friend from Texas, Michael Nesmith, asked him to pen a song for The Monkees’ fourth studio album, Pisces, Aquarius, Capricorn, & Jones Ltd. After releasing one album on Colgems Records with the Lewis & Clarke Expedition, Murphey moved to Wrightwood, CA, to focus on his songwriting. He signed a publishing deal with Screen Gems and placed songs with Bobby Gentry, Flatt and Scruggs, and Kenny Rogers and the First Edition. Murphey moved back to Texas in 1971 and became part of the burgeoning progressive country movement. He was signed by producer Bob Johnston to A&M Records and released “Geronimo's Cadillac,” which became a hit and the unofficial anthem for the American Indian Movement. He has released 34 studio albums, five compilation albums, and 46 singles. He continues to perform and will be doing a series of concerts with a BBQ dinner under the stars among the tall pine trees in Red River, NM, in July and August 2024.